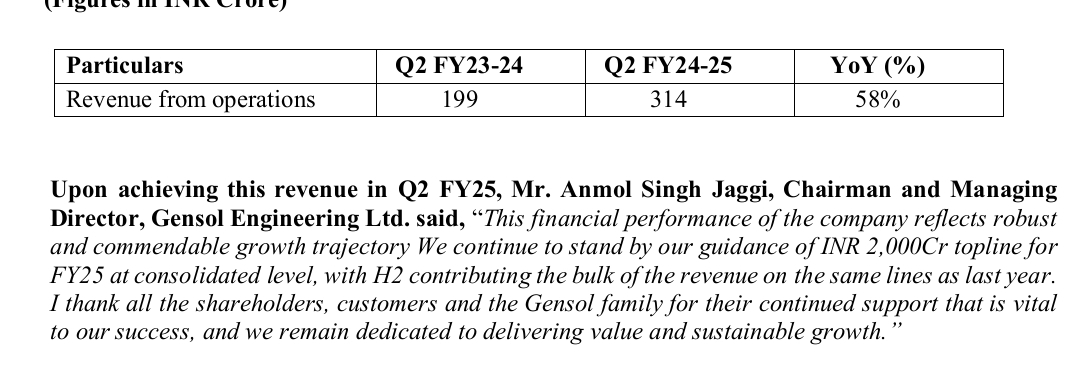

By looking at the Q2 numbers released by Gensol (Revenue of 314 Cr.) this maths doesn’t seem to be working very well.

1 Like

Yes the revenues are missing the guidelines by miles.

If possible can you please explain a bit more about BESS projects.

What is the approx per MW price?

Who puts up the capital?

How does the revenue work? And for how many years would this revenue come in?

What do you mean by Terminal value post 12 years would be 400 crs?

Thanks in advance

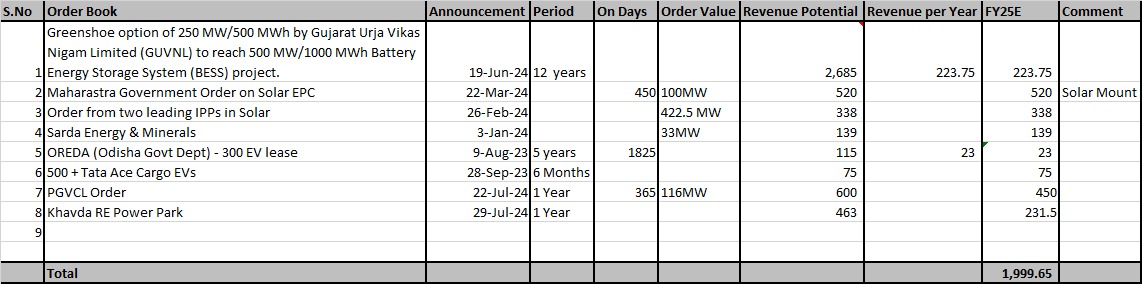

Typically Q4 is where the company gets almost 40-60% of their Revenue. And according to the calculation I did (based on their orders) they can achieve this 2000 crores Revenue.

I feel they will achieve this 2000 crores target based on the order they have

Even though I have invested in this company (1%), still I don’t get the confidence in the promoters as I feel they aren’t able to deliver what they have promised (EV Vehicle) on time (2022). Also, I feel recently there is no new announcement of orders which is What worrying me the most as their competitors are getting some order every month

2 Likes

I have same worry about Gensol not being able to deliver on EV. They keep on saying from 2023 that EV is about to be launched. I am not sure about how many people will buy their car as personally I didn’t like the design of their EV. But i think they will first use their EV in Blu Smart and their leasing business. It should consume their EV atleast for 1-2 years of production. Gensol is one of my biggest allocation(around 6%) and it is turning out to be hope story now.

Going back to my previous comment made 6 months ago on the company, I still don’t fathom the hype around this stock. In the last 2 months I have got several whatsapp tips on this stock.

I’d rather play EV theme, if at all, with better quality names and protect my capital.

Small or microcaps with zero ownerships from institutions or tier-1 PMSs are driven by liquidity from tier-2 PMSs or big HNIs and once they notice sign of bull market flattening or in recession they will bail out causing even further deep cuts in the stock prices.

1 Like

My highest allocation is Gensol Engineering.

My thesis:

-

SMILE formula (Vijay kedia Sir’s Formula).

-

Its under valued…

-

If they give guidance of X.

I am very very happy that they are executing of their guidance atleast X/2.

