Detailed article - https://www.moneycontrol.com/news/business/moneycontrol-research/ideas-for-profit-this-little-known-indian-firm-is-a-major-vitamin-d-ingredient-producer-3361251.html

Yet vitamin D supplementation has failed spectacularly in clinical trials. Five years ago, researchers were already warning that it showed zero benefit, and the evidence has only grown stronger. In November, one of the largest and most rigorous trials of the vitamin ever conducted—in which 25,871 participants received high doses for five years—found no impact on cancer, heart disease, or stroke.

How did we get it so wrong? How could people with low vitamin D levels clearly suffer higher rates of so many diseases and yet not be helped by supplementation?

As it turns out, a rogue band of researchers has had an explanation all along. And if they’re right, it means that once again we have been epically misled.

These rebels argue that what made the people with high vitamin D levels so healthy was not the vitamin itself. That was just a marker. Their vitamin D levels were high because they were getting plenty of exposure to the thing that was really responsible for their good health—that big orange ball shining down from above.

Sure enough, when he exposed volunteers to the equivalent of 30 minutes of summer sunlight without sunscreen, their nitric oxide levels went up and their blood pressure went down. Because of its connection to heart disease and strokes, blood pressure is the leading cause of premature death and disease in the world, and the reduction was of a magnitude large enough to prevent millions of deaths on a global level.

Weller’s largest study yet is due to be published later in 2019. For three years, his team tracked the blood pressure of 340,000 people in 2,000 spots around the U.S., adjusting for variables such as age and skin type. The results clearly showed that the reason people in sunnier climes have lower blood pressure is as simple as light hitting skin.

When I spoke with Weller, I made the mistake of characterizing this notion as counterintuitive. “It’s entirely intuitive,” he responded. “ Homo sapiens have been around for 200,000 years. Until the industrial revolution, we lived outside. How did we get through the Neolithic Era without sunscreen? Actually, perfectly well. What’s counterintuitive is that dermatologists run around saying, ‘Don’t go outside, you might die.’”

My personal opinion as stated earlier, Vitamin D pills may provide a marginal benefit especially for folks living in Northern latitudes (Europe and North America) with limited exposure to Sun.

Major benefit comes from being exposed to Sun which is free.

All things in life follow a U-Shaped curve. Too less is just as harmful as too much.

Most natural things restrict the “too much” dose. It is difficult for most persons to withstand sustained exposure to Sun, before he starts thinking about finding the nearest shade.

Same could be said of Salt or Water. Forcing oneself to drinking too much of water (overhydration) causes dilution of salt levels in blood leading to hyponatremia which can be fatal.

On the other hand, it is very difficult to over consume plain salt or with water without being repulsed by its natural taste.

Having said all of the above, like most things with misaligned incentives and top-down policy driven guidelines it needs a bottoms-up grassroots approach from the consumer patient to drive change.

On a side note, Vitamin D levels were found to be higher in longevity experiments on fruitflies and C.elegans. But is it a marker of good health as stated above rather than a cause for longevity?

Disc: Not invested. Posted as a FYI with good intentions.

Thank you for your good intentions, this is very helpful.

@hitesh2710 Your comments sir?

Some cutting from the dishman carbogen con-call on vitamin D business.They are into it big time and a new capacity will be on board this fiscal.But they say its more artificial manipulation which chinese companies are doing.

Question --> On the marketable molecule side of the business, we were into Calciferol some years back and

now because of the imminent shortages, there has been massive price increase and some of our

competitors are now benefiting. So, are there any plans or is it possible for us to get into

Calciferol now?

Mark Griffiths: That is one of the focus areas, as Arpit mentioned about the Soft Gel facility. So, that is part of

the strategy to leverage some of those. It is one of the reasons why the Netherlands business has

been doing so well.

Question --> Mark, that would be Calciferol, right?

Mark Griffiths: Calciferol, Calcitriol, Alfacalcidol, there is a whole bunch of this, probably 20 different analogs

of Vitamin D.

Question --> By the end of this fiscal year, do we expect to get our facility on track?

Mark Griffiths: Soft Gel, yes. The facility is due to be operational by the end of this fiscal year

Actually the Cholecalciferol market, the shortage was already seen by us two years ago. The

Chinese manufacturers create an artificial shortage in the market and we were in this

Cholecalciferol business before and that is exactly what was causing us difficulties. The

profitability of the Netherlands facility improved because of the change in strategy. So, this is

an opportunity for us in terms of going in the market and then again convincing more customers

by highlighting our engagements with the previous customers, ongoing customers now and how

they are benefiting from the contract.

