Sir you have covered the company’s future growth well. But what do you think could be the issues which could be detrimental for Expleo?

Disclosure: Holding

Sir you have covered the company’s future growth well. But what do you think could be the issues which could be detrimental for Expleo?

Disclosure: Holding

Any subdued growth or clients freezing or postponing projects, Recession in the IT sector, will affect Expleo.

But do bear in mind, that even during the worst period of Brexit & Consequent Forex losses ,& clients freezing, & postponing projects, SQS BFSI , reported annual consolidated EPS of ₹21. That shows the resilience of Expleo.

However , over the coming 10 years ,IT sector is expected to do extremely well , with digitalization, Cloud, IOT ,RPA, Block chain , Security surveillance, Data analytics, 5 G etc , & Expleo is expected to outperform .

Yes, there is competition as well, but as per Neelson report & the Management, there is enough space for all, in a growing market.

Further Expleo plays out in the higher end of premium segment, , leaving the lower margin segment to other players.

Another issue is that forays into US Markets , have not been successful & Expleo is left with a negligible share of US Market.

The strategy of Expleo management is to focus on European, APAC , Middle East & india to Ramp growth & profitability.

Of course, the Management, continues with sustained efforts to conquer the US market & I’m certain, that there will be a break through in US market in 2023, to be precise, & thereafter Ramp growth in US Markets too.

Further cross selling of products & services using the clout of the parent ,is a certainty in global markets, including USA.

Since the market is competitive, these players could enter into better margin businesses that Expleo is in . Do you see any competitive advantage that Expleo has that the Other players dont? If Expleo directly competing in Europe with TCS, Infosys or Wipro with deep pockets, then there is a threat to the sustainability of those margins.

