Current market cap of GHCL is 4,740 Cr. The capex of GHCL is 4,000 Cr(Green field capex) + 300Cr (Bromine+Vaccumsalt) in next 3 yrs. Current Soda ash price which are at bottom due to turkey import. As per the management, after capex - they will touch max of 0.5 Debt to Equity ratio which is quiet healthy.

Risks:

- Dependency on Soda ash prices - crash or range bound for next 1 or 2 years

- Turkey soda ash dumping continue due to europe slowdown

- Company capex plans are delayed.

- Delay in raising funds.

- Tata chemicals capex will be commenced before GHCL.

Any other risks which I am missing?

2 Likes

GHCL Q1 FY25 Analysis: Key takeaways!!

Business Outlook:

- GHCL delivered operationally strong performance in Q1 FY25 with volume growth and improved cost efficiencies, despite moderation in soda ash pricing globally.

- Management expects 5-6% volume growth in soda ash and 20-25% growth in sodium bicarbonate for FY25.

- Demand outlook remains positive for India, with 2-3% growth seen in Q1. Solar glass investments expected to drive demand from FY26.

Strategic Initiatives:

- Focus on cost optimization and productivity improvement across operations

- Expanding sodium bicarbonate capacity

- Developing 500,000 MT greenfield soda ash plant

- Received 6,449 hectare land allotment for salt production to support existing and new capacities

- Progressing on vacuum salt and bromine projects for diversification

Trends and Themes:

- Global soda ash demand remains mixed, with strong growth in China but slowdown in Europe/US

- India soda ash consumption growing but imports declining due to supply chain issues

- Shift towards solar glass and green energy driving future demand

Industry Tailwinds:

- Growing domestic demand for soda ash in India

- Government initiatives promoting solar glass manufacturing

- Increasing applications in lithium batteries, green hydrogen

Industry Headwinds:

- Global overcapacity and pricing pressure

- Demand slowdown in certain end-use segments like auto

- Supply chain disruptions impacting trade flows

Analyst Concerns and Management Response:

Concern: Sustainability of margins given global pricing pressure

Response: Cost initiatives and operational efficiencies to support margins; pricing believed to have bottomed out

Concern: Timeline and funding for large capex plans

Response: Strong balance sheet with ~INR 1000 crore cash; capex to be spread over 5-6 years

Competitive Landscape:

- GHCL well-positioned as cost leader in Indian market

- Global players like Solvay facing cost pressures in Europe

- New capacities coming up in US and China creating oversupply concerns

Guidance and Outlook:

- 5-6% soda ash volume growth expected for FY25

- Sodium bicarbonate to grow 20-25%

- Cautiously optimistic on demand recovery and pricing stabilization

Capital Allocation Strategy:

- INR 7000-8000 crore capex planned over next 5-6 years

- Major investments in greenfield soda ash plant, bromine, salt fields

- Maintaining 1:1 debt-equity discipline

Opportunities & Risks:

Opportunities:

- Growing domestic demand from solar glass, batteries

- Backward integration into salt for cost advantage

- Diversification into bromine

Risks:

- Global overcapacity impacting pricing

- Execution risks in large greenfield project

- Volatility in energy costs

Regulatory Environment:

- Reinstatement of import duty on solar glass to boost domestic manufacturing

- Environmental clearances required for new projects

Customer Sentiment:

- Strong inquiries from solar glass manufacturers

- Auto sector seeing some slowdown

- Overall positive demand outlook from domestic customers

Top 3 Takeaways:

- Cost optimization initiatives driving margin resilience amid pricing pressures

- Significant capex plans to expand capacities and diversify product portfolio

- Positive long-term demand outlook from solar glass and green energy applications

3 Likes

638639055532914352_GHCL Ltd - Company Update - SMIFS Institutional Research.pdf (827.6 KB)

