Rather than posting only conclusion/derivation, have instead chose to put here above stated 20 Years’ varied data points analysing a company from different angles, so that VP members can use them to arrive at their own analysis and derivation. One person’s thinking can be limited and its the collective thinking of all of us which makes us arrive at right conclusion. What I have understood from my analysis is stated below and its only my personal understanding I have used to invest in the company and no one should rely on this. I will be delighted if more members use these data points and put their own analysis on VP so we all can learn from each other’s strengths and correct each other’s weaknesses.

My Understanding :

When this thread was initiated in VP in July 2014 by Jatin Kalra, the heading was a question “A good business or business having a good time ??”. If we analyse company since inception, i.e. if we analyse past 20 years since the company has existed in current form, business doesn’t seem to be bad atall. But, the question is whether its a good business or its the good management of an ok business. Answer lies in two things :

Maintaining the same line of business and carving out success from it,

Technological Advantage.

Maintaining the same line of business and carving out success from it :

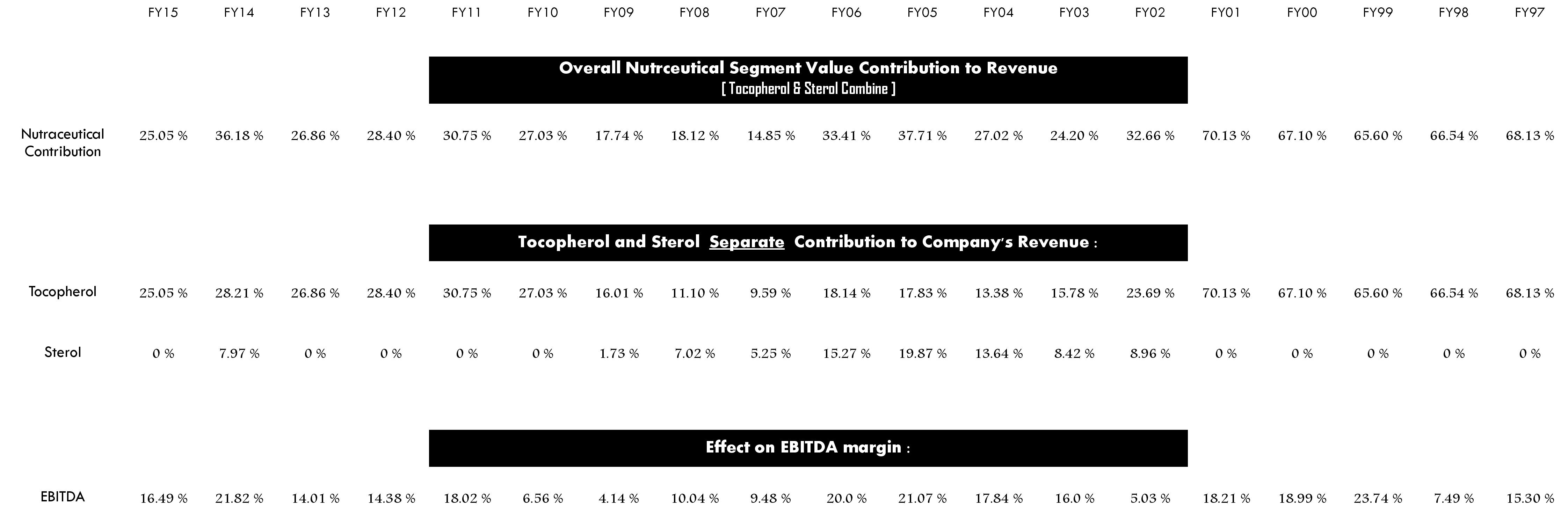

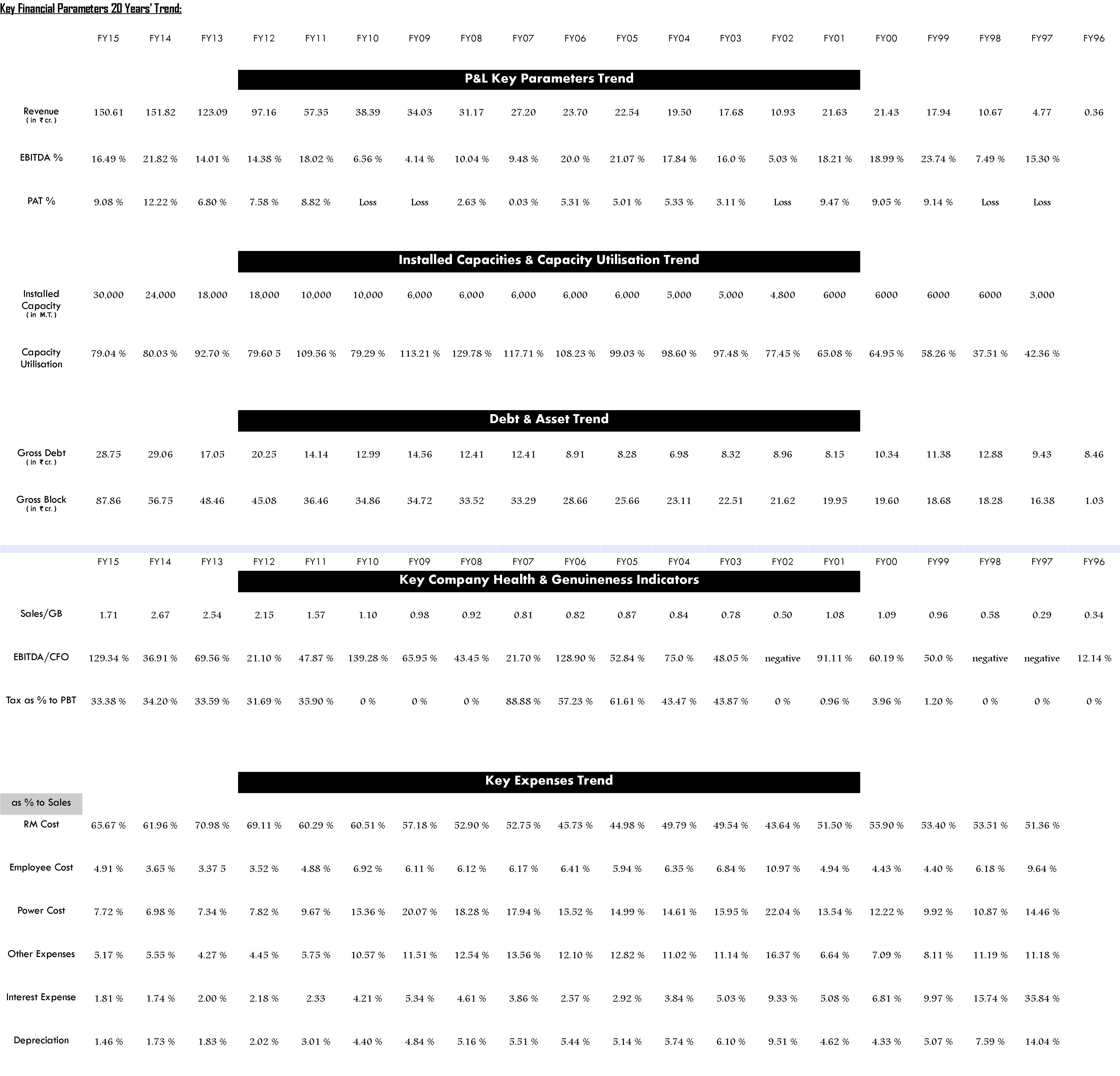

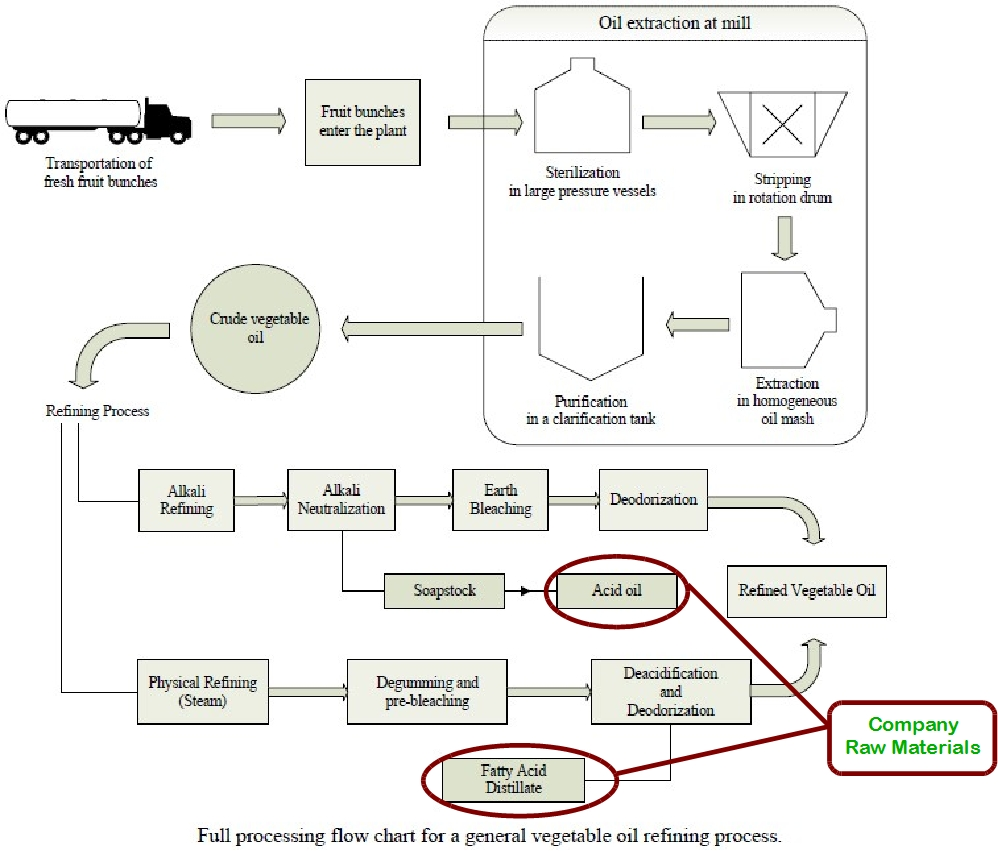

I like those companies who don’t change their line of business despite many ups and downs faced and infact utilise downs to bring out best in themselves. Adi Finechem perfectly fits this criteria. Since FY96, company has focussed on using byproducts of vegetable oil processing to produce niche products – first it was tocopherol then sterols then dimer acid and slowly it seems to be moving up the value chain. Over these many years, it has also focussed on profitability which is evident from sustenance of EBITDA margins despite all odds. It weathered ending of exclusive production offtake contract, it weathered the difficult RM procurement stage, it weathered sudden severe RM price increases too.