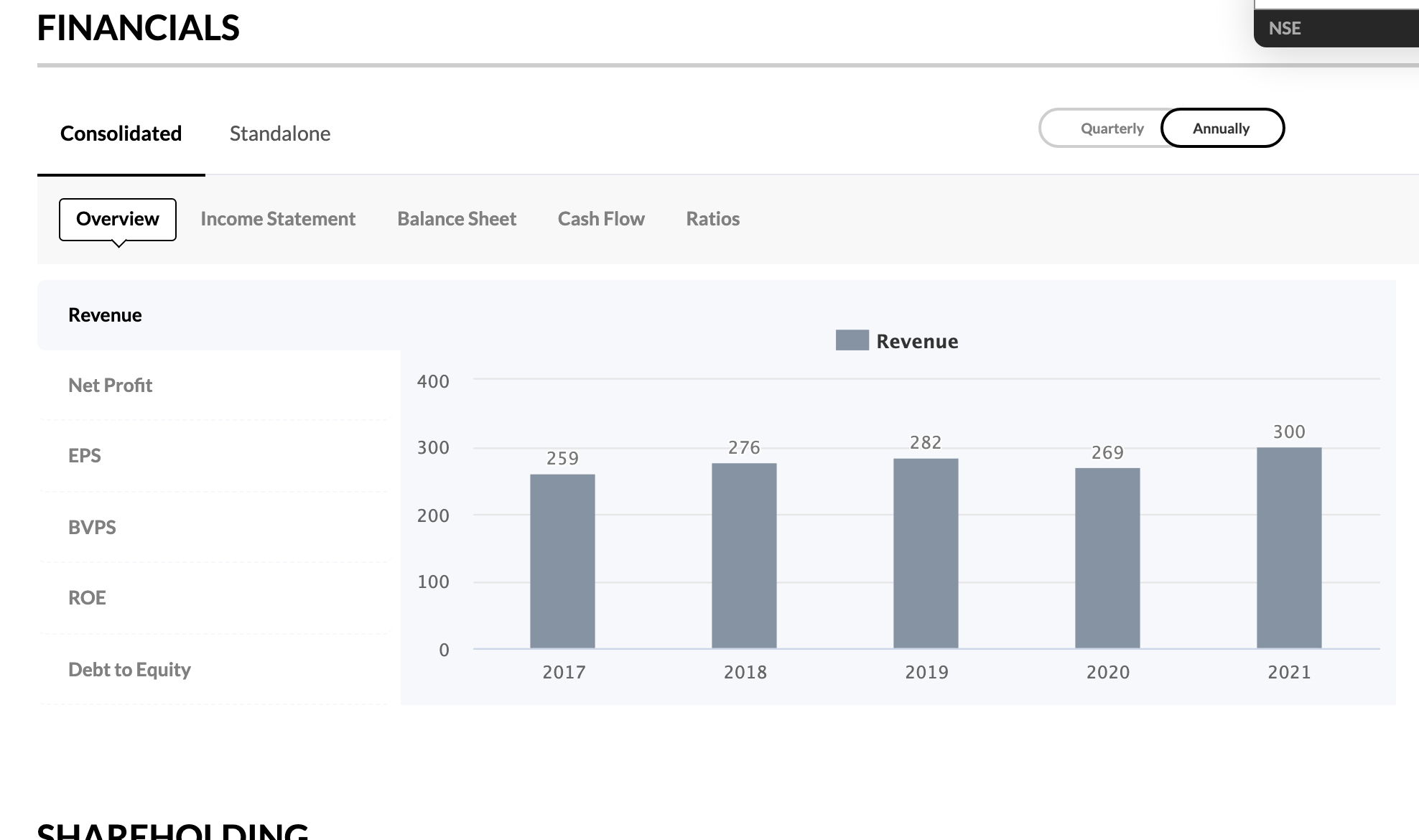

I would want to be in Expleo for a long term if there is a clear visibility of it going from a micro cap to a midcap by ramping its Sales and Profits. Currently the valuation with respect to earnings and book value is stretched. The last five years the sales has only grown at 3%. It has been unable to grow at higher rate.

Disclosure: Holding

Just because the past growth rate has been poor doesn’t imply that future growth will also be poor.

Most important, in the past, Expleo has always maintained consolidated EPS above ₹25:, except during the worst period of Brexit , when it was lowest at ₹21.

Now Expleo caters to certain niche segments, where there is no direct competition with TCS, infy & Wipro.

Even infy ,TCS & Wipro ,use Expleo for QA & validation of their products.

You have seen glitches in GST implemented by Infosys & Income tax portal glitches for which infy was summoned to Finance ministry, but you will never find glitches in Expleo.

To illustrate ,it’s like infy & TCS designing & execution of Multiplexes , while specialized systems like audio, central Air-conditioning , interior furnishing, ambience, event management , plumbing & electrification are outsourced to specialists ( Read Expleo) where the margins are higher , for specialist j

