GSK growth has almost disappeared. It will continue to be very low looking at trends in West.

ITC is far superior option. A lot of FMCG launches especially in Food categories.

GSK growth has almost disappeared. It will continue to be very low looking at trends in West.

ITC is far superior option. A lot of FMCG launches especially in Food categories.

Thank you for the prompt response. Will look into ITC in detail. The valuations are compelling but I need to develop that conviction before i could go and buy. Need to read and learn more…! Thanks again…!

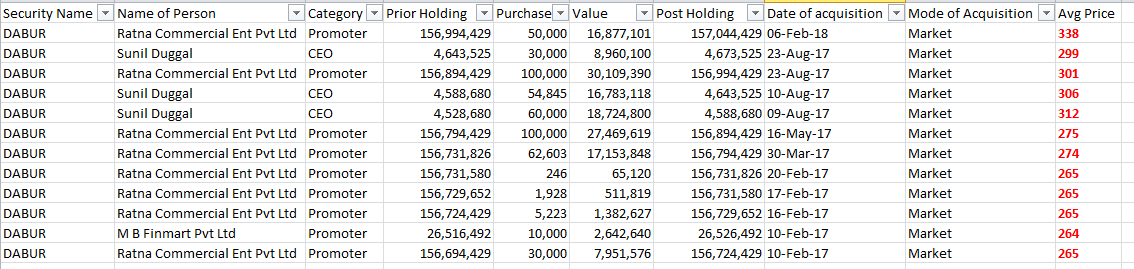

While this information is delayed, still I thought worth to share it in this forum.

Dabur promoters and CEO have picked-up the shares at around Rs.300-305 range. From that the price has already run up by around +10%.

sir, unable to download/view the excels shared above/earlier post. Any way to find/restore those links.

Itc - if you look at profits from cigarette vs rest of itc profits, the second draws a blank! I think itc is a buy at current levels just due to tobacco play. Other fmcg launches are not contributing anything to pat despite contributing significantly (30%) to revenue.

Valuationwise, nothing is cheap now in this sector…all good players like Nestle, Britannia, HUL, Marico, bajaj, godrej, and few others all are trading at astronomical valuation. I see good growth in Nestlé and Britannia and other dairy companies (hatsun and heritage) ahead but think vis a vis valuation. If one is already invested from lower levels, this sector is a hold. But buying now i don’t think will be rational seeing extremely low growth and high pe despite longetivity. When i look at adf, dcm, pratap snacks, i always wonder market is ignoring, all the risks in their business. Discounting next 5-8 years of earnings growth without any black swans or competition.

Disclaimer - invested in hul, nestle. No transaction in last 3 years.

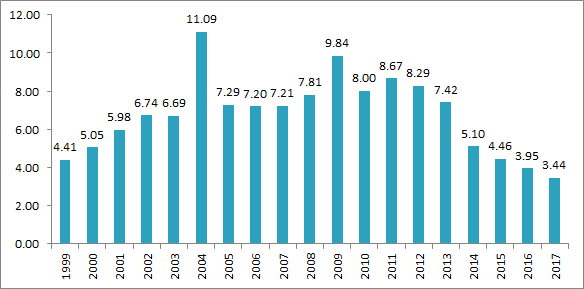

Attached is the FA turnover ratio trend for colgate for the past 19 years.

As you can see the FA turnover has been dropping since 2011-2012 to about 3.44 as on 2017. The reason behind this is the substantial investments made in the net block over this period. Net Block has increased by 5x since 2011. However sales has increased by 2x. The average over this 19 year period is at ~7 peaking out at 11. Currently the FA turnover at 3.44. The thesis is that the FA turnover will revert back to its average during which operating leverage dynamics will play out. If this happens then the PE at which Colgate is available looks optically high and could present an interesting opportunity.

Best

Bheeshma

Disc - invested, Forms about 10% of portfolio.

**

**

Operating Revenues (Sales) have been stagnant for past two years, which is alright considering GST and notebandi. However, earlier to that, Operating Revenues had grown, consistently, by 10% YoY, and that is an attractive number for a great management like that of ColPal.

Moreover, ColPal is often available at PE of below 40. Accordingly, a correction of 20% from current levels will make the share price attractive, and add to this a prospect of 10% growth, makes a great investment for years to come.

Current PE is 53. A very high number looking at the historic PE levels.

**The Columns are in reverse order. The First Column is of 2017 the last one is Mar-12

Hi @jamit05

The PE is to be adjusted for normalized earnings. The investments in assets will produce revenue but with a lag. In my view, the PE ratio looks high but at a normalized level its much lower. The per capita consumption of toothpaste is pretty low in india at 176 gms. In countries like brazil per capita levels of tootpaste consumption are 3x of india. The penetration is 90% for urban india and 63% for rural. Colgate has a market share of 50-55% in india. Several toothpaste brands have tried to take market share over time but have realized quickly that its pretty difficult. Dental hygiene is very poor in india in general. Of course the competitive landscape will keep changing with new entrants in this space but broadly people are habituated to a particular brand of toothpaste and dont change often over their lifetime.

Best

Bheeshma

Could you elaborate or may be present a PE based on estimates.

