Extracts from Fairfax Shareholders Letter: https://s1.q4cdn.com/293822657/files/doc_financials/annual_reports/2018/Website-Fairfax-India-2018-Shareholders-Letter.pdf

Fairchem Speciality (Fairchem)

In March 2017, the previously announced merger of Fairchem Speciality and Privi Organics (Privi) was completed,

resulting in Fairfax India owning 48.8% of Fairchem. Fairfax India had earlier separately owned controlling interests

in both these companies.

Based on IFRS, for the year ended December 31, 2018 the consolidated Fairchem entity grew revenue by 37% to

$194 million and net income by 71% to $10 million. Shareholders’ equity grew 13% to $74 million, generating an

ROE of 13%.

While the two businesses have been merged into one corporate entity, they each continue to be managed

independently by their founders and existing management teams. We describe below the performance of the two

businesses:

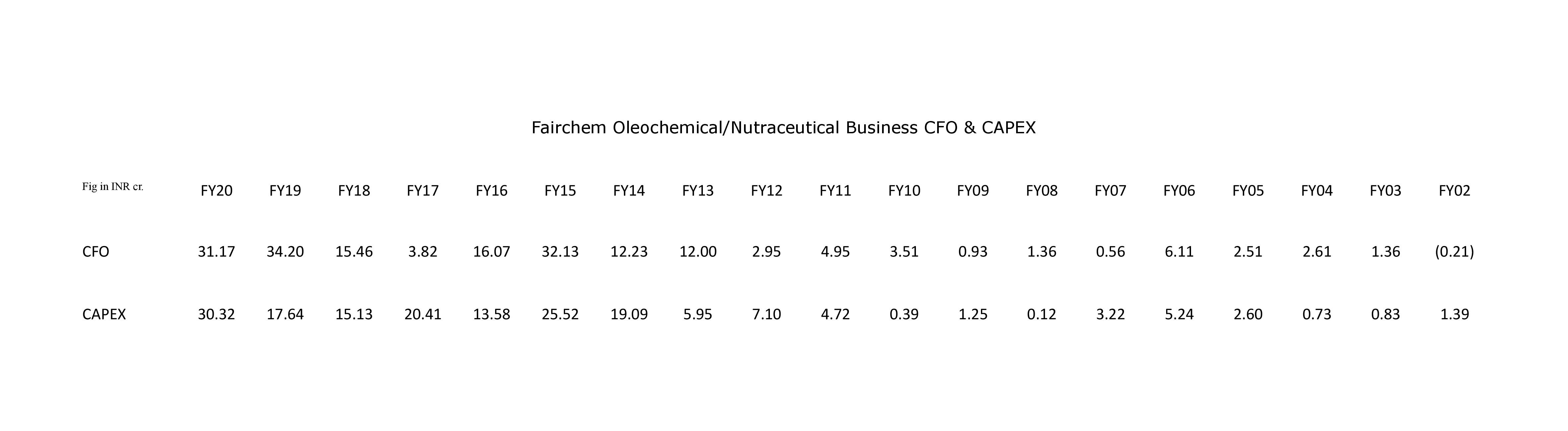

Fairchem (formerly Adi Finechem): Fairchem, led by Nahoosh Jariwala, is an oleochemicals company.

Oleochemicals are, broadly, chemicals that are derived from plant or animal fat, which can be used for making both

edible and non-edible products. In recent years the production of oleochemicals has been moving from the U.S. and

Europe to Asian countries because of the local availability of key raw materials.

Fairchem occupies a unique niche in this large global playing field. It has developed an in-house technology that uses

machinery manufactured by leading European companies to convert waste generated during the production of soya,

sunflower, corn and cotton oils into valuable chemicals. These chemicals include acids that go into non-edible

products like soaps, detergents, personal care products and paints, and other products that are used in the

manufacture of health foods and vitamin E. The company’s customers include major multinational companies

including BASF, Archer Daniels Midland, Cargill, Arkema and Asian Paints. Fairchem operates out of a single plant in

Ahmedabad, the largest city in Gujarat, the home state of Prime Minister Modi: the plant has one of the largest

processing capacities for natural soft oil-based fatty acids in India. Over the last ten years Fairchem’s sales have grown

on average 24% per year, net earnings have grown on average 33% per year, and the average annual ROE was

around 19%.

Based on IFRS, for the year ended December 31, 2018 Fairchem revenue grew by 4% to $37 million, net earnings grew

by 65% to $3 million, and shareholders’ equity grew 22% to $14 million, generating an ROE of 24%.