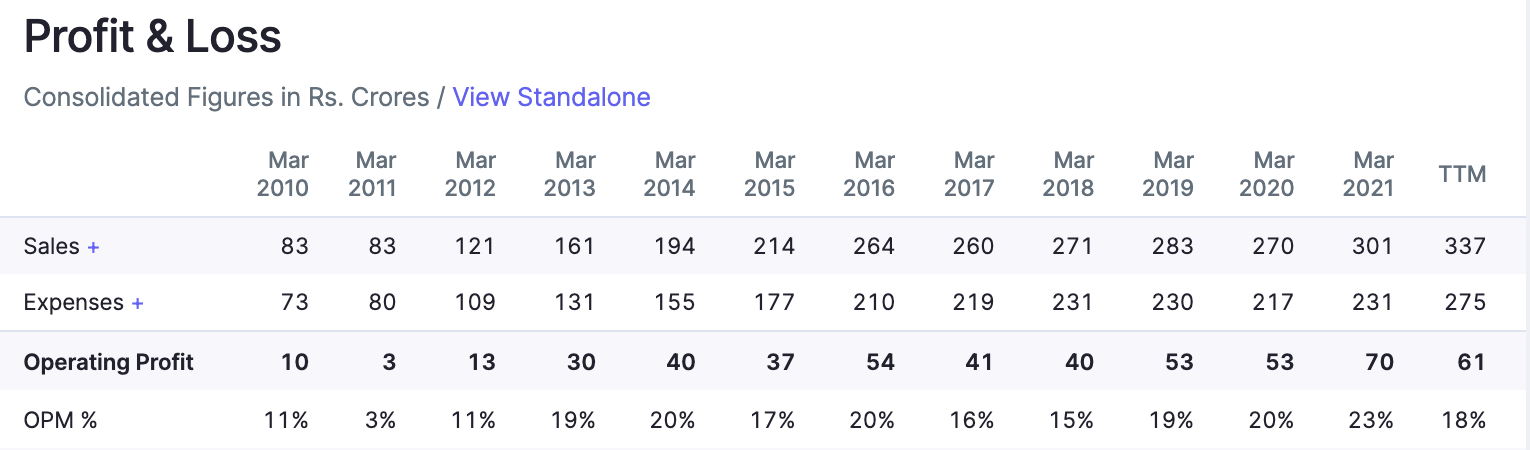

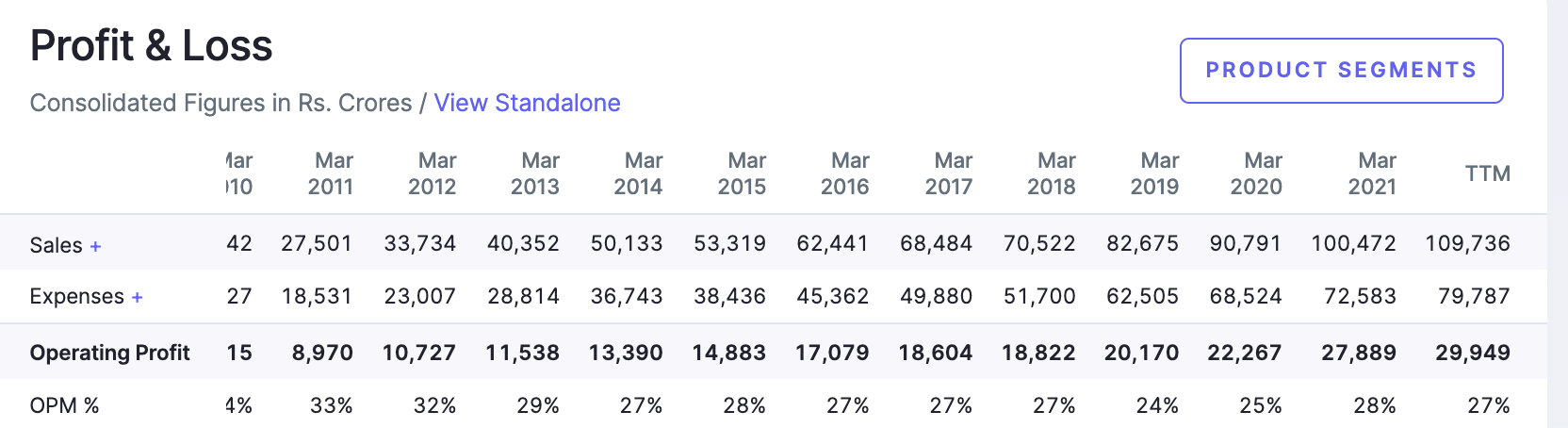

The operating margins of Expleo are lower when compared to the operating margins of TCS.

Expleo 19 - 23 %

TCS 27 - 29%

Infosys 25 - 29%

It looks like TCS, Infosys has a better operating margin when compared to Expleo. If there is a better margin business that Expleo is in, it is not reflecting in the books. Then where is the better margin business evident? Am I missing something that you are trying to elucidate?

You are definitely right on the points raised, Historically Expleo margins have not gone beyond 27 percent & averages around 24 percent.

Expleo is primarily into software testing & Quality assurance business, the contours of which are rapidly changing. The future lies in digitalization.

So in the past , the margins have been around 24 percent, however in future, Digitization, Robotic process automation, IOT application on 5 G , Data analytics, Security surveillance, cloud based services, Block chain application & Consultancy @ Moore house consulting, are the specialist jobs , where margins would be substantially higher.

New Revenue streams being mined on digital platform are not limited to BFSI segment, alone , but also in aerospace, automotive, telecom, Retail , pharma & across all industries wherein software is employed.

Expleo is not into software production ( except for an in-house unit) , while Infy , TCS , Wipro are into software production as also other services related to software , like QA , validation, which are done by different teams or outsourced to Expleo .

My few cents on Expleo.

I am doctor by profession so ( kind of ) can have unbiased view.

I entered and started averaging up in Expleo when I came across “Merger” reports by MNCL & Sharekhan from 1100.

