All ValuePickr friend should read SEBI’s order on Gensol as attached. It explains how the loans sanctioned by IREDA and PFC were diverted to the promoter’s account. Shockingly, the company even forged letters from these lenders—manufacturing letter that IREDA and PFC later confirmed they never issued.

For most companies, especially from a retail investor’s perspective, one of the most important red flags should be significant promoter selling (typically 3–5%). Even if the company isn’t involved in fraud, such selling often points to overvaluation.

Take Gensol as an example—the promoter stake dropped by around 7% between March 2022 and March 2023. This kind of significant offloading should be a primary reason to exit or not to enter in stock, despite of exceptional numbers of revenue etc. The only exception to this rule is when the selling is done by a Private Equity (PE) firm—as seen in cases like Home First Finance. Over valued example is Easymytrip, stock price is halved when promoter first sold in March 2023. Always check change of promoter holdings.

We all expected fraud to some extent in this company.

I mean writing was there on the wall.

Icra/care downgrading their rating to Default.

They alleging fraud document was provided by company regarding loan repayment.

Cfo resignation comes to light the next day.

But fraud to this extent:

They were treating public money as their ancestral belonging.

I would be really amused, if somehow promoters escape the jail sentence even from this.

This was posted by me in oct 2023. From the outset this was a fraud including Blue smart which was so a asset heavy startup pretending to be a platform with E vehicles as a bonus .

Ms dhoni, deepika padukone and very big names like renew CEO are invested in blusmart and gensol in earlier funding rounds that was also one of the reason I got very convinced with this company and made it 40% of my portfolio

But these guys have put some much reputation and trust for some pennies like 100-200cr and luxury items

Gensol would have become a 20kcr mcap company easily had they stick to just the solar EPC and renewable energy biz as the boom is just starting

But they screwed it for pennies interms of what they would have got later

Hope they get in jail and never come back for the sort of wealth destruction and savings retail share holders lost due to this frauds

I haven’t looked into BluSmart or how annoucement of rebranding to Uber Green might play out, but I really hope you’re able to recover your losses in the long run. Accepting mistakes is the first step, and I genuinely respect your courage for facing it head-on.

From my own short experience, there are always new opportunities—good trains will keep arriving at the station. I hope the next one takes you to a better place, with better rewards.

I’ve been thinking about portfolio concentration too. I usually found myself running with 30 names, highest 8% weight, but sometimes I wonder how much to bet on a single name. Concentration can be powerful, but also risky. Still figuring it out.

One line of unsolicited advice from a fellow investor - whatever company or management you invest in - if you see anything in social media which questions their lack of integrity then do not even touch that company with a barge pole - no matter how much fan following is there for that particular company. For gensol - there was enough warning and red flags floating around in twitter. Yes - those allegations may not have turned out to be true… but it would be better to stay away and miss a good investment rather then risk a large part of portfolio. Also - we have all done our mistakes and learnt so dont feel too bad. Hope this helps.

This is not confirmed. Anybody who has studied Gensol: how it is likely to affect Gensol in case the sale goes through?

Disclaimer: Made a small investment in Gensol today.

It’s not going to change the life of gensol investors, since bluesmart isn’t a subsidery of gensol.

Though promoter group is the same

One may make an argument, that sale of bluesmart will allow promoters to access money, because promoters will get money in case they sell bluesmart and thus they may be able to infuse money in gensol.

But given the reputation of Jaggis, I doubt, even if they get money, they will infuse it into a firm, they looted.

If they were sincere about gensol, they wouldn’t take money out of a firm that’s already starving for cash.

Agree @jhon_azhar

This seems catching falling knief. One need to consider, would you buy whole company if offered at 421 cr (Current market cap) which has 53 cr paper profit but 98 cr cash flow loss and 1372 cr debt?

Even if such co acquired, equity holder may get almost nothing. e.g. Ruchi Soya is acquired by patanjali. As part of the approved resolution plan under the IBC Code, the existing equity share capital of Ruchi Soya was reduced by 99%. If someone held 100 shares of Ruchi Soya before the acquisition by Patanjali, they would have received 1 share in the restructured entity (Patanjali Foods). Similar is for Orchid Pharma.

This is my understanding, if anyone has different view, I would like to listen and if needed would like to change my pov.