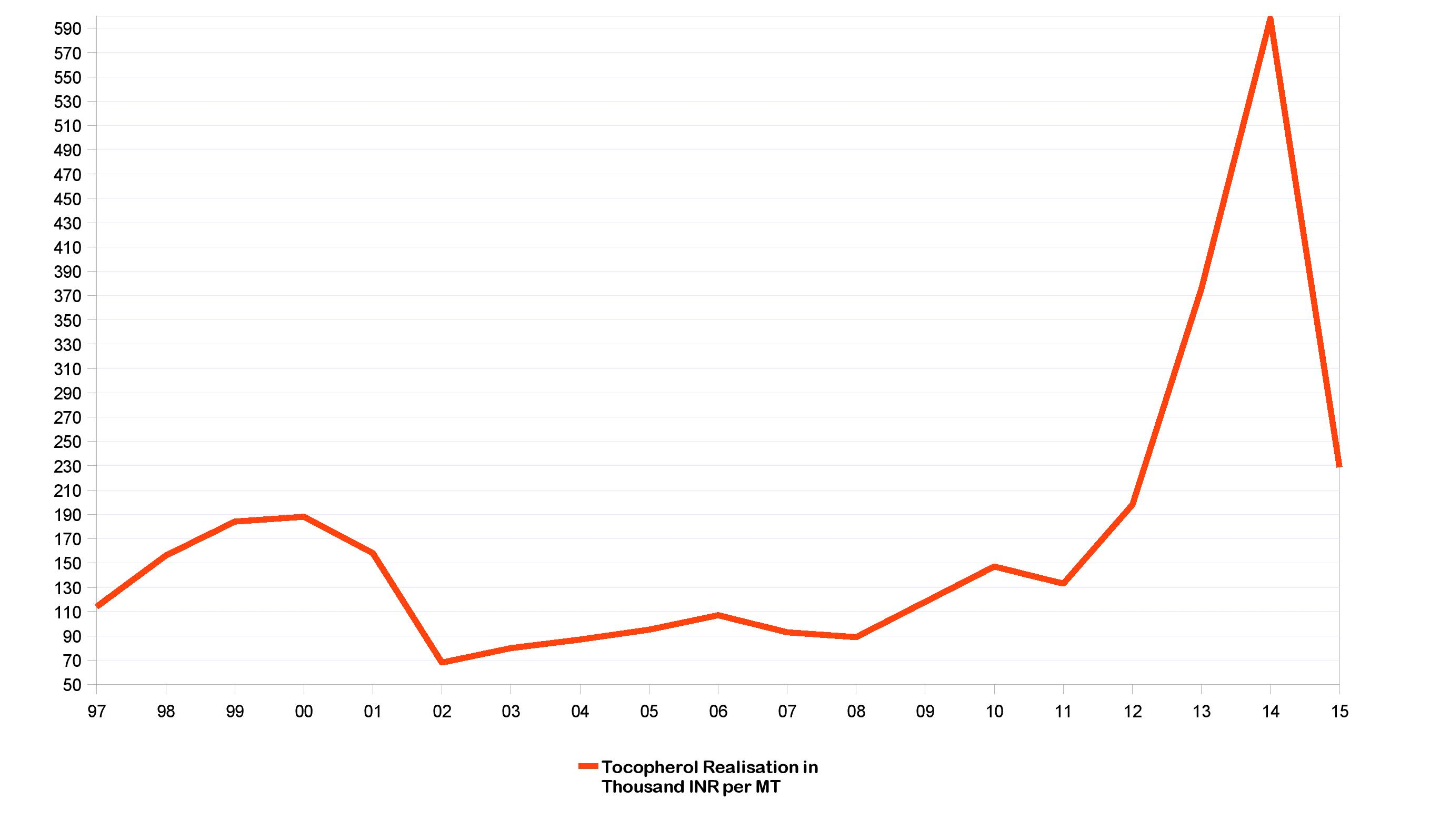

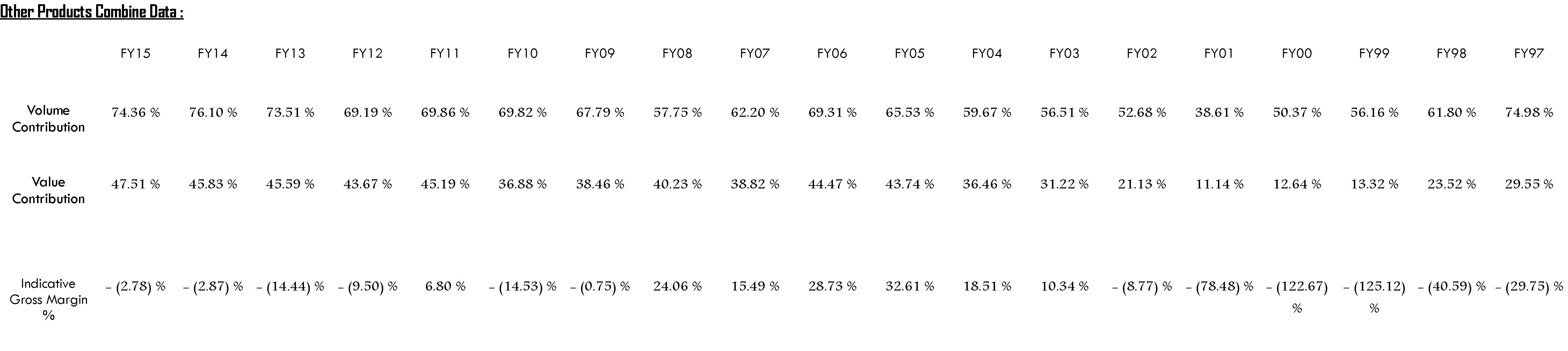

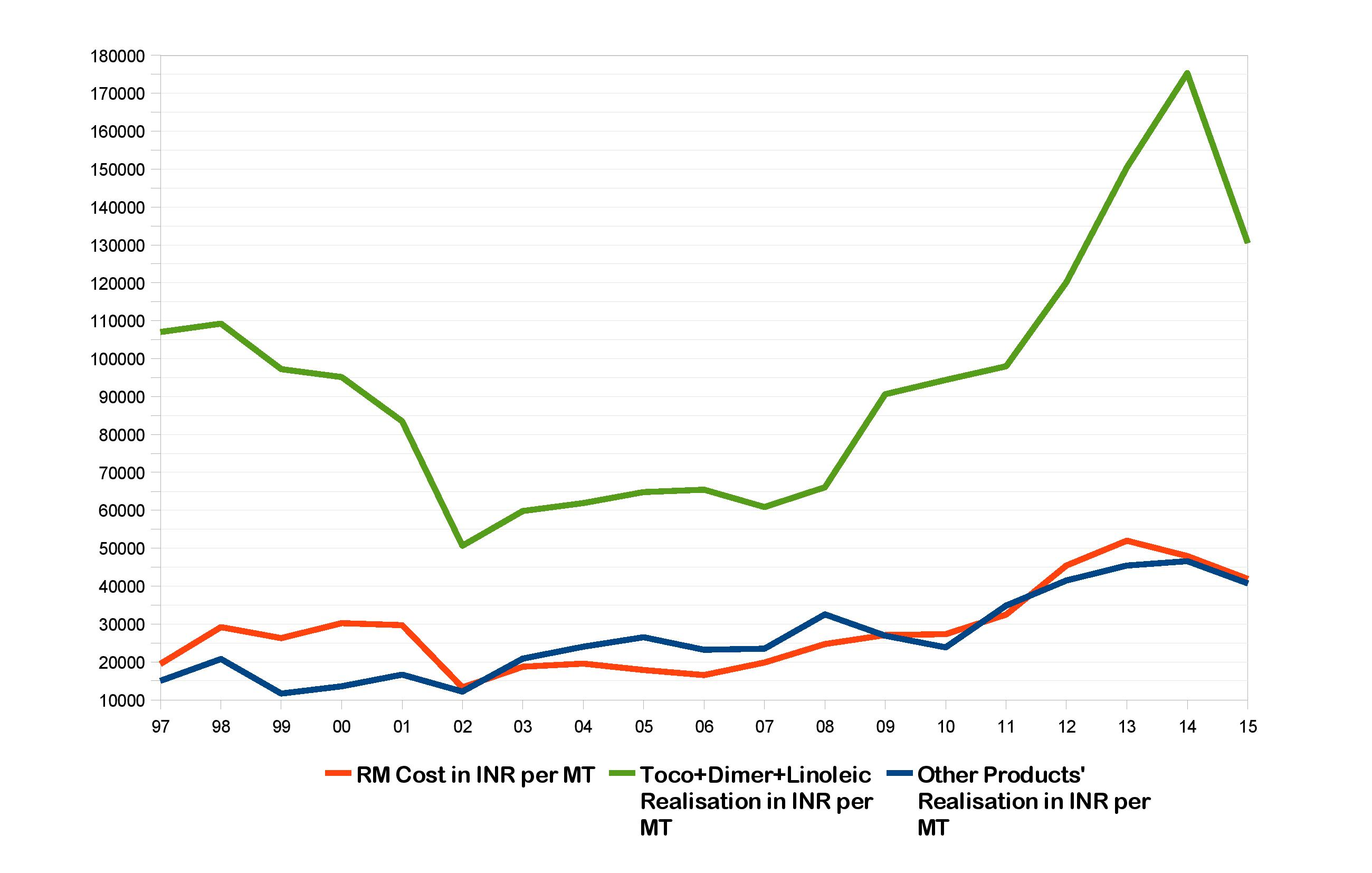

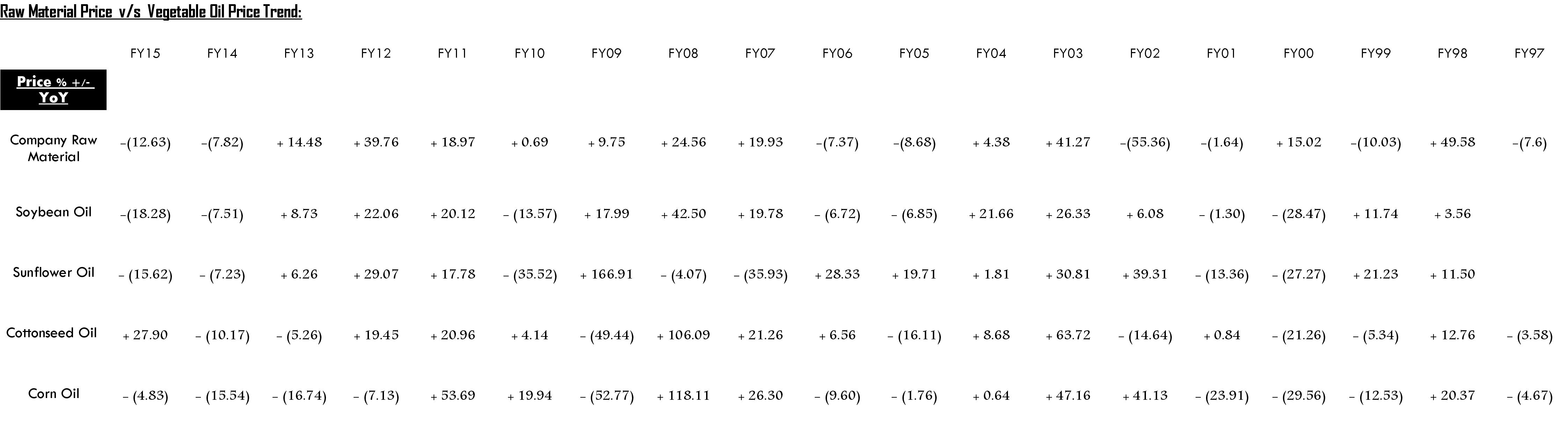

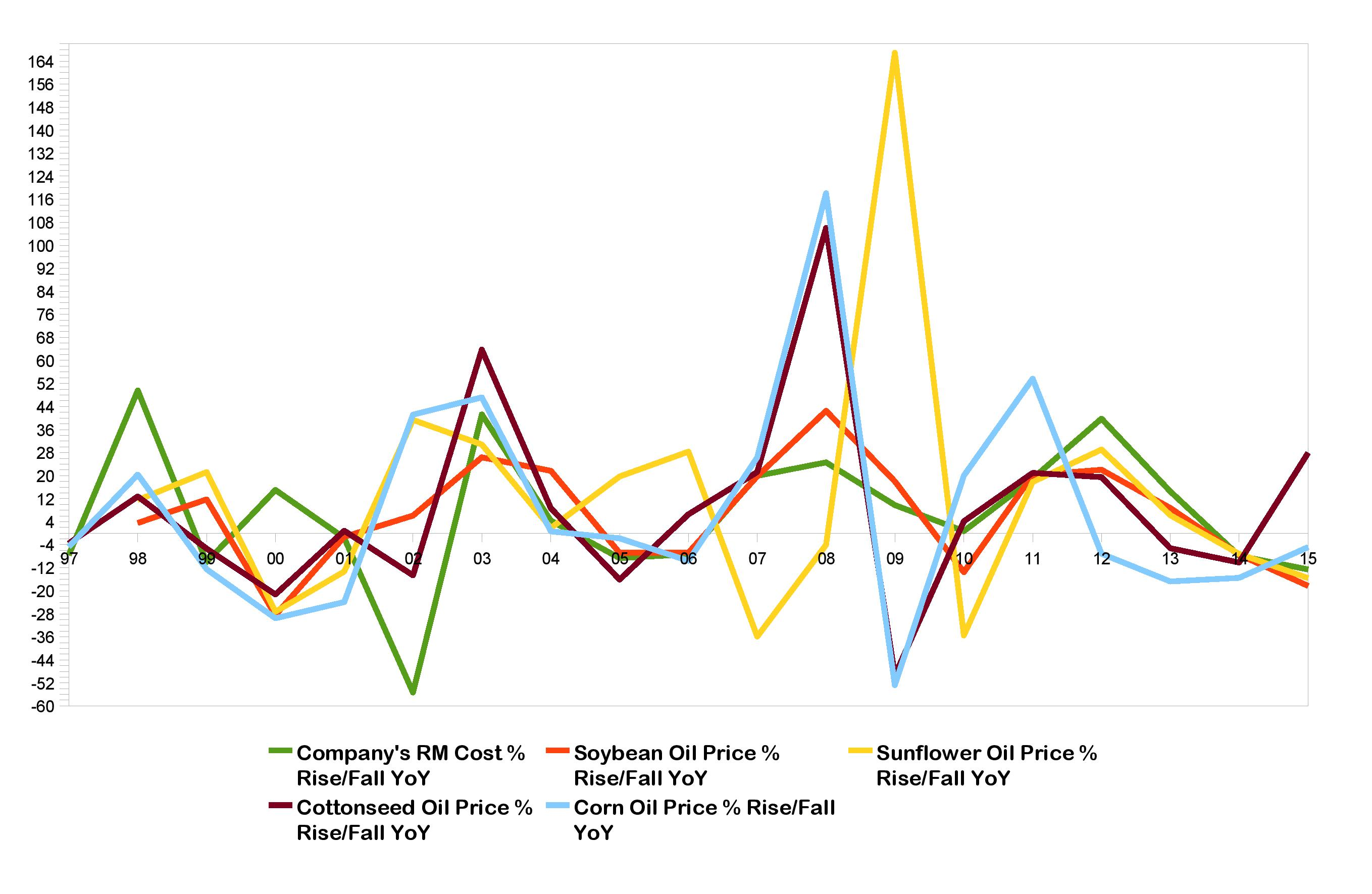

And in these many downs was the business or product offerings good enough to let this happen ?? – If we analyse closely past 20 years’ data points then it seems business/products is not bad but is not good either. This I am saying because, if we check the actual sales realisations registered by the company then they seem to be less than RM price increases that company had to suffer. Just check the realisations’ trend against RM price increase trend from FY07 to FY15 as given before by me and one will find how company was able to turn even a bad period into an extremely good one between FY11 to FY15.

As I said before, its not a bad business atall. All through last 20 years one thing is consistent and that is demand of company’s products. Now is it because management was able to foresee before time that which product will be in demand and so was able to timely introduce such product(s) that is for one to conclude based on varied data points provided.