This is basically a SPECIAL situation investing scenario.

If one sees sales of Expleo ,they are surely flat without any significant growth.

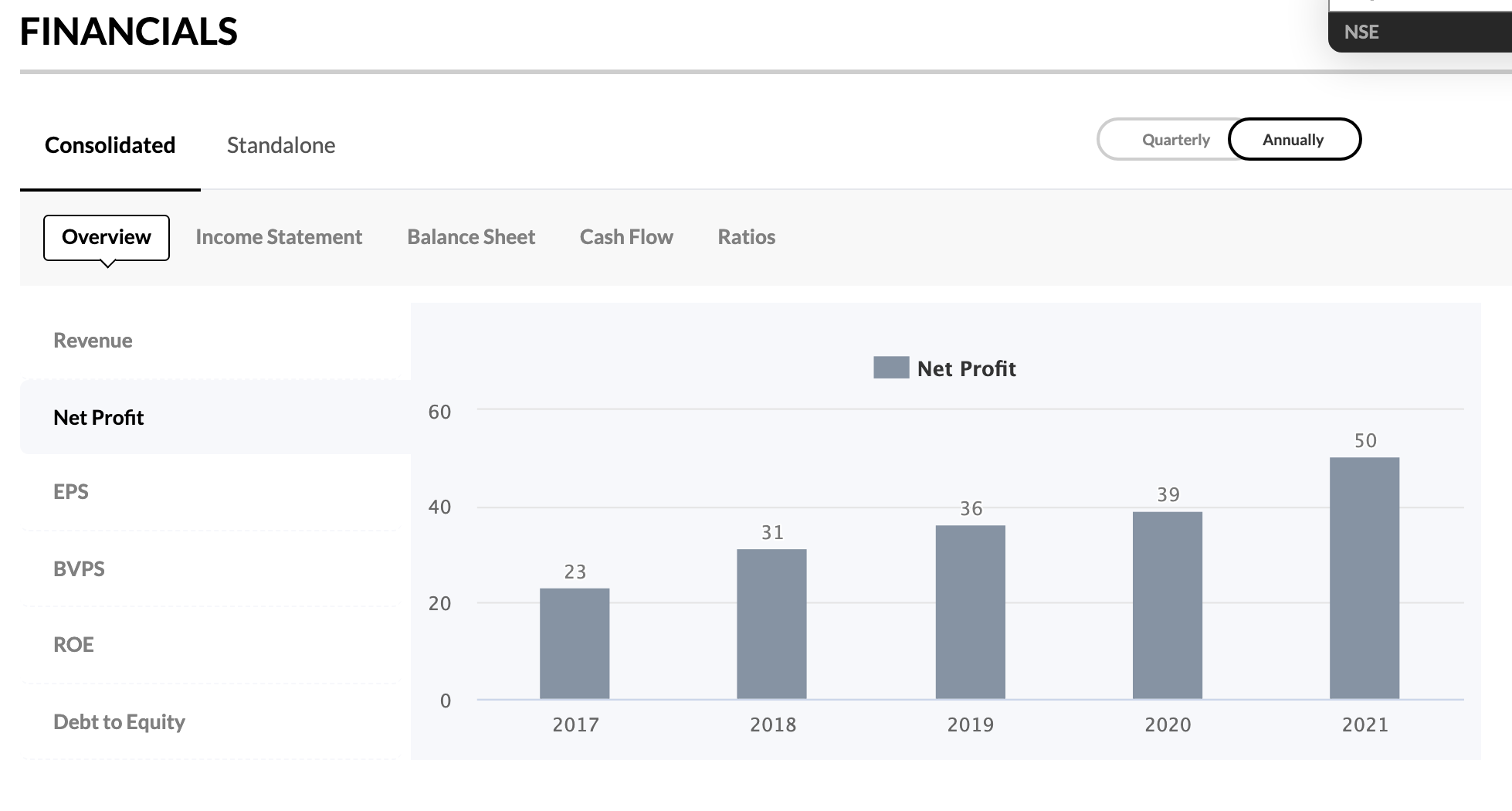

But management has done a good job to increase net profit YoY.

Probably the Management also know that the next growth in sales may not be easy and that why they are going ahead with this merger.

