Float + Moat = Shipbuilding businesses in india(Cochin shipyard, Mazagaon shipbuilders and Garden reach shipbuilders.

2 Likes

Could you explain the float here? Are these companies getting money in advance?

The location, BKC, where these facilities are located is a financial district. There is enough room for both.

1 Like

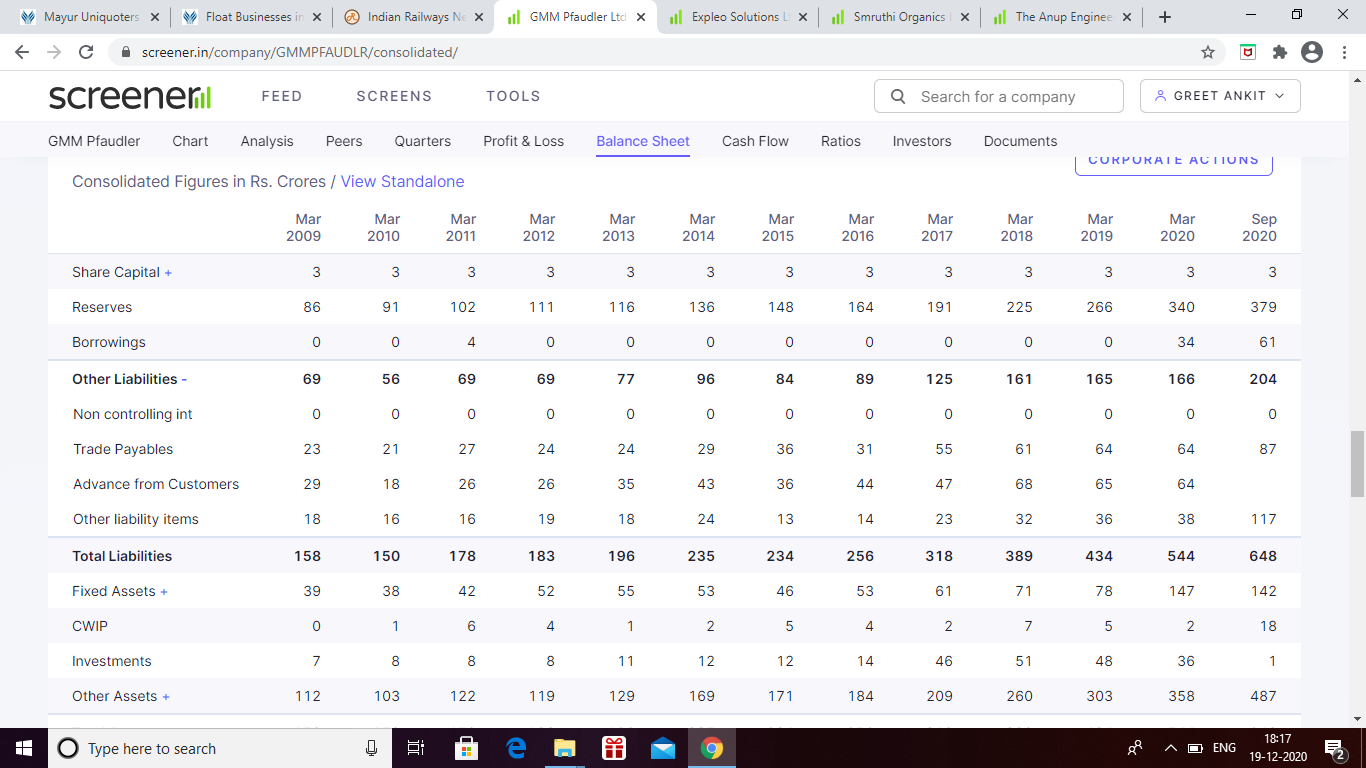

Yes…they get money in advance from ministry of defense plus a fixed margin of 7.5%…look at the cash in their books mazagon has 5000 cr cash with 54000 order book to be executed in next 5 years. All companies have negative working capital and earning huge interest income from the cash balances which are advance received.

1 Like

Just to spice it up…Prof. Sanjay Bakshi and Radhakrishnan Damani also own stake in it.

1 Like

True, MD’s other income is almost three times their operating income, and that is the problem. There is float and moat but no growth

1 Like

given that 54000cr order book there is hell lot of revenue and growth visibility here as they will be done over next 5-7 years. Also, remember they are sitting at a very strategic location at mumbai with 100 acres of land

Maybe this plays out the way you think it will, and I hope it does. But my experience with these kinds of businesses (with the government as the chief client) is that the order book is usually a pie in the sky kind of number. There will be delays, cancellations, reorganizations etc etc and this number rarely fully translates into actual revenue in the said timeframe.

That said, the downside risk does seem limited given the valuations and the secure nature of the moat

3 Likes

Here you go…RK damani and Ramesh damani enters Mazagon Dock with 40 lk shares with 2% shareholding = 70 crore investment

4 Likes

Fascinating. Was this investment made at the IPO price or post listing?

It seems like there is something going on shipbuilding businesses. First they bought into Cochin Shipyard Ltd now this.

(If you read the latest concall the first person to ask questions is Mr. Ramesh Damani. He is just stuck on one question: Will the company be able to grow at 20% for next 10 years?)