Here X/2 is greater than previous year sales.

2 Likes

If you see my reply, all I am saying is, company looks good and the promoters don’t look like a Chor (Cuz they have Blusmart running) but I feel this company has to burn a lot of cash as their EV Manufacturing and Leasing business is yet to be profitable, and will not be profitable (EV Manufacturing) till FY29-30. Leasing business will be profitable (Bottom-line) only in FY26-27. I feel they will be profitable and will do well for one more years.

Also their valuation is cheapest among their peers for FY25 (Trading at 20x times) while their peers are trading at 70-100x.

So if you ask me, in Gensol all I care is their EPC Business, other businesses are just an addition to the cashcow business (Solar EPC). So if they deliver in other businesses just like their Solar EPC business then we are seeing a 20,000-30,000 crores Market Cap company.

My only problem is their EV Manufacturing and Leasing business (mostly leasing to Blusmart).

Why leasing business is a problem to me? - Cuz lets say they want to go for an IPO (First Indian taxi or ride-hailing company to go for an IPO, correct me if I am wrong). They have to show profits so that investor will pour money, normally if you are leasing a car for the taxi business, rent will eat at least 30-40% of their revenue, depreciation will eat 10% (maybe 5%), petrol cost will eat another 35-45%, so the margin will be less than 10% and PAT margin will be in the range of 5-7%. If I am a promoter, I will reduce my rent cost to less than 10 or 20%, I feel this is what they will do when the IPO time comes, if thats the case, then Gensol will yield less than 10-20% on their investment in Leasing business

So I don’t care about the Leasing or EV Business (Though I plan to ask this question to the management in the current quarter call). Still, if they don’t eat the profits of Solar EPC and run on their own. And Solar EPC business gets at least 50% more order to the previous year, I am very much comfortable in owing this or even increasing my allocation.

1 Like

What you have mentioned about Blusmart is correct but what is the point of worrying about Blusmart ?

Can you through some light on why their EV leasing business is making loss? Somehow i dont get the factors which will improve their margins as the business grows to large volume.

Promotor has said it in concall that the same team / system in place can manage large volume. Is that enough to make an impact on margins? On a contradictory note, why can’t you increase team size as the volume increases? why its needed upfront?

I think you didn’t understand the thing I said about Blusmart, see for a company like blusmart to come to IPO, it need to show profit, but the problem is they aren’t is having one. So, what happened is they will do OPEX, how? Simply they will cut the cost of paying the money as a lease to the owner, in this case Gensol which has the same promoter So GENSOL and BLUSMART comes under RPT, to make one thing profitable (Blusmart), they will burn the cash in another (in this case GENSOL), in that way the leasing business will always burns the cash and won’t make profit for the next 2-3 years.

6 Likes

that was helpful, thank you. Never thought listed entity can burn cash for unlisted entity just like that.

1 Like

Thanks very helpful.

1 Like

All I am saying is that their previous accounting has showed lesser results than present. Aggressive accounting would be when the restated results are lesser. I feel the stock is getting way too much negativity since that Zenith issue.

2 Likes

While the company revenues and margins look fine, stock is near 52wk low in Stage four. I do like their business, promoters and valuations as well are at 35PE TTM. But no healthy buying, no institutional interest whatsover is causing the story to be distorted. All ears to hear a counter thesis as to why this is still a good company from a 2-3 year perspective.

3 Likes

Has anyone used or seen a Gensol’s leased EV?

Separately, has anyone in the group visited their EV car manufacturing plant? will be good to get any thoughts.

My sincere apologies if this was addressed in the thread and I missed it.

1 Like

Gensol has more than 15 customers who lease vehicles from them. (Page 8, Q3 FY24 Results Conference Call) BluSmart accounts for more than 50% of that. (Page 11, Q4 FY24 Results

Conference Call) BluSmart cabs are quite commonly seen in Delhi NCR.

Scorpio tracker order book was 1000MW+ 8 months ago but why meaningfull revenue not coming from it? Anyone have idea about it.

I think they add Scorpio tracker revenue in solar EPC segment.

Currently trading at 2700 CR Market cap.

Big opportunity for buying gensol at this level

If we see gensol direct compitition - Oriana Power

Anyone can get great insights about how gensol is extremely undervalued.