I think most of the debt is pledged and lenders are cashing out so I am.not sure if they will be left with any debt in the end

Also they have leasing assets worth 500-600cr in cars that can be sold out

But in any case if some company offers to take equity of jaggi bros and infuse liquidity to continue the solar EPC execution or else it’s a falling knife only

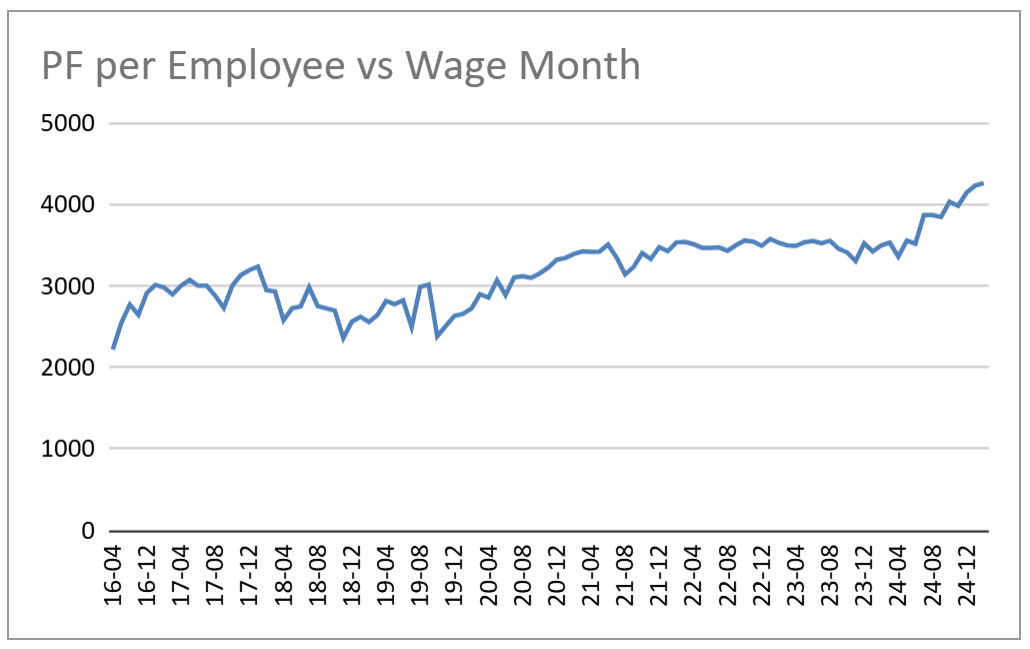

Using EPFO data, I tried to see if we could pinpoint the fraud, but it seems that the folks at Gensol did know how to game the PF employee numbers. Both the employee count and the total PF paid increased as they showed their sales growing

What was the rationale for making that investment? Is it pure speculation and hope? I just wish to understand why people buy such companies. Personally, I wouldn’t dare to touch this company.

It was silly. I fear, the CNBCTV18’s first headline was wrong. It said Eversource to buy Gensol, or may be I got it wrong. And I made the mistake many investors make. Jumped up thinking they will rescue Gensol. And this when I am not a trader.

May be ‘buy the hated companies’ rang somewhere in my mind. Now my hope is to get out of it.

You were not the only one. There are multiple bulk deals in 120s that are very large, somebody even bought 15 lakh shares at 127. Hope you get the exit soon. People will buy this all the way to zero. Seen this in case of Kingfisher Airlines too. People bought right until it got delisted.

I think we should learn from our mistakes. Investment based purely on hopes is basically speculation. One must try never to speculate, or if one must, only in very small quantities. Maybe one should keep an annual limit and a funded dmat for this hobby(I do this). Take it as luck and move on.

For proper investment decisions, must be like our mother is/was with clothes. Bargain hard, look at a few counters, ask a lot of questions, reject on smallest things. Most of all, have a clear idea about expectations, budget and need.

I have seen this happening after RBI had written off the Lakshmi Vilas Bank equity. All who were waiting for its take over by a bigger bank got their teeth knocked out. And I could sell my shares after the equity had been written off. Same evening.

Today there were no buyers. Anyway, ICICIdirect does not allow either reverse trade in it or a sell till delivery has been received.

We keep making our last mistake.

“For proper investment decisions, must be like our mother is/was with clothes. Bargain hard, look at a few counters, ask a lot of questions, reject on smallest things. Most of all, have a clear idea about expectations, budget and need.”

Fantastic advice. So grateful.

Thanks a lot for responding i lost 60% of my profits last year to gensol and to this scam but I am strong and trying to make up in other scripts and my strategy has changed a bit after this set back i am not going with such high allocations any more

As I feel there are many high growth stocks in market and we don’t need to concentrate so much on 1 stock