3 Likes

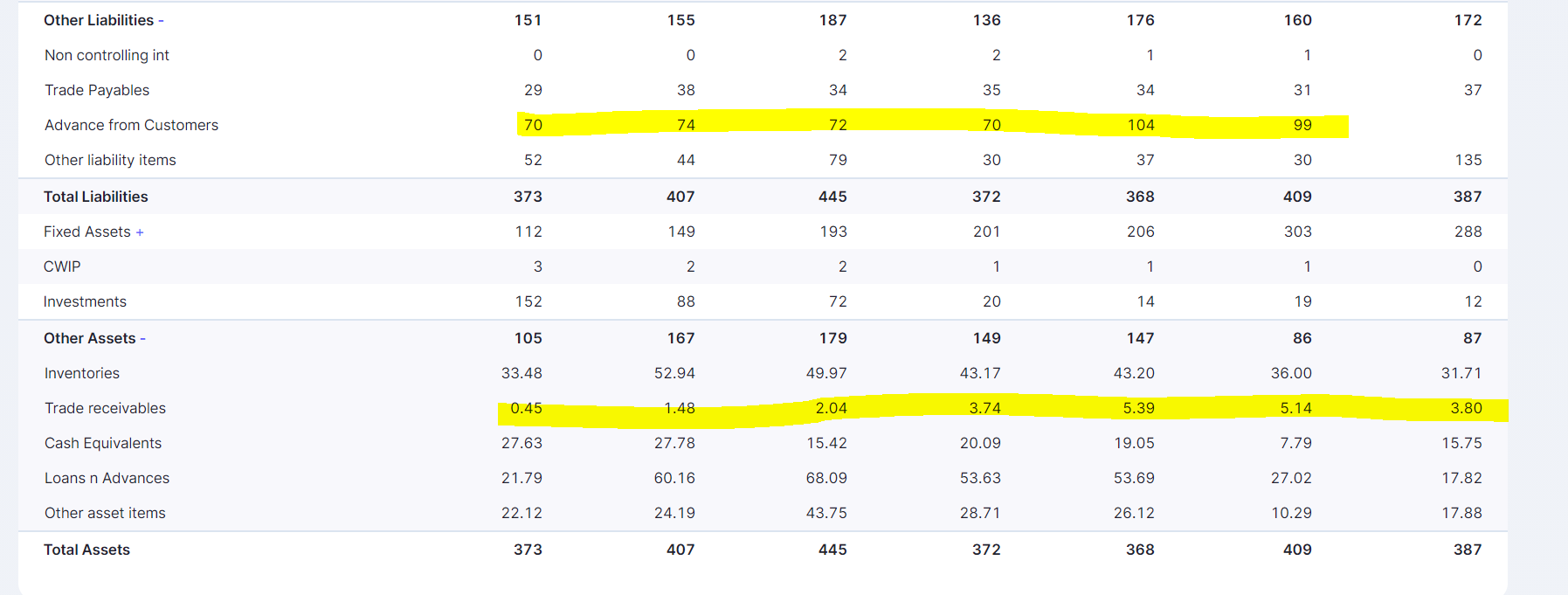

Well on a comparitive bases, doesn’t Cochin Shipyard seem more efficient - lesser cash on books, better receivable cycles, higher dividend, better top and bottomline growth and higher RoE?

Order book for both companies is large and expected to grow, but Cochin Shipyard seems to be better executioners

This is post listing purchase as they were not in the anchor list and in ipo no one got that much allotment due to huge oversubscription.

2 Likes

Yes, advance from customers is definitely considered as float money.

There is another company called isgec heavy engieering, you can read more about it on this valuepickr forum only, also the REIT companies… Which give thier office space on rental collect some advance deposits from their tennants, also another lesser known stock known as elnet tech, its similar to these rental companies taking advance from customers (similar to nesco as mentioned above)

1 Like

Other company which found with lots of float is Kaya

Huge amount of customer advances in relation to current asset…

Disc :: Not invested

2 Likes

Getting advance from customers is not the only way.

Float money is also through taking goods on credit from suppliers and getting cash from customers, that is the reason FMCG companies have an amazing business model.

I think VIP Industries too has some Float money which helps them cover some part of their operating assets.

Details in the thread: https://twitter.com/badola_arjun/status/1284027040249737216

Getting advance from customers is not the only way.

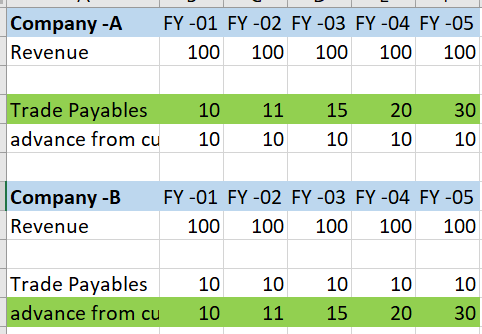

you hit the bullseye , right in a sense a good float business is the one which can make use of the others money for long duration for its advantage for free

regarding the credit from suppliers or trade payable -----------------I fell we must be very careful

because if the days trade payable keep on increasing then it means company-A(eg below ) is squeezing the suppliers.

this would result in (Company -A)

- sour relationship with the said supplier

- credit charge / late pay / finance charges

while if the company-B has the same trade payable over the years , but if the Advances from customer keeps increasing that means customer are willing to pay for company products in advance eg :: royal enfield → customers use to pay advance and wait for there bike

just my thoughts…

3 Likes

I agree, getting advance from customer seems a much better approach.

But the trade payable could also be because like the customers who are willing to wait same would be for the suppliers.

The supplier would be very interest to supply material to a like Hindustan Unilever as they know their changes of defaulting is very less and demand is huge. So, to remove other suppliers from competition they would agree to give supply on credit.

1 Like