Everyone is commenting here about 2000Cr rs guidance

Let’s deep dive

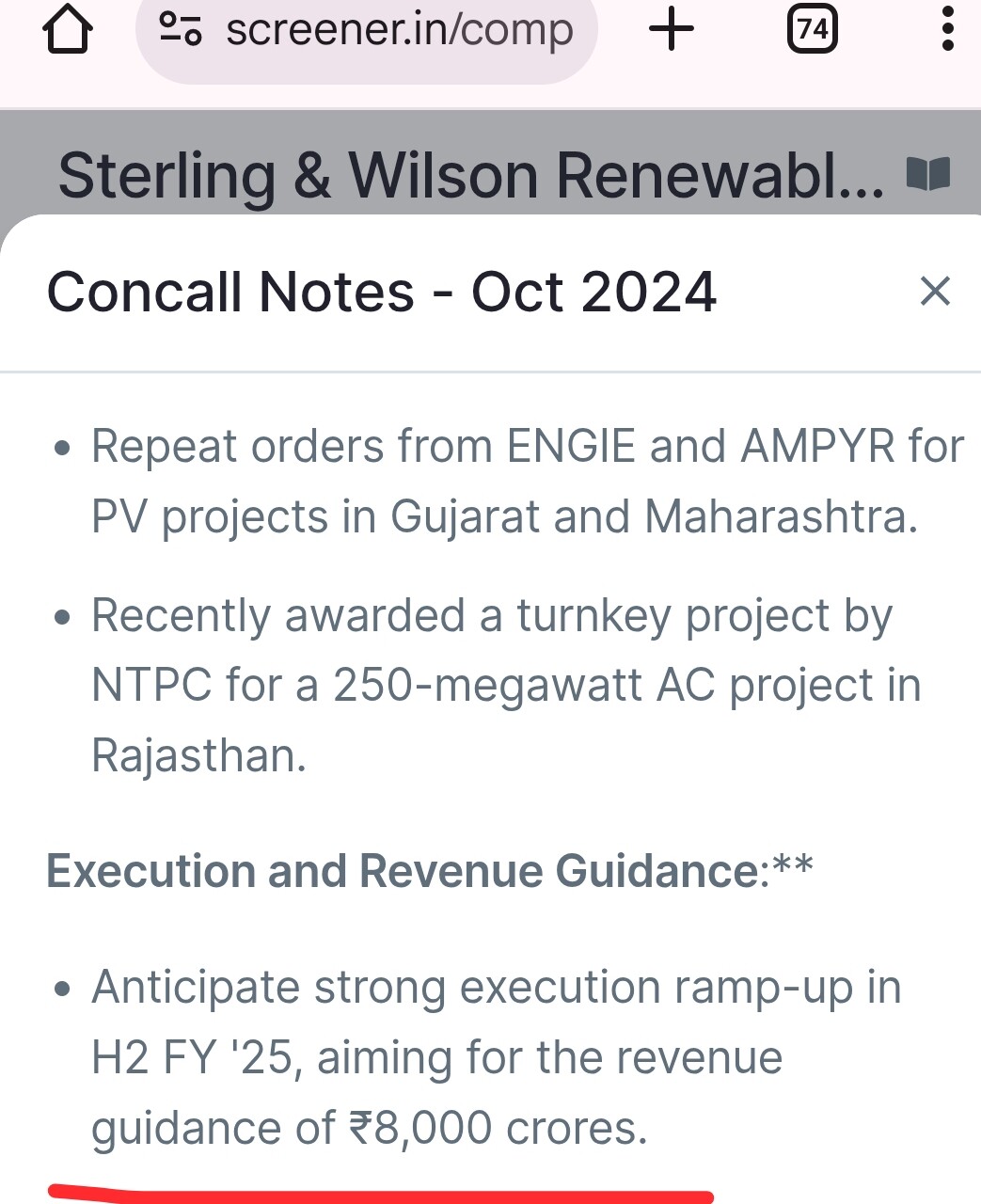

sterling& Wilson fy 2025 guidance - 8000Cr

They have done approximately 2000cr in H1

75% Still Remaining for H2

Oriana Power fy 2025 guidance - 1000 CR

Co. Have achieved 360 CR revenue is H1 means 36% of guidance

64% Still Remaining for H2

Gensol engineering fy 2025 guidance - 2000Cr

Co. Have achieved 708 CR Revenue in H1 means 35.4% of guidance

64% Remaining for H2

They are all Solar epc companies and Oriana Power 99% business match with gensol

And

In Q2 FY25 Results promoter himself mentioned 2000 Cr guidance in Q2 results pdf and said same in opening commentry of concall

So relax and accumulate

Disc- <45% of portfolio

Highest allocation for me

2 Likes