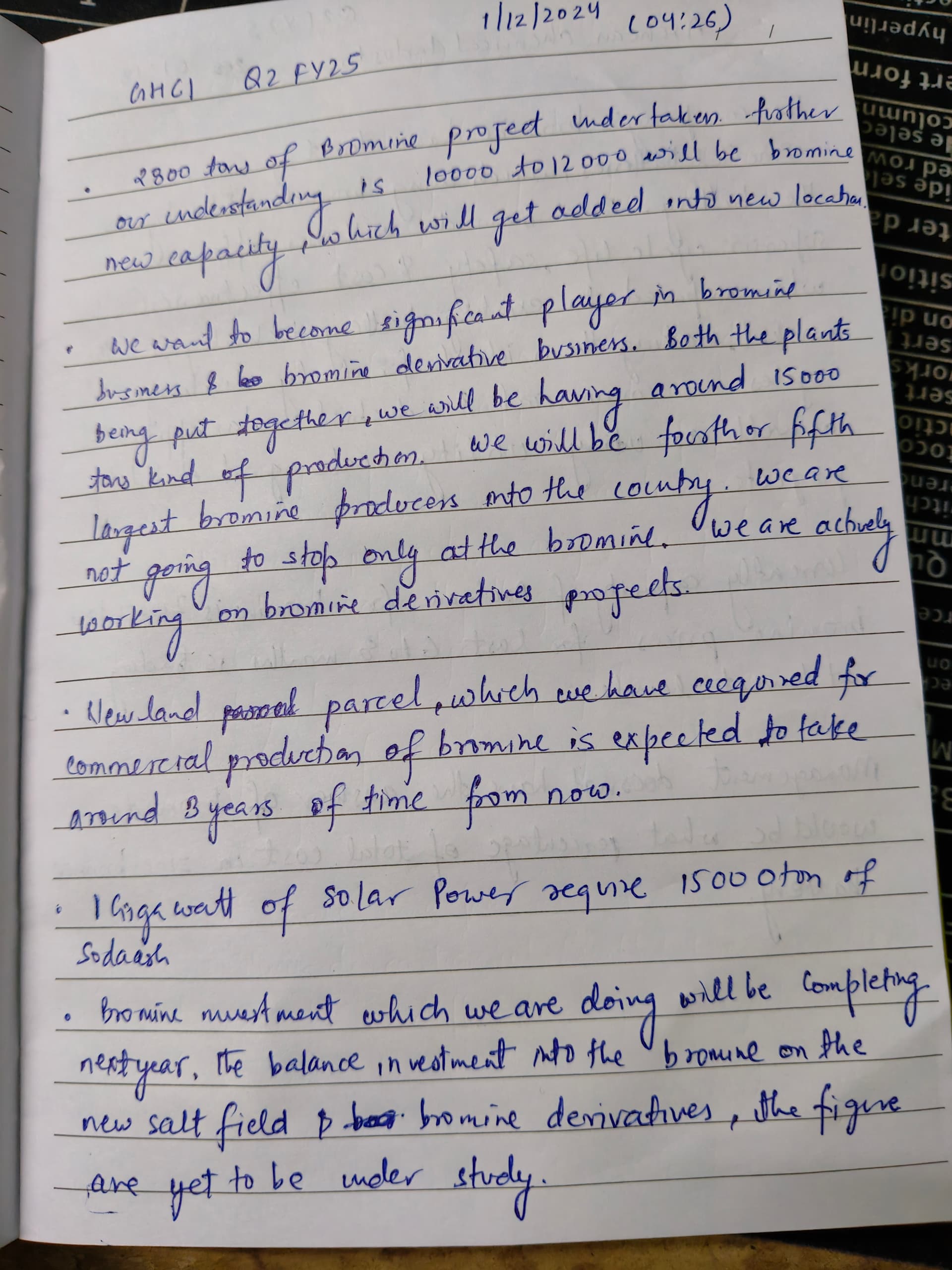

Ghcl is going to venture in Bromine space. Capex for the same has already been started by the company. Will share my notes very shortly. Holding from 167 levels for more than 8 years.

5 Likes

Another house sees upside.

