This is what happens when people blindly become ‘bhakts’ of so called market gurus who just started investing public money a few years ago and spent a large part of their careers peddling stocks to other fund managers using sensationalism as their prime marketing tool while earning fat salaries. These newbie sell side guys turned into fund managers almost like a clock work have to mandatorily come to business channels to give their views on each and everything under the sun of which they claim to be expert about. Writing books (and then marketing them on every possible forum from linkedin to twitter to what not!!), coming to business channels and dealing with their HNI investors - I wonder when do they actually get any time to do meaningful research other than telling us statistics of Indian markets since independence and their favorite stocks trading at 100 times earnings.

Now coming to the stock in question, everyone was super bullish due to massive media coverage even when the stock was trading at 100 times earnings - and remember this is no amazon, not even HUL, this is a B2B supplier of equipments (not even APIs) to pharma companies. In the world of investing, yes things can look insane for a long amount of time but sooner than later all bubbles have to burst. GMM has been a great stock for momentum traders but can’t be called an investment candidate at 100 times earnings by any stretch of imagination. Yet, so many media friendly guys will not stop raving about it no matter what the stock price is. The problem is that instead of unabashedly telling that they are momentum traders they wear of coat of being long term wise investors. The other problem is that momentum trading is fine when one is dealing with small money, but you can not execute it successfully when you are managing 2000 crores (and another 20,000 cr from your media followers are copying your strategy for free !!).

The primary questions which interviewers should ask in such business channels interviews are:

Should an interested party like a large investor in a extremely illiquid stock like GMM be even asked to tell his views on the stocks? What else was the interview expecting to hear - that it sucks to be in stock without liquidity!! (never ask a barber if you need a hair cut)

Why have the promoters and their learned investors decided to make the stock remain this illiquid till now - why haven’t they announced a bonus share or split the stock. I don’t think there is any other stock which is such a smallcap yet with such less number of shares in existence, thereby susceptible to manipulations.

Why is the QIP happening at 50% discount to price less than a month ago - again there is no precedence of such a large discount at least not that I remember.

If valuations don’t matter because fundamentals are strong - why isn’t this stock doing QIP at 10,000 Rs a share?

When it is a mutibagger story from now, why is their long term partner exiting at 50% discount, why so much of desperation?

In the markets, the only things which work is to be very flexible or very long term oriented. But if your linkedin posts are about your month till date returns in your new strategy then better to have a exit strategy also by being only a momentum chaser in very large cap stocks. The problem is that if one does so, then one can’t hide the fact that you are underperforming NIFTY because you are not having Reliance in your portfolio. And then the problem is Reliance is not coffee can stock. And then the problem is coffee can can’t always be so short term oriented. And then the problem is your short term performance helps you raise funds which is your main concern which is why you are everywhere. So in the end you just have a khichdi and then the only way out is to do what one has been doing all their life - peddle your owned stocks on the business channels rather than like earlier peddling your research stocks to fund managers.

The reason I am writing this is for investors to always remember : Buyers Beware. Media presence of a stock is not going to make your money. Have your own conviction. One downside of today’s internet age is that it is very easy to know what others are doing. However, in investing, Buffett or even Soros have not made their billions listening to media interviews of others. Do your own work, collaborate but don’t get swayed by the media liking of the darlings.

Best,

Sarvesh Gupta

PS - I run my own investment firm. Views are personal.