My plan as of now is to ride this till the actual merger happens and then wait for few quarters to see any REAL growth in the sales and then decide about holding / selling the business.

Regards,

Dr. Vikas

Hi @Balki ,

Being a novice investor, I was interested in this scrip and had taken tracking position @539 around 8 months back.

But after seeing your tremendous analysis, I am very much interested in this stock. Having been working as a QA myself in the fintech domain, I can say that we were mostly into automating all the transactions of banks which would use our products.

Based on your analysis, I see you are using a lot of technical terms such as IOT, 5G, blockchain. I am really not sure how automation would go forward in this space and would like to know more about it?

Could you give more details?

Automation is a process in which entire gamut of services are programmed to start & stop at a predetermined time or completion of the task.

Simply put, street lights can be programmed to switch on & off, industrial production programmed to start & stop , food processing, irrigation, agricultural harvesting , etc can be programmed without the need for human intervention across all industries.

Now it’s like the Lord of the universe switching on ,day & night, Rains & thunder, birth & death , pandemics etc with precision .

Now ,Robots with or without human like bodies, with artificial intelligence are used inside Nuclear reactors

to ignite fission & reprocess radioactive materials which humans can’t do coz of lethal radioactivity.

These same Robots with alloy type human bodies, with artificial intelligence can substitute humans in cooking food in Restaurants, Driving vehicles, cleaning & mopping, manual & industrial labour & industrial process etc,which is called Robotic process automation.

IOT is linked to 5 G & will open up opportunities which cannot be imagined.A surgeon in US or Europe can conduct surgery on a patient in Bangalore , using IOT based Robotic process automation.

You art working in Fintech space but thou dost remember that the whole of human universe in running on software like industrial production, Retail, aerospace, automotive, telecom .

These software systems need validation, Quality assurance, to prevent glitches or accidents, continuous improvement, updation, prolonging lifecycle of the software etc .

This is done by Expleo ,as a specialist, while we have Infosys, TCS & Wipro creating & patenting software for diverse needs & applications.

So long but I have cut it short. Hope it helps

It sound so complicated. For people like me who are in not in the IT industry all these difference between what Expleo and what Infosys or TCS does is so vague. Especially when we say Expleo is a specialist and TCS and Wipro patent new software. That does not sound any different. Basically if they are patenting software it has to be unique. They wouldn’t be patenting something which can be done by all. So in that sense they are doing special work too.

Expleo is no longer in testing alone. It is part of a larger entity now covering other fields in IT services. Most of these overlap with what other bigger companies are doing.

I feel that Expleo has lesser margins than TCS and Infosys is not concerning. But TCS and Infosys might be charging premium for their services where as Expleo is unable to do so.

Almost every IT company is talking about Automation now. There is opportunity for more and more players. So that is good for Expleo. Its just that I feel Expleo is not the only specialist or expert. It is probably similar to Speciality Chemicals and Pharma where those industries have been accommodating many players providing them with sufficient margins. In other words, the IT industry has a very long runway and there is demand for what it’s creating and that is the reason for good margins.

I can understand from what @Balki sir is trying to explain is that most of the emerging technology like Robotic process automation, Self Driving Vehicles, Industrial automation is going to come or has already being used.

To elucidate further, take for example self driving technology which @Balki presumes is the domain of Expleo like companies and not of Infosys or TCS.

It is better to be cautiously optimist and think twice before investing in microcap like Expleo.

Disclosure: Holding

It’s not complicated unless you want it to be. Simply put ,infy ,TCS , Wipro manufacture software for diverse requirements.

Expleo does value added services on the software produced by others like validation & Quality assurance ( to avoid glitches & teething troubles), increasing the life span of the software by periodic updates ( otherwise obsolete) , security surveillance (otherwise hacking ) & tailoring this software to meet their various requirements ( user friendly & made for each other)

Now the classic example is the glitches in GST software manufacturered by Infosys over a span of 2 years . During this time , there was massive evasion of GST by those who took advantage of the glitches in the system. Govt of India , lost several lakh crores due to glitches in GST software.

Looks like Govt acted penny wise & pound foolish.