Technological Advantage :

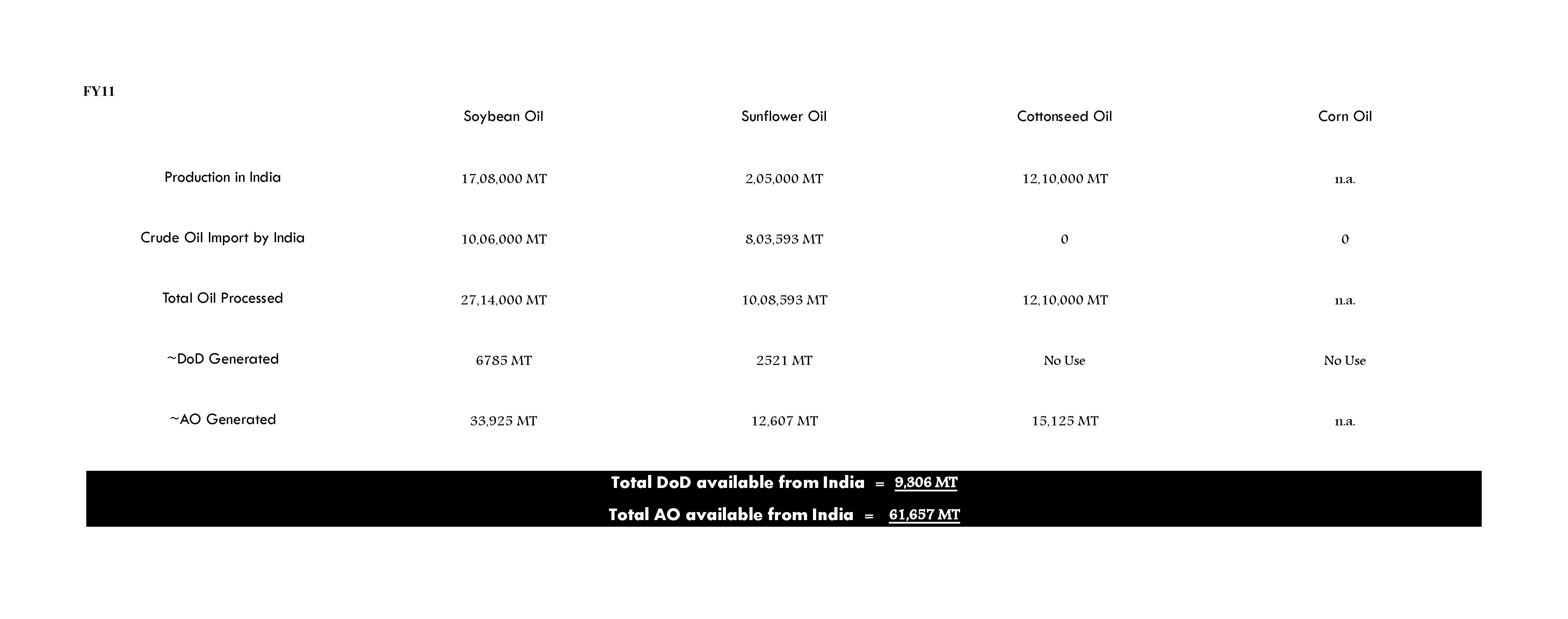

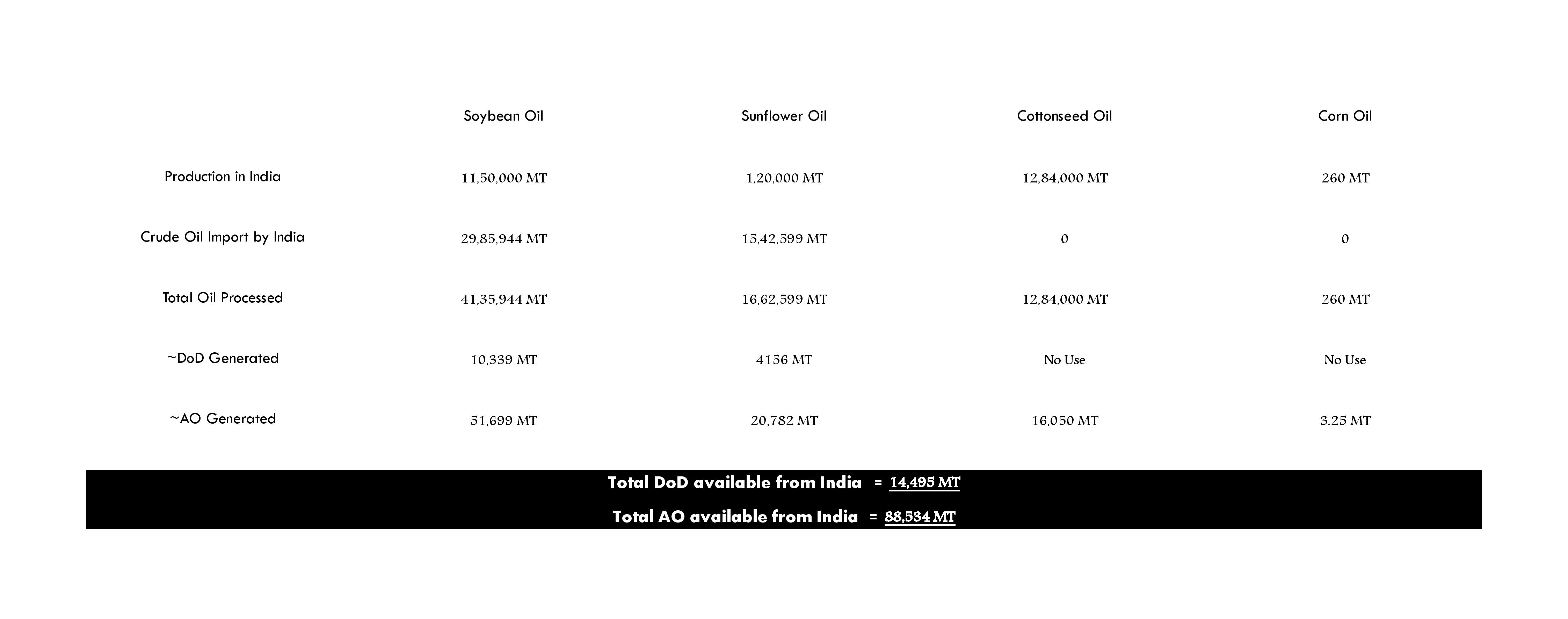

This is the crucial aspect working in favour of the company. Adi Finechem surely seems to have technological edge which, if firm contracts are established with global manufacturers, could do wonders to the company in tocopherol business. Already before in this thread as also many IC reports it is discussed by many how company is able to manage varied quality of raw materials procured from different sources and use them to produce niche products. However, another important thing which no one seems to have looked is the tocopherol yield it is able to generate out of RM used. Just see the trend below :

We have the 15 years’ data out of 19 years from FY97 to FY11 and the average tocopherol yield company is able to generate is 22.48 % – lowest being 18.20 % and highest being 32.51 %. This is exceptional and with current 12,000 MT of RM processing capacity (DoD), one can just calculate the revenue and profitability only tocopherol business can generate in good realisation period if firm contracts with MNCs are established.