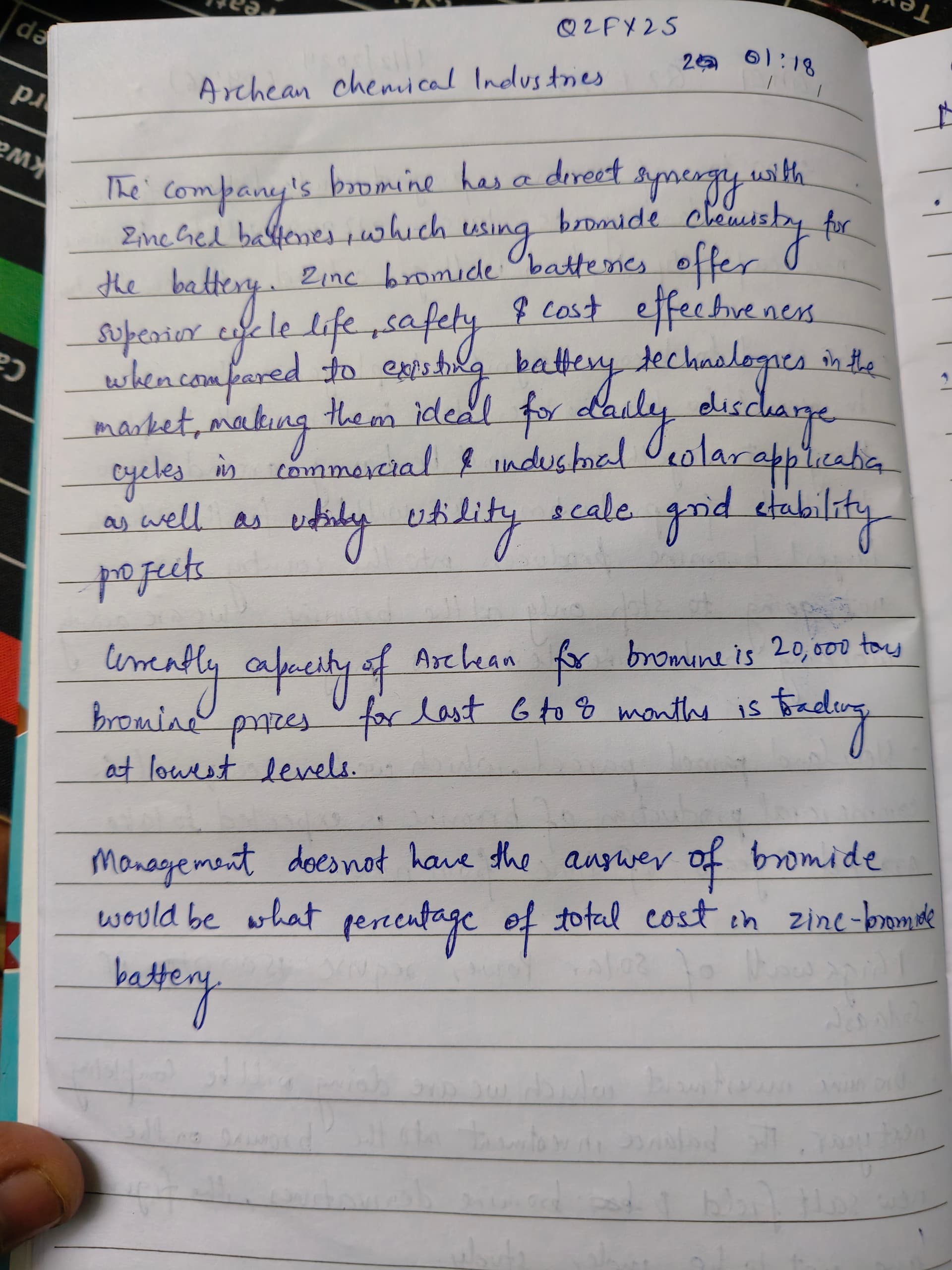

For comparison purpose I have also studied Archean chemical industries which is prominent bromine player.

Let see where this new segment (bromine) takes Ghcl. Finger crossed.

Disclaimer: Invested at 167 levels before demerger and part of long term portfolio, with holding time of 8 years.

4 Likes

Seems Good for GHCL, though Tata Chemicals not so benefitted as their Indian operations in consolidated sales are only going to get benefitted from these.

Wondering against the notified price (minimum import price is Rs 20,108/MT) … what’s the CMP ongoing in market ![]()

Awesome habit of keeping notes for future reference … thanks for sharing.