Now had the GOI entrusted the validation & QA of GST software to Expleo , this software would have run seamlessly & would not crack under any circumstances. Of course GOI would have to pay a few crores to Expleo, but then GOI would have got a few lakh crores more in revenue, which was evaded by several clients using glitches in GST software.

Now GOI has liberty to act penny wise & pound foolish, coz of bureaucrats who are nuts .But MNCs & corporates worldwide will not allow a bad name/ loss of revenue/ client dissatisfaction due to glitches in the software. So they use Expleo to test & QA the software manufacturered by infy to ensure that it works seamlessly.

So as long as software is manufactured in the world, Corporates & organizations use Expleo to validate QA & 24X7 security surveillance of their software.

In the rare event of any glitches happening at any time in future, it’s the endeavour of Expleo to repair & restore the system ,in the minimum possible time, though in real world it never happens.

Now I come to the main point. Commercial 5G with embedded IOT ( internet of things ) will be available in india from January 2023 , while beta testing will begin in second half of 2022.

With 5G & IOT , there will be unlimited opportunities,& Expleo will be the main beneficiary. When you talk about Robotic process automation ( RPA ) or automation, what will happen if there arise glitches in automation software? The end product ( chemical/ pharmaceutical/ ) will be useless & has to be thrown out , creating hefty losses. So whether it’s RPA or automation software validation & QA can’t be ignored.

Caution is always advised in stock markets.The converse is no pains ( risk ) no gains. Expleo is a high Risk high return stock . The MNC lineage, high promoter stake ( 71.05% post amalgamation) good corporate governance & tailwinds in IT sector, mitigates the risk to a substantial extent.

I will not be surprised to see levels of ₹5000 plus in January 2023 , for Expleo coinciding with Rollout of 5G in india with IOT which is the kingpin for the blast in Expleo .

Expleo again

Returns in Expleo ,as in most stocks are non linear.

Expleo has given 4100 percent return in last 10 years ,535 percent in last 2 years & 260 percent in last 1 year.

Above returns, when compared to Fixed deposits interest of 6 percent per annum & embedded TDS ,looks astronomical.

Typically all stocks , follow a cycle of rapid growth & few years of stagnant growth.

Now I would like to highlight that the next 10 years , look promising for IT companies to give megasized returns of 3400 percent plus. It would be prudent to invest in a basket of IT stocks for mega returns.

View Point

Date: 22.12.2021

Source: Sharekhan

Disc: Invested

[

ExpleoSolutions QuickBites.pdf (768.9 KB)

](https://)

Q on Q , increase in topline & bottom line,in a seasonally weak quarter is commendable.

There has been increasing Expenses on manpower as

Well as Coimbatore facility being operational.

I will give a detailed view after attending concall, tomorrow at 12.30 noon .

Amalgamation of unlisted entities with Expleo will be completed before March 31, 2022, awaiting legal approvals for the amalgamation.

Thank you, Nitin Jain, for uploading the results.I feel the scrip can easily take out ₹2500 levels by end of 2022 or early 2023, with increasing digital deals.

Roll out of Digital currency in india in 2023 as well as in Europe & USA , along with 5G embedded IOT will open up immense opportunities for Expleo.

Why do you call this a traditionally weak quarter? A quick search on screener shows that the revenue and PAT for Oct - Dec quarter has been comparable, if not better, than the previous quarters for the past couple of years.

In IT sector typically ,Q1 & Q2 show Robust Results

Q3 is seasonally weak, due to large no of seasonal holidays, Xmas vacation,& clients demanding year end discounts due to budgetary constraints or ramping down with spillover to next quarter.

Q3 is seasonally weak for Europe & USA business

Q4 is another week quarter for Asia due to seasonal holidays, vacation & budgetary constraints due to financial year end.

I spoke in General, but there are exceptions too.

The result of expleo solutions is in line with expectation if you have observed this quarter company had exchange loss of 1.6 cr compare to exchange gain in yoy quarter of 3.7 cr so eventually if we exclude such kind of gain/loss then NPBT comes to 17 cr compare to 13 cr YOY. That’s 30 percent increase

Further the expenses of staff count has increase as company has hired 416 employees this quarter seeing the growth perspective in future.

Good thing is new 14 new client were added during the quarter that will add the new revenue potential.

Dis- invested