Having said all these, the apt heading today for this thread should again be a question – “ Is it a good business facing a bad time ?? ”

Company is surely going through a bad time with :

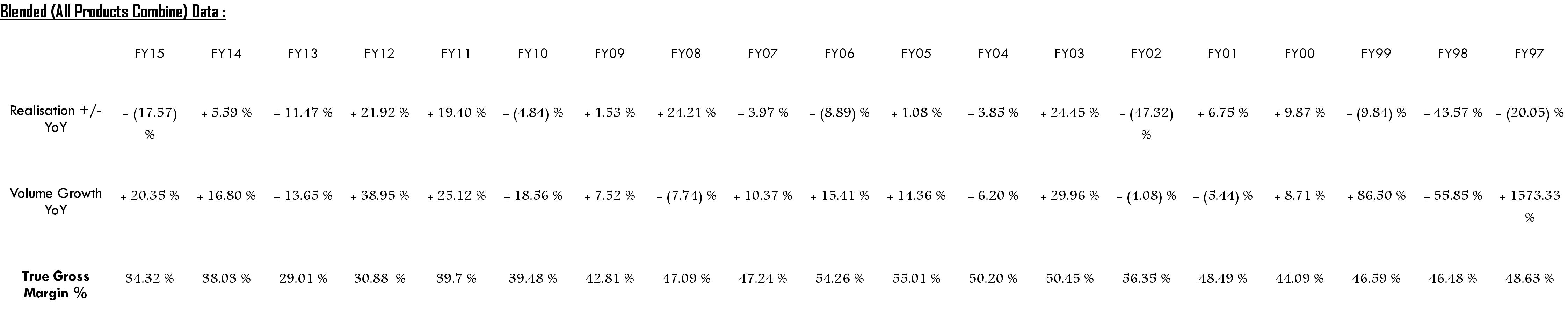

– gross margins touching ~32 % in 9MFY16 over already low figure of ~34 % in FY15 and

– EBITDA margins going below the 19 years’ average and touching 12.41 % in 9MFY16,

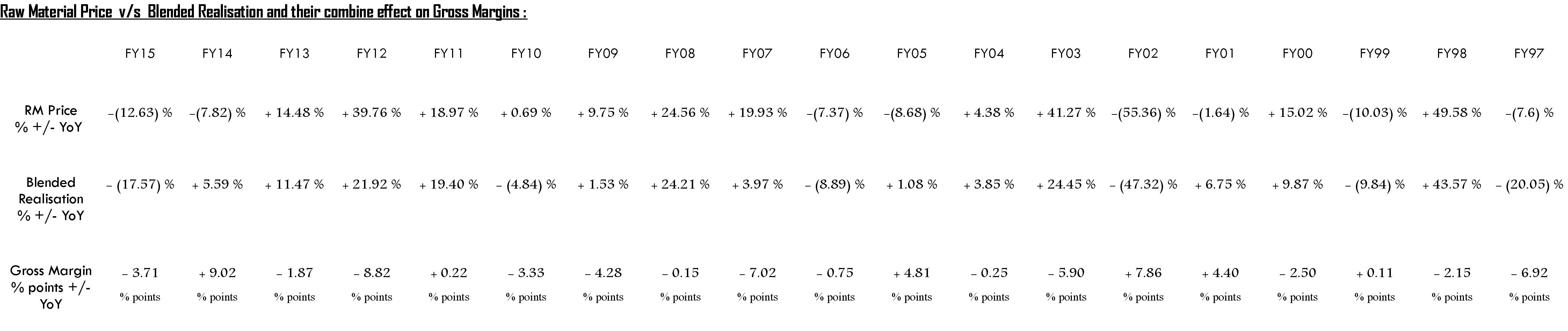

– blended realisation seems to have dropped by 7.95 % as against RM cost drop by 5.75 % in 9MFY16,

– tocopherol realisations have already touched 150k in FY16 which is well 34 % below FY15 realisation and is at 5 years’ low,

Key Question is – is this bad time sustainable ??

If one goes by history then probably not – we need to ask some questions to ourselves :

Will the realisations keep falling and touch 20 years’ lows – blended realisations have already touched 5 year lows in 9MFY16 ??

Will alongwith falling realisations, RM prices continue to keep rising and touch multiyear highs – Soya & Sunflower oils made 20 year highs in FY13 itself ??

Will the demand for company’s products fall severely from now on which have otherwise not fallen over these many years ??

Will company not be able to move up the value chain in oleochemicals itself forget here the nutraceuticals ??

Will company not be able to introduce any new products as it has done in the past ??

To answer only the last question, company was already working on a new product in biofuel segment for which technology and production process were already finalised and samples were ready but the project was shelved as crude went below 50 USD. Now, this is the beauty of this management ; it is not overly dependent on any one segment/product – if tocopherol doesn’t perform, it produces sterols, dimer acid and vice versa and weathers the bad phase and maintains profitability over medium term. Its core area is producing different products from byproducts of vegetable oil processing and it seems to be playing well within this core area.