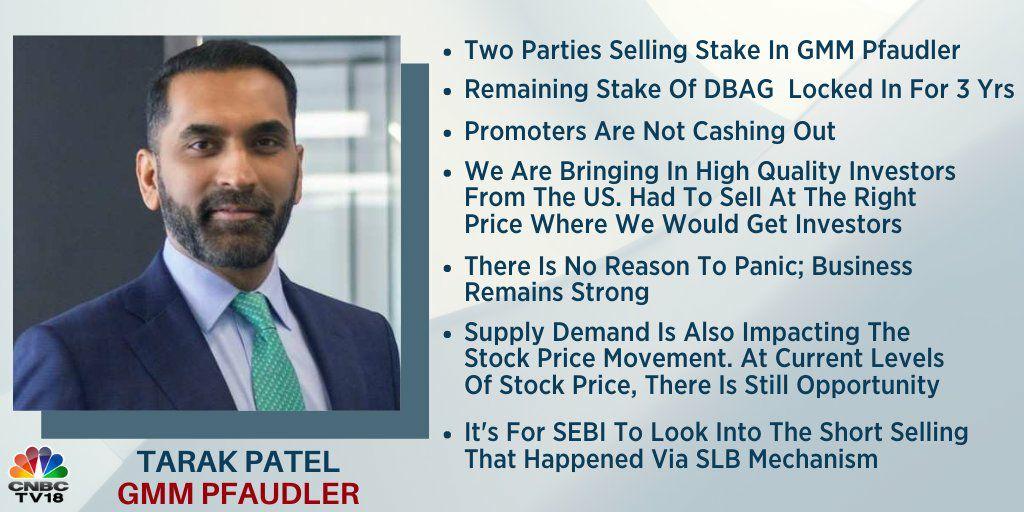

CNBC-AWAAZ (@CNBC_Awaaz) Tweeted: #AwaazExclusive।#GMMPfaudler में लगातार तीसरे दिन लोअर सर्किट, कंपनी के प्रोमोटर की सफाई डिस्काउंट पर OFS लाने की जानकारी लीक नहीं की, हमसे एक्सक्लूसिव बातचीत में कंपनी के MD Tarak Patel बोले हिस्सा बिक्री का बिजनेस पर कोई असर नहीं । देखिए ये खास बातचीत @pandyapradeep के साथ। https://t.co/4rfKF8OaMzhttps://twitter.com/CNBC_Awaaz/status/1309029271143415808?s=20

Md interview with cnbc, answering a lot of questions

Also tommorow there is a conference call to answer all questions.

I would stay away from this company even with increased EPS and lowered P/E after promoter shenanigans. Once, Insider trading is on the cards, it is useless to waste time on checking fundamentals.

Yes, there seems to be a case of Insider trading. According to a CNBC news item as given in the link …

“Some investors borrowed around 74,000 shares of GMM Pfaudler from the Stock Lending and Borrowing window of NSE and short sold them just a few days before the company revealed the price of the OFS. This has raised eyebrows because there were no previous dealings in GMM shares in the SLB window”

Short-selling in GMM Pfaudler: Punter’s luck or inside edge?

The MD, GMM Pfaudler very confidently says it is up to SEBI to investigate…it is possible that either someone outsider could have taken a chance to do it or the so called outsider would have got the information from external sources.

After listening to Tarak Patel in Zee business and CNBC, I am not sure if there is some kind of scam. He is young guy and perhaps a bit immature to go in instagram chats etc. This whole thing of buying global parent and OFS could have been handled better and they just rushed into everything too fast and messed their reputation.

My real worry is SLB transactions. Here like he said, in such a large deal like this there will be 100s of people involved and one guy could have done something fishy. Second worry is how good the global business is. Who are their competitors and how can GMM scale the global business.

I am looking forward to Invest in this company if I get clarity on these two points.

Another thing investors here should watch out for is a future merger of the global business of Pfaudler Group with GMM. GMM only owns 54% of this while promoters have taken 26% directly and 20% is held by DBAG. Tarak claimed in the CNBC interview that management wants to increase its stake in GMM from ~22% after the OFS to 30% in the next few years and the way they might do this is by merging the two businesses once global ops have turned around. This looks like a ripe opportunity for them to play the valuation differential in their favour and convert a stake they bought for 100 cr into a significant ownership of GMM worth multiple times their investment. I see no reason for them to have directly bought into the global business when GMM could have taken the entire 80% itself.

Edit. Detailed discussion on this issue today with Bloomberg. In simple words he is saying “we are selling 2% of GMM today to fund an acquisition which we will convert to 8% of GMM after 3 years via a merger”

So basically they have made the listed Indian entity buy 54% of the global business, with the rest lying with promoters (26%) and DBAG (20%). The promoters sold 2% of their stake in the listed entity to fund this purchase. They hope to do a merger over the next 3 years, and based on their current estimates their stake post merger will go to 30% in the listed entity. In a nutshell, their 25% shareholding goes to 30% (without promoters paying anything) and the rest of equity shareholders are diluted in the process. This is kind of an ESOP transaction where promoters have given themselves more shares of the company (assuming they are able to turnaround the international business). What if international business doesn’t turnaround? Does the Indian entity still buy the rest 46% stake? Or do the promoters pay the listed Indian entity for the international business? Its unlikely to happen.

This is just my opinion, but a better way to do this transaction would have been a share swap deal where the listed Indian entity issued new shares to fund the acquisition. This is very commonly done in acquisitions when the acquiring company is trading at very expensive valuations and the asset they are acquiring is at cheaper valuations.