In 2018, Fairchem implemented changes in its plant that further debottlenecked its operation and optimized the

production process. These changes have resulted in increasing installed capacity from 45,000 to 72,000 metric tons

per annum (MTPA) of raw material that can be processed. In 2018 Fairchem processed 39,000 MTPA implying a

capacity utilization to year end capacity of 54%. This provides considerable room to grow since the plant can operate

13

FAIRFAX INDIA HOLDINGS CORPORATION

at up to 90% of installed capacity. Fairchem has also initiated two capital expenditure projects: both will be financed

by a mix of term borrowings and internal accruals and are expected to enter production in 2020:

• a plant to manufacture sterols and higher concentration tochopherols; and

• a plant to manufacture bio-diesel using three by-products of its manufacturing process: palmitic acid,

monomer acid and residue.

It has been a year of significant achievement for Fairchem.

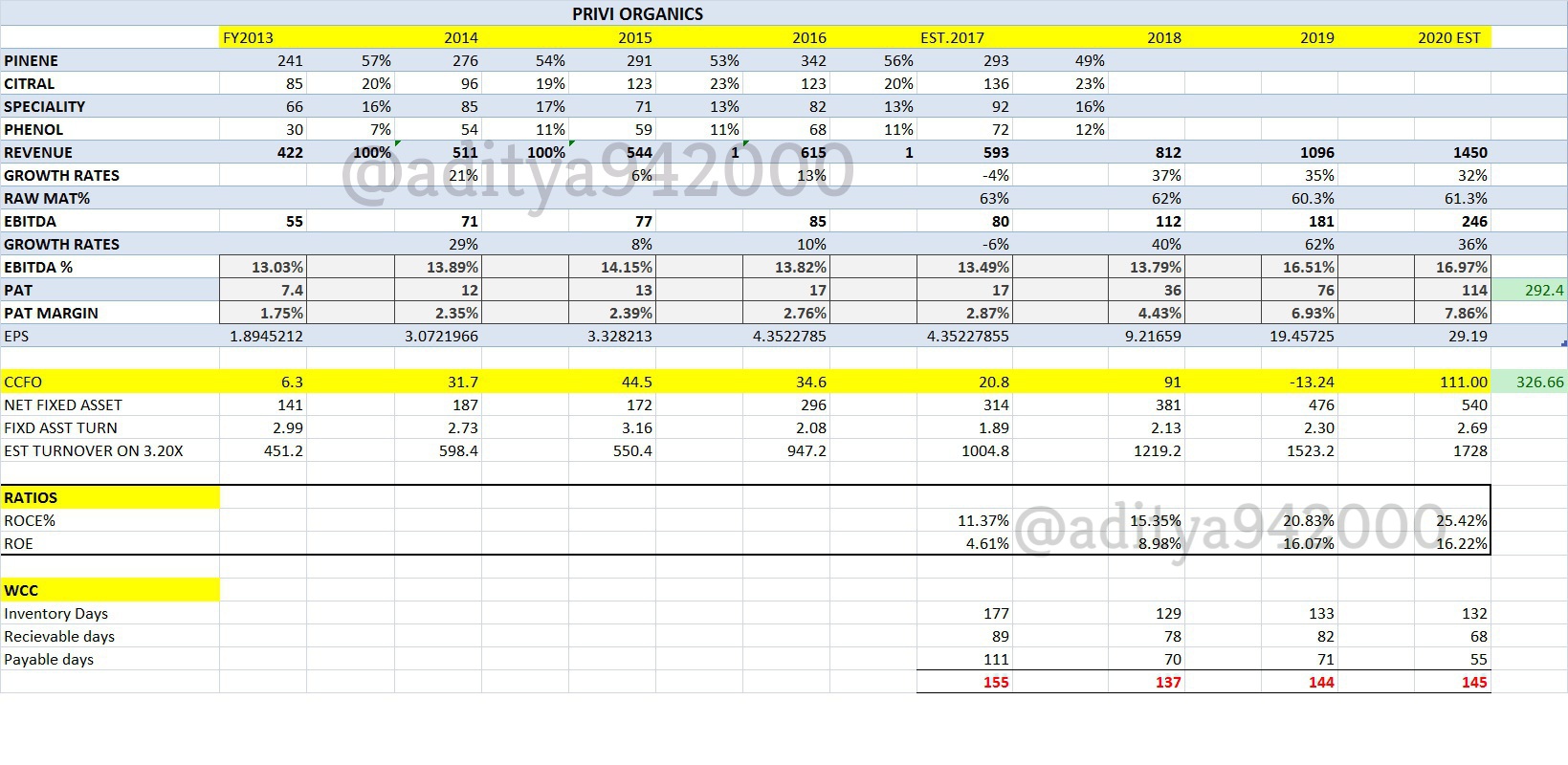

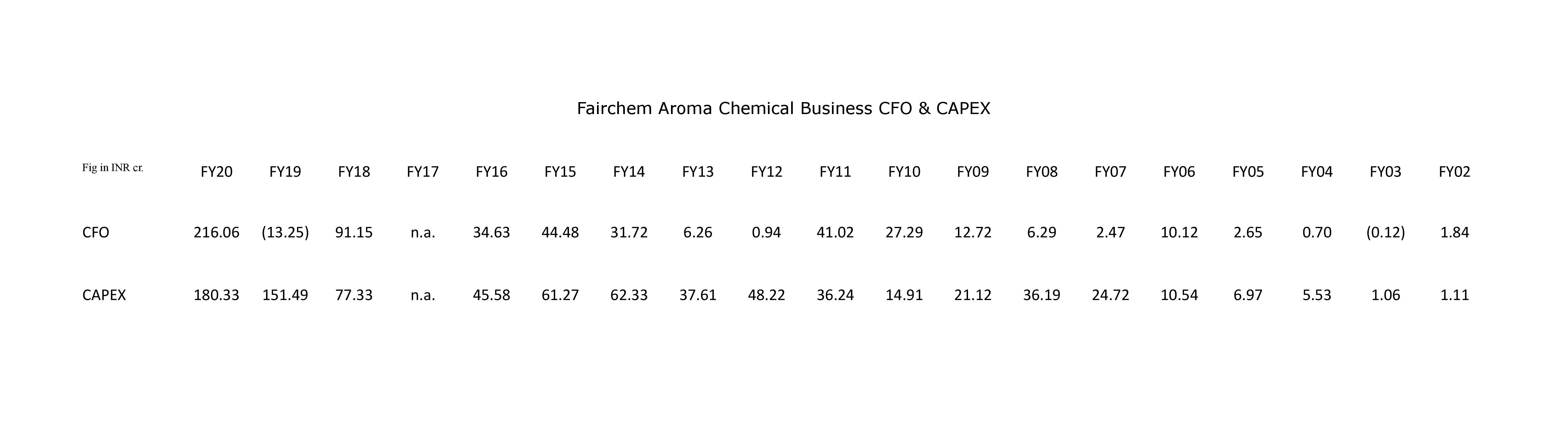

Privi: Founded in 1992, Privi, led by Mahesh Babani and D. B. Rao, is one of India’s leading manufacturers of

aroma chemicals. Privi started manufacturing aroma chemicals with only two products, which it gradually expanded

to a range of over 50 products today, with a capacity of over 27,500 tonnes per annum. Its products are used as

fragrance additives in perfumes, soaps, shampoos and packaged food. Privi enjoys a dominant position and

economies of scale in its product categories. Privi also develops and produces custom-made aroma chemicals to

specific requirements of its customers. Privi sources most of its raw materials from pulp and paper companies globally

and competes primarily with pure play and niche suppliers such as IFF, DRT and Renessenz.

One of Privi’s significant strengths is its established research and development capabilities in aroma chemicals, with

