Been holding this since Sep last year, done well for me and have good hopes from this going forward as well. Things that appealed to me when I researched this (am listing only the crux of my investment thesis here)

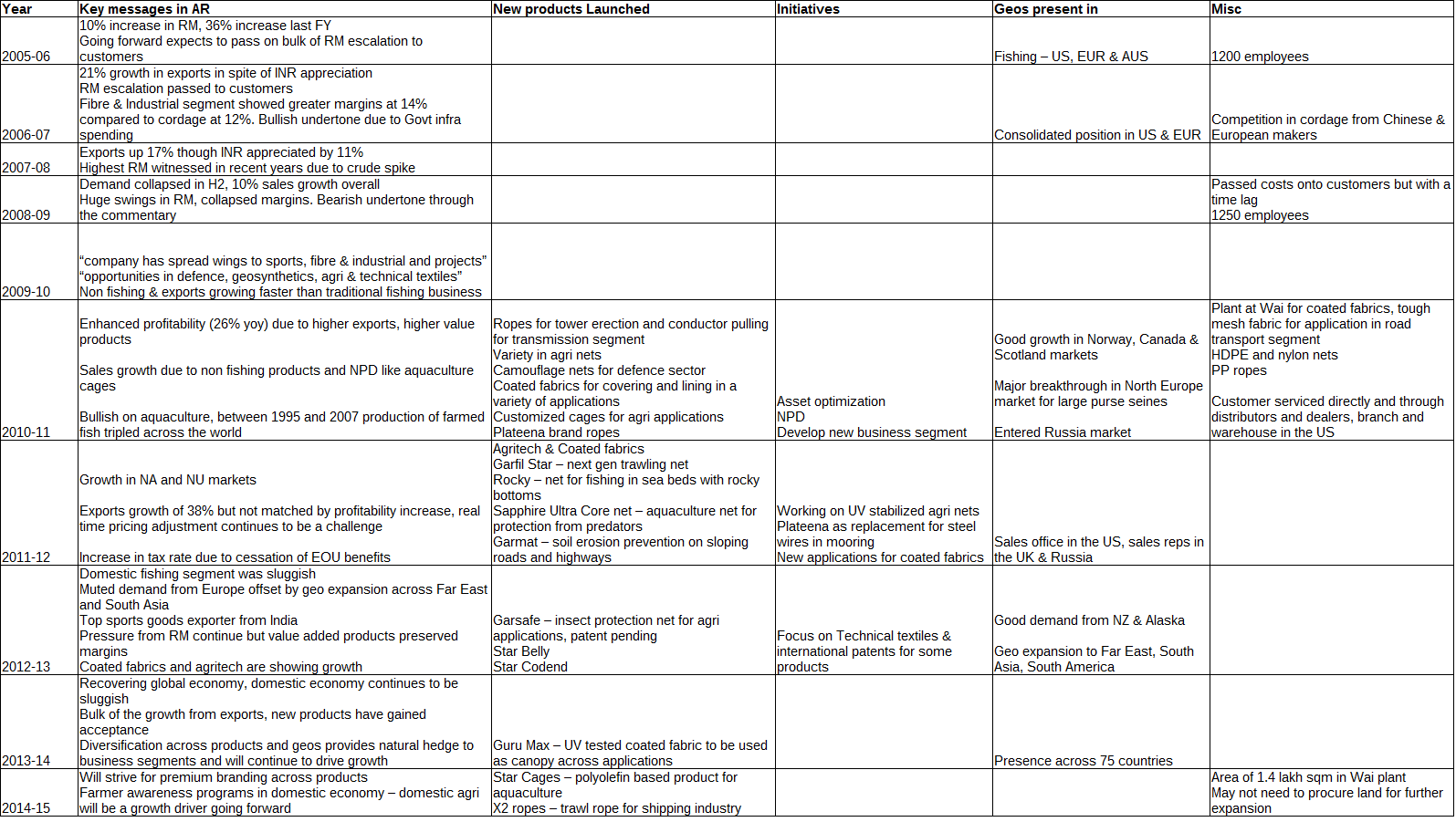

- While this has not been a high growth business over the years it does not take too much effort from here to build products for new avenues. Technical textiles is a huge industry worldwide, though GWRL is playing only in some segments (Sportech and Agrotech) they have demonstrated the ability to build customer specific products without too much investment in R&D. Attaching a snapshot from my research note, the R&D and New prod Devpt appears to be well managed. Possibilities appear very exciting though there is quite some distance to go before the company can demonstrate the ability to tap into an addressable market size of 50,000 Cr per annum.

-

Very good financial discipline, it was very evident from the cash flow analysis that profit/incremental capital would be high over the next 3-4 years. They have spare capacity in the industrial segments that can be put to good use in Govt and defence based domestic orders. Positive FCF at an OCF yield of almost 9% meant that downside would be very limited even if things were to go wrong. Met my criteria of an asymmetrical payoff matrix, upside to downside ratio clearly in excess of 3:1

-

Dominant position in most of the segments (fishing nets, sporting nets) with aquaculture showing promise going forward. Incremental growth expected to come in due to tapping into newer geos initially before the NPD cycle assumes critical mass

-

Demonstrated ability to ride out commodity cycles without too much variability in margins, a management that appears very reticent to run after publicity and believes in focusing on what’s happening on the ground

This was one of those cases where the possibilities looked promising though the path to glory wasn’t very apparent to me. The final decisive factor for me was the valuation at which this was going, I was willing to put in a bet that would yield multibagger results for above average results and keep my principal intact in case things continued to be average. At CMP it looks fairly valued for the prospects unless something fires which can tip the medium term growth rate to over 15% yoy

I had presented this to a couple of funds/investors and none of them were willing to buy this based on my logic. Guess that’s the advantage that we retail investors have - we can be agile, stay under the radar and take time to build our positions.

Disc: Invested, this is a 4% of my net worth kind of position since I am investing based on possibilities, not based on strong conviction like I have in an APL Apollo or a TCPL