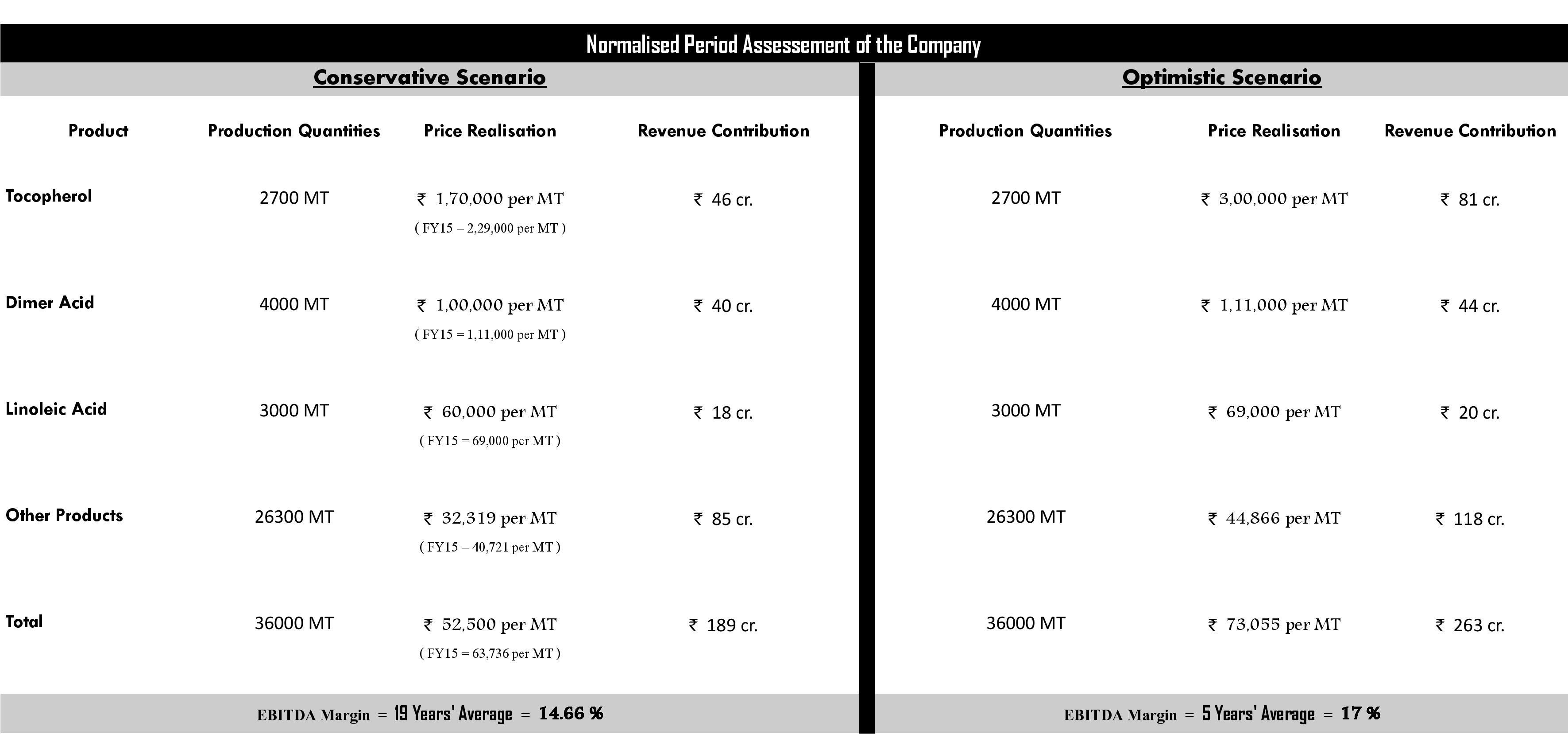

So, when we look at this company we need to look at a normalised scenario (as we should have done in FY14 also when tocopherol realisation touched multiyear highs). Question is what is the normalised scenario for this company. For this, I made a simple calculation based on the variables already known –

Normal Scenario Calculation :

First let’s have a look at a very conservative normalised scenario assuming the lowest realisations of each product –

– Company has expanded to 12,000 DoD capacity and based on tocopherol yield achieved by the company in the past at 19-30 % (average 22.48 %), we can expect 2300-3600 MT tocopherol production at full capacity utilisation. Hence, to assume a normalised scenario, we will take steady-state 2700 MT p.a. tocopherol production within two years from the company.

– Tocopherol 20 years’ average realisation achieved by the company is 169k per MT whereas post ending of exclusive production offtake contract with Henkel, since FY02, 14 years’ average tocopherol realisation comes to 172k. So, on a steady-state basis we will assume 170k per MT realisation and so based on this, within two years on a normalised basis tocopherol alone should contribute 46 cr. p.a. to company’s revenues.

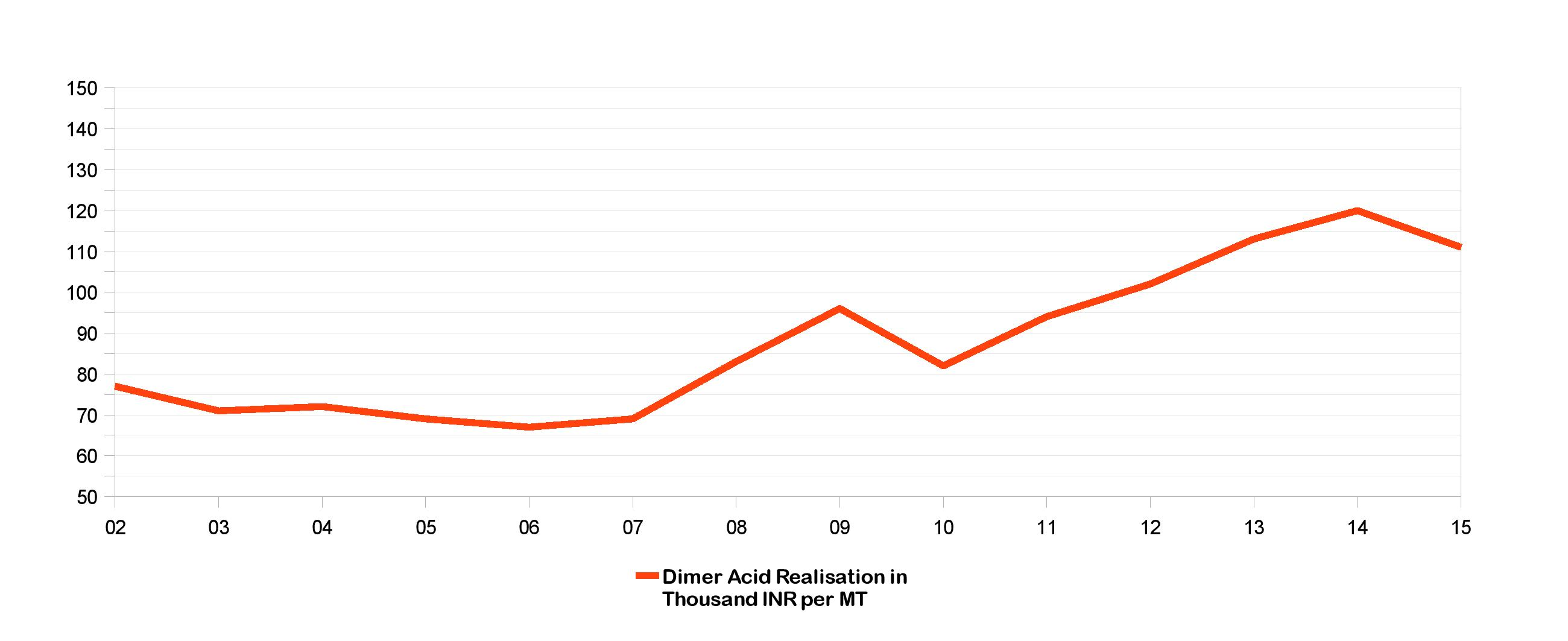

– Company produced 2550 MT of Dimer Acid in FY15, with expanded capacity, company should be able to produce 3800-4500 MT p.a. of Dimer Acid. So, on a steady-state basis we assume 4000 MT p.a. of dimer acid production from the company within two years.

– Dimer Acid 14 years’ average price realisation achieved by the company is 88k per MT. However, FY15’s realisation is 111k per MT and from the data points given before we know that dimer acid’s realisation are pretty stable and have never fallen more than 14.58 % YoY. Also, in FY10 when dimer realisation fell by highest 14.58 % YoY to touch 82k, it didn’t go below then five years’ average of 77k. So, we will assume normalised dimer realisation of 100k per MT which is below FY15’s 111k as also five year’s average of 108k. Hence, steady-state contribution from dimer acid based on this realisation within two years on a normalised basis should be 40 cr. p.a. to company’s revenues.