Qtr ended Mar-17 Jun-17 Sep-17 Dec-17 Mar-18 Jun-18 Sep-18

Sales from Bulk Drugs -

Fermenta Divn 41.47 42.32 65.27 91.12 93.29 76.50 1 17.31

Commission on Sales-

Expenditure 0.31 0.66 5.31 9.23 5.02 5.44 8.53

PBT (Consolidated) 0.28 (3.41) 10.63 34.17 34.58 21.97 46.05

Sales Commission / Sales % 0.75% 1.56% 8.14% 10.13% 5.38% 7.11% 7.27%

Sales Commission as % of PBT 50% 27% 15% 25% 19%

DIL LTD - Analysis of Selling Commission

DIL Ltd’s Vitamin D products especially Animal Grade prices have risen internationally. This should give pricing

power to the company. But analysis of expenditure incurred on selling commission gives a different story. Usually

for pharma companies, commission on sales is less than 2 % of sales value (For Dishman, commission is less

than 0.05% of sales). This was the case with DIL until Jun 17 qtr.

After the rise in international prices of Vitamins, commission on sales has shot up disproportionately to as high as

10 % of sales. In a seller’s market where company has pricing power and good demand, commissions should be

flat or should reduce. Why should selling commission rise disproportionately?

More so, as Commission as % of PBT is also very high. Are we to assume that the company is paying very high

commission on incremental sales? Or is there any pilferage? Can anyone throw some light on this ?

Quarter result and detailed presentation on path forward:

Could any one clarify reason for loss in property segment and QoQ decline in topline incontrast to Dishman growth QOQ

AR 18-19 notes

- DIL holds 91.2 % In Fermenta Biotech, a merger is underway – will lead to better economies of scale , value accretion and efficiency.

- Executed a 99-year lease agreement for the acquisition of land aggregating about 40,000 sq meter from the Gujarat Industrial Development Corporation (GIDC) authority in Ankleshwar, Sayakha, f or expansion and new projects

- Revenue of company was 417 cr vs 312 cr yoy; operating profit was 161 cr vs 102 cr yoy.

- Operating margin jumped 39 % with respect to 32 % yoy.

- Net debt to equity dropped drastically from 0.98 to a comfortable 0.42.

- Debtor days improved greatly from 80 days last year to 57 .

- China’ s Blue Sky policy caused many of the factories to be shut down – this caused 4 fold rise in animal feed vit D realizations. Due to this the company had 50 percent of animal feed in their product mix as against 15 percent earlier.

- Human nutrition realization also strengthened by 7 % this year.

- Company invested 12 cr in 18-19 and will further invest 65 cr in 19-20 in increasing its manufacturing capacity.

- Exited the entertainment and wellness business by writing down accumulated losses

- the market of Vitamin D3 is growing in scale and scope as new downstream applications are being continuously developing ; at the same time the number of players is not increasing beyond a handful due to the high entry barrier.

- Company has an aspiration to grow by 15-18 % CAGR for next 5 years.

- They believe they can get a higher share of the animal feed market.

- DIL acquired 21.05 % of equity held by private players in Fermenta this year taking their total to 91.2%.

- Additional capacity at Dahej will be effective from Oct 2019 and at Sayakha from Dec 2020

- The Company’s credit rating strengthened from BBB to A- (for longterm debt), moderating debt costs and enhancing corporate respect.

- The company is very optimistic about the size of opportunity in vit D market – due to rising awareness among people about vit D deficiency.

- Vit D business revenues jumped to 316 cr vs 228 cr last year. Company developed rodenticide product gained momentum.

- Fermenta developed a new formula using spray drying technology for Vitamin D3 feed manufacture, enhancing product stability

- Introduced offerings in the competitive food pre-mixing segment in regulated markets

- Tied up with an European manufacturer for exclusive sales of Vitamin D2 in India for DNS and food applications

- Received approvals from international customers and initiated supplies of Vitamin D3 from Dahej, allowing the Company to enjoy taxation benefits (facility located inside SEZ)

- Company’s biotech division showed massive growth ( on a small base) from 5.7 cr to 13.8 cr. Company manufactures enzymes in this segment

- Company’s pharma segment was flat with around 47 cr revenue this year.

Overall I feel the company delivered great number aided by macro factors. The profit margins might nt be sustainable but the increase in capacity and the huge opportunity size might make things interesting. The volume growth in vit D for the next few years can make up for the dip in margins going ahead. Also the company exiting its loss making businesses is a big positive.