Hi @jamit05

Using average historical operating ratios - the EPS is expected to be about Rs 50. I have assumed a Net Profit Margin of 15% ( which is the average of the last 10 years ). Based on this the PE multiple on a normalized basis comes to ~ 23. The 2017 EPS was 21 - so clearly i expect an increase in earnings power of about 18-20% over the next 5 years ( or 10% over the next 10 years ). The company also has an excellent capital structure - which acts as a floor PE - which i believe to be in the range of 25-28. In a worst case scenario i dont think the PE will go below that. If assumptions pan out as expected it presents a safe risk reward opportunity.

Best

Bheeshma

Does anyone track Sampre Nutrition. This is a microcap FMCG player and is basically a Candies manufacturer and recently launched new flavors of their candies. It was an outsourcing partner of companies like Dabur, Mondelez and more recently their biggest customer patanjali, but with launch of their own candies, i believe it needs due attention and research from FMCG lovers. Its headed by first generation entrepreneur who happens to be the Chairman of Indian Confectionery Manufacturer Associated (ICMA) also (recently re-elected as chairman) and therefore, he comes with credibility. Disc- Invested.

Yes I do.sampre nutrition had been a contract manufacturer for major players all these years.with new contracts with patanjali & mondelez,the business turnover is going to see a quantum jump.having said that,their intention of selling hard boiled candies in their own brand is a major breakthrough in itself.This is because,the company had maintained very good name in quality & also has good experience in product variety…so one can expect their products to go well in the wider markets.also it is a high margin segment within the confectionery space.so there is a huge value unlocking waiting to happen in this counter even as the results should be able to speak for itself in the next few quarters.with a small equity base,it can do wonders.

Invested.

How do you view it with PE> 80 , RoE< 5 , D/E > 1.3

Lykis limited is the fastest growing Home & Personal care Company in India. Its presence pans across the Beauty & Grooming segment, Homecare segment, Food &Beverages segment, Health &Wellbeing segment. These include an enviable portfolio of brand names such as Lykis, Britex, Rox, Bonita, Vogly, Tazaagi, Cheers, Alivio, etc.

From its humble beginning with the object of managing tea plantations, manufacture of quality tea sale & export of tea both in domestic & overseas market. Lykis Limited was incorporated on 15th October 1984. The company has come out with its IPO in the year 1995 with an equity issue of Rs 3, 60,000 shares. It is also a BSE listed company. The company has now diversified its business & has launched multiple products under various brands & is marketing these products from Mumbai branch.

We have a portfolio of 1000+ Sku’s products. Rox deo, Perfume, Talc, Shower gel , Shaving cream, Lykis soap, Deo, Perfume, Shampoo, Hair oil, Coconut oil, Bonita beauty soap , Cream & Lotion etc. Britex dish wash bar& liquid, Britex Airfreshner, Britex floor cleaner, Britex toilet cleaner, Britex glass cleaner to name a few. Our current operation comprises in 36 countries including African countries, CIS countries, USA, UK, Haiti & Middle East countries. Lykis is dealing in qualitative products by ensuring a strict check on quality control where every product undergoes close scrutiny before dispatch. In the financial year 2012-13 we have been awarded for “Best Debutant ExporterOf The Year”

Lykis limited is a vibrant company with bold ambition & are becoming more agile & future ready. We are constantly innovating to delight our consumers with more exciting, superior quality products at affordable price. The company insists on honesty, integrity & fairness in all aspects of its business & expects the same in its relationship. We work to create a better future everyday & help “People look good, feel good everyday with brands that are good for them”.

Our transparent business practices, fair dealings, wide distribution network, timely delivery, client centric approach & cost effective price structure have earned us vast appreciation of customer base spread all across the globe.

Highlights

The Company owns a tea garden of 952 Hectares named ‘Iringmara Tea Estate’ at Cachar, Assam. About 400 Hectares of the same area is presently, under tea cultivation. Iringmara Tea Estate is located at National Highway and is just 30 Km from Silchar town which in turn gives easy accessibility to the markets.

It has been more than two decades since the establishment of the Company and its entry into the Tea plantation business.

The Tea Garden is spread over 2150 acres area of freehold land.

The Tea Gardens of the Company are located strategically amidst the best of such estates in Assam.

The company has in place various channels for the sale of its tea both in the local market in Assam and outside the state of Assam.

Once their new initiatives come into play,the nos should stabilize better,though debt levels are expected to go up due to planned capex of 35crores announced recently.

small cap investing is not about looking at ratios but looking at the secular trend of business. If the ratios were good then the business would have been well discovered and why would it then be available at such cheap valuations - market cap to sales (as it is FMCG company). It has grown almost 15 times its sales in last 12 years, albeit on low base. It has bagged some big contracts from big customers which give it earnings and growth visibility and most importantly the launch of its candies is a game changer. One has to understand the business to value it in entirety.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/50bcb333-c158-404d-8d7e-7e5c4a255a81.pdf

Very strong set of results from Colgate.

Dear Members,

I am pretty much new to investing world just picking up knowledge from this valuable forum.

my bro earlier used to manage this company sampre nutrition as part of his job, do you need any specific info which can i try to source from him.

Thanks

Regards

Jithesh V