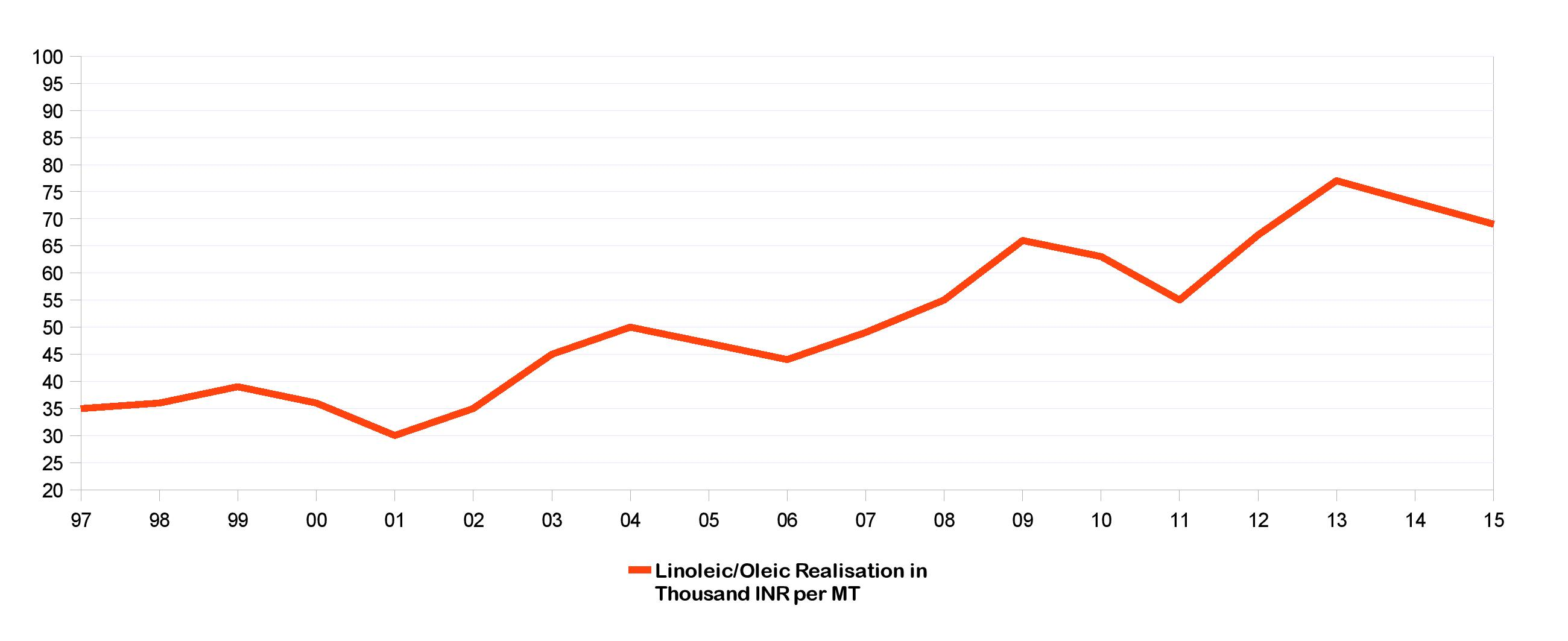

– Company produced 1858 MT Linoleic Acid in FY15 and with expanded capacity it will be able to produce 2800-3400 MT p.a. of Linoleic Acid. So, on a steady-state basis we assume 3000 MT p.a. of Linoleic production within two years from the company.

– Linoleic Acid 19 years’ average price realisation achieved by the company is 51k per MT. However, FY15’s realisation is 69k per MT and from the data points given before we know that Linoleic acid’s realisation are also pretty stable so, we will assume normalised Linoleic realisation of 60k per MT which is below FY15’s 69k as also five year’s average of 65k. Hence, steady-state contribution from Linoleic acid based on this realisation within two years on a normalised basis should be 18 cr. p.a. to company’s revenues.

These above-mentioned three products have contributed average ~ 55 % in value terms to the company’s sales and so keeping the same ratio, normalised steady-state topline should be INR 189 cr. p.a. with average 14.6 % EBITDA margin (again a 19 years’ average) or an EBITDA of 27.5 cr.

Now, an optimistic normalised scenario based on the good period we witnessed before –

We will assume the same production quantities of three products as we have assumed in conservative normalised scenario but only realisations will change – we will assume tocopherol realisation at 5 years’ average of 300k per MT, we will assume dimer acid realisation at same 111k of FY15 and Linoleic realisation at 69k of FY15.

With these realisations, we get a topline from these three products at 145 cr. and applying the same ratio 55:45 as before we get a blended topline at 263 cr. with an 17 % EBITDA margin (5 years’ average) or 44.7 cr. EBITDA.

These production quantities assume ~80 % capacity utilisation of expanded capacity which is below 19 years’ average capacity utilisation of 85.78 % at which company has worked.

Fairfax Coming in diminishes most of the Internal Risk Factors :

Before discussing this aspect, I need to admit one thing that Adi Finechem came on my radar two times before and each time I turned it down after some initial analysis as I had doubts on three aspects – Scalability, Funding & Continuous Efficient & Ethical Running of the company. So, is Fairfax entry so important that all these three concerns are addressed ?? I feel yes because even before, there was no doubt that management had nice operation and good business to run with history surely on its side, but having niche business/products is a different thing and to scale it beyond a particular point is a different thing. Now, with Fairfax coming in as a majority shareholder, management can’t be complacent and can’t afford a failure as otherwise management itself runs a risk of ousting. There will be quarterly reviews of the management and at each stage, success/failure of a particular vision will be assessed. Resources/contacts will be aplenty and funding will also not be a problem. Inefficiency and loose corporate governance also will not be tolerated as above all Fairfax’s goal will be to earn superior IRR from its investment.

Attached is Fairfax India’s first Annual Report for members’ reference. It is worthwhile to note here that Adi Finechem’s MD Mr. Nahoosh Jariwala will be representing his company on April 14, 2016 at Toronto alongside Mr. Nirmal Jain of IIFL and Mr. Sanjay Kaul of NCML in front of audience which will include, amongst others, repesentatives of renowned institutions like Fidelity, Franklin, Blackrock, TD Asset Management, Vanguard, etc.

We also need to note here one another interesting thing that Adi Finechem today is a sort of unique company where majority of the shareholding is having its cost price near to CMP. Fairfax’s 45 % shareholding price is INR 212 per share, Malabar’s 4.26 % average holding price is INR 255 per share and SBI’s 3.41 %'s average holding price is INR 210 per share ; so effectively, 52 % of the shareholding’s average cost price is just 20 % below CMP. Although this doesn’t mean anything, but, it could help in commanding of scarcity premium in good times as these holders might not part with their holdings at a lower rate unless there is some significant negative development with regards to the company.

To sum-up, Adi Fine Chem Ltd. at current stage seems to be :

A good business…going through a bad time…run by a good and dynamic management…supported by a strong strategic investor…who, alongwith management, are having aggressive future organic as well as inorganic plans.

Key Monitorables :

Product Contribution Trends,

Product Realisation Trends,

RM Price Trends,

Capacity Utilisation Trends,

Greenfield Expansion plans,

New Product Introductions,

Acquisition Profile & Structure of the deal,

Funding Route – proportion of Equity dilution, debt, low-cost debt support from Fairfax.

Discl. - Invested in Adi Finechem Ltd… Company forms 15 % + of family portfolio. Bought in last 30 days.

Note – This is not a Buy/Sell/Hold recommendation of any kind and is only part of a general discussion. Here, only statistical facts and figures are presented and this should in no way be interpreted as recommendation of any sort. Statistical Facts and Figures are meant to be used as further study of a segment/niche business and not otherwise.