It’s clear from this convo that the acquisition of Pfaudler global was always part of DBAG’s plan to cash out and Patel family’s plan to increase their stake in GMM (for free). They first “fattened” the golden goose in India with the acquisition and then sold it to institutional investors at a “discount”. Investors loved the fully cooked dish served to them and forgot to check the price of the ingredients. This is a good business but the valuations and management behaviour raise a massive stink.

I have not been following the stock fundamentally but needed to ask a few things:

How is promoters or other investors exiting what has been a phenomenal amount of money made in the last 5 years some sort of lowered corporate standard.

What would be the market accepted way to exit? If exit were at 5000 then it would be okay?

Its actually a company with a very dominant market share, its like a monopoly in pharma capex business and the Indian pharma industry has invested a lot of money into capex in the last 5 years (specially the ones which are rapidly expanding into US like alembic, ajanta, torrent, etc.). Its a very good business, although its still cyclical (like a capital goods company catering to the pharma and chemicals sector).

About price of exit, its not the price which is the matter of discussion but the deal structure which could have been done in a more minority shareholder friendly way. However, there have been much greater corporate governance issues that have come up in other companies. This is not a case of fraud or even corporate misdemeanor, its just not very shareholder friendly.

However, the level of disclosures is really bad. I say this because the past run up to 7000 happened before the global acquisition news and post the news prices actually went down (its like buy the rumor sell the news). Again for this OFS, somebody knew; that’s why the huge borrowing before the news was made public. So there is definitely information arbitrage happening here.

No doubt, it is very difficult for any analyst to explain whether these steps taken by GMM Pfaudler management are right or not.

At some point, it looks fine as it is a PE firm(DBAG) who sold the majority of the stake. Other hands, the question is why in such a cheap valuation. But again, Rs.3500 is not cheap at all as @Rs. 3500 P.E ratio is 72.

DBAG could sell the share gradually instead of once at a time. In that case, probably they could get a higher valuation. But it is unlikely to be an option due to the low volume in the share.

Why are the promoters not buying? You can’t complain as valuation is still very high.

Now there is an allegation over insider trading but it is not yet proved whether it is done by the promoters or not.

I can tell you that lot of insider trade happens not because of the promoter but service providers like investment bankers, trade advisors, legal advisors, auditors, board member and their brokers. It is also very difficult to prove if SEBI doesn’t find direct relationship with a leaker. SEBI might investigate and might not take any action due to lack of solid evidence. Investors should not worry too much unless the promoter is found involved in these insider trades. Prima facie it does not look like a case of bad governance. Just think about the whole issue if the stock price was say 4000/share and they still went ahead with the same plan of offloading @3500. Would it cause so much heart burn visible today?

To an extent speculators who took the share to 100+ PE are responsible for this mess. Any sane biz man promoter and Pvt equity included would take advantage of this situation. Communication could have been better but the promoter looks high on adrenaline and low on maturity.

Yes, I agree with your point here.

While the investors are responsible to buy@ 100 P/E, but the way in which the stock was extensively covered through Digital media and recommended very strongly by the so called Fund manager GURU’s at multiple occasions is a cause of concern…

Afterall, it is not a stock with a big MOAT nor a Retail stock like DMart, or Trent nor digital media stock like Info-edge. It is just a performing cyclical stock with some tailwinds from pharma / chemical sectors which nobody knows how long it would last…

Learnt a couple of lessons, (1) never invest in a small cap stock unless it has a strong Moat with reasonable valuation and clear high growth visibility. (2) Never get influenced by others/ Media / fund managers/ Digital media… you may watch , listen , read … but do your own assessment…with regards to credibility of promoters, promoter stake , multiple entity promoters… etc etc.

(3) Be cautious if PE investors have invested in any stock … or dont buy a stock just because PE Investors are buying… they may exit any time which may result in to a crash.

Discl… Entered @1400, 50% Sold @4500 level before 2nd circuit breaker…will watch further development and then decide whether to continue or exit…anyway, I have already made a profit…

The big concern I see is that the suddenness of the OFS announcement; while there was roadshow for the institutional investors, retail investors are out of the loop.

Could have been handled better from communicating the block sale better & longer OFS window for retail investors.

That being said this OFS event for me

Increases float in the public markets for the company. More liquidity & better price discovery.

Brings in more institutional money from the current ultra low levels of institutional holding. This will increase scrutiny & increase quality of conversation about the company.

Exit of PE fund from being a 50% owner and now we know in 3 years there can be another such liquidity event. Core promoters still are around & hungry to make money.

So, Overall still positive on the long term prospects. Being a small cap, I am taking this event in stride.