Disc- Invested

Thanks

Did you check their merger with Fermenta ?

How many shares are they are issuing Fermenta’s non Dil share holders to acquire Fermenta completely and merge with the main business ?

Total Revenue (including other income) at Rs. 84.09 Cr as against Rs 83.45 Cr in Q1 FY19

EBITDA (including other income) at Rs. 27.42 Cr, margin is at 32.6%

PAT at Rs. 14.06 Cr as against Rs 16.68 Cr in Q1 FY19

plant had remained shut for one month for maintenance and debottlenecking

post this debottlenecking the production capacity will improve by 15 %.

The prices of Vitamin D3 for Animal Feed have shown weaker tone as compared to earlier

quarters.

Recently one of our largest Vitamin D3 customer has indicated that due to technical issues at their production facility, they would not be able to manufacture their product till the end of this year, therefore we anticipate a decrease in Vitamin D3 Animal Feed demand for the coming few quarters from this customer.

Looking at the demand for Vitamin D3 backed by growing awareness, we continue to believe that the volume will continue to grow at 15-20% CAGR over the next 5 years.”

overall the results are very encouraging. it is good to see that since the prices in animal feed were weaker the company substituted that by having a larger chunk of revenue from human side compared to last year.

Disc - Invested

I had attended the AGM of the company earlier. Sharing the summary:

We are concentrating on Nutrition. Vitamin D also falls in the nutrition category. Going forward, we want to expand the product basket.

We are undertaking 60-70 Cr Capex and it should be completed by year end. It will be a multi-purpose plant. D3+ some new products.

We supply to 55 Countries.

R&D - We have shifted from 7000 sq ft to 15000 sq ft. Look to spend 15 Cr on R&D vs about 7-8 Cr earlier.

3-4 competitors outside India. We are the only one from India. Outside China there is only 1 competitor - DSM.

Human Side - We have 25% market share. Its a much more stable business. We are sole suppliers to some companies and have better control.

For this year, we see realizations closer to what we saw over last 2 years. They have fallen from peak but they are still very good. If the current prices or even a bit lower range remains, we can maintain current margins.

Commission on sale is a variable payout to distributor based on certain pricing and volume.

We have healthy mix of long term and spot contracts.

Shutdown of 1 month was there but we should be able to make up by de-bottlenecking.

80% export, 20% domestic.

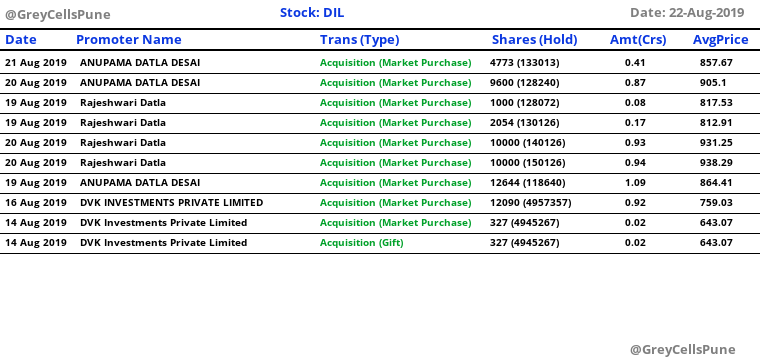

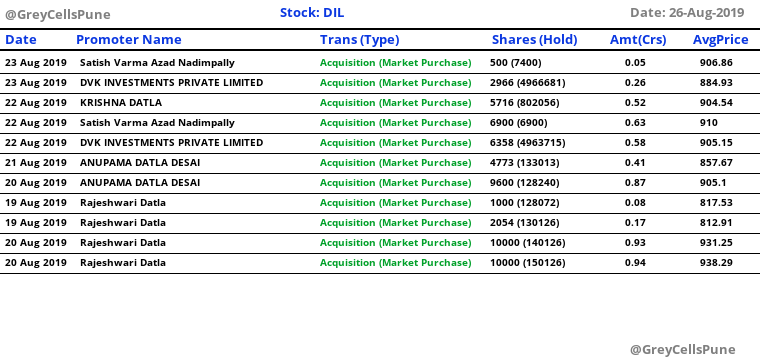

Promoter has bought shares even they buying continuously . This shows lot of confidence promoter has in the outlook of future business.

Why promoters same relatives buying almost every week ? Why not single time ? Any restriction on investing amount for promoters ? Or because of stock liquidity ?