a staff of 81 people comprised of PhDs in chemistry, chemical engineers and instrumentation engineers. The research

specialists continuously strive to develop new products and processes. Importantly, one of the R&D labs is

completely focused on developing, through biotechnology, green products and green technologies in technical

collaboration with the University Institute of Chemical Technology, Mumbai.

Privi has made significant investments in manufacturing facilities that convert a waste product in pulp and paper

manufacturing, crude sulphated turpentine (CST), into aroma chemicals. CST, a more cost-effective raw material

than the more traditional plant-based gum turpentine oil (GTO), is procured through annual contracts, while GTO

has to be purchased on volatile spot markets.

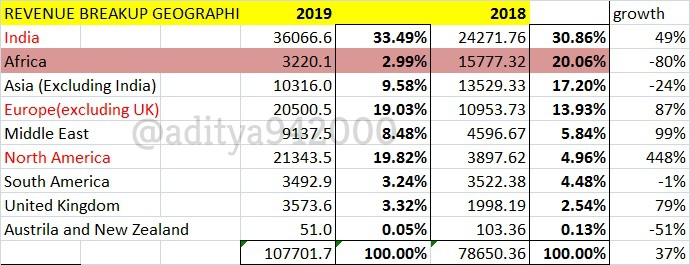

Based on IFRS, for the year ended December 31, 2018 Privi revenue grew 48% to $157 million, net earnings grew 59%

to $6 million, and shareholders’ equity grew 11% to $60 million, generating an ROE of 10%.

This is quite a remarkable result when you consider that on April 26, 2018 there was a major fire at Privi’s main

production facility. While it is fortunate that there were no injuries as a result of the fire, the fire completely gutted

critical production units that impacted all production, all of the raw material and finished goods warehouses and the

administrative offices. The entire plant including the production units that were not affected by the fire had to be

temporarily shut down. However, Privi was able to open the facility and start operating the plants not affected by the

fire in a record time of 29 days. Using third party production facilities in combination with its own production units

unaffected by the fire, Privi was able to start supplying all of its products by June 2018.

Around the same time there were fires in two other plants that produce products similar to Privi’s, resulting in an acute shortage of certain aroma chemicals and consequently in much higher prices and margins.