Hi , Vineetjain fully agree with you. I have nothing more to say.

2 Likes

yes , we are unncessary argueing. ,Market knows better then us and they have postively rewarded, and i must thank @Balki . Your conviction about the company has helped me as i am holding expleo since more then 5 years and due to your views still holding .

1 Like

Read and draw your own conclusions on the financial performance of Expleo group.

Expleo financials: YE 2020.

Expleo Group – in which Assystem holds 38.2% of the capital as well as quasi-equity instruments issued by that company (convertible bonds with capitalised interest) – contributed a negative €35.2 million to consolidated profit, breaking down as Assystem’s €45.2 million share of Expleo Group’s loss for the period and €10.0 million in coupons on the convertible bonds.

Revenue generated by Expleo Group came to €908.0 million in 2020, compared with €1,084.1 million in 2019. The Covid-19 pandemic severely hit demand for outsourced research and development in Expleo Group’s two main sectors of activity, i.e. the aeronautical and automotive industries. As this impact is set to be lasting, the company has decided to restructure its corresponding operations, primarily in France, with most of the restructuring measures to be carried out in 2021.

Expleo Group’s EBITDA (excluding the IFRS 16 impact) amounted to €51.5 million for 2020 (of which €27.3 million in the second half), representing 5.7% of its consolidated revenue, versus €108.6 million and 10.0% respectively in 2019. The 2020 EBITDA figure includes a negative €12.8 million impact corresponding to the residual amount borne by the company for its employees on short-time working and furlough schemes, recorded in EBITA (which totalled €38.6 million).

Expleo Group recorded a consolidated loss of €92.2 million before recognition of the capitalised interest on its quasi-equity instruments. This amount includes a net non-recurring expense of €77.3 million, of which €66.8 million relates to the provisions for the restructuring plan.

Also equity of EIIPL the co which will merge with Expleo Systems Ltd(the listed co) is Rs11.47 lacs.

2 Likes

Regarding your views on consolidated loss, it’s not the loss ,that the market prices in, but the potential for future growth & profitability & the track record of the promoters.

Going by the same logic ,Tesla , Flipkart, Amazon ( indian operations) are incurring heavy losses , but the market prices them at a premium.

Dear HIMSHAH

My conviction, comes from indepth study of Expleo solutions since 2016 .

The Indian listed entity, post amalgamation, will provide tremendous opportunities for capital appreciation, along with buybacks & dividends.

Iam one of the top 10 shareholders of Expleo.& I can say, that Nihar Nilekani son of Infosys director,Nandan Nilekani, Rajasthan global securities, Little Champs PMS of Saurabh Mukherjea & of Expleo director Rajiv kucchal ( venture capitalists & former Infosys group director)hold substantial quantities in Expleo solutions.

You can see the pdf of Top 100 shareholders I have posted previously for reference. The Market has also given thumbs up , to the amalgamation & it’s a win win situation for all including minority shareholders.

2 Likes

#Balki-Loss is a loss. Mkts can price in anything. I didnt say that the mkts cannot price in anything. Bitcoin has no assets, balance sheet or a regulator but the mkt prices it at crazy value.

I only said make your own conclusions.

1 Like

@esoteric thanks for sharing. Are these figures for the global entity?

What does this mean? The document that they released on Friday said the net worth of EIIPL was 225cr.

You may be partly right about the Market’s behaviour. Markets are mostly right in the long term. This spike definitely makes most of us Euphoric. But It is acting like a voting machine now. Today I noticed that the major bidding was done by one person in BSE and other in the NSE for around 20K and 5K.

The fundamentals of Expleo Solutions as a testing company has been great too. After amalgamation, the company is going to be operating on other areas. Let us wait and see how it is going to perform going forward.

I am holding on to the stock but with a weak conviction. The stock might go up for now and let’s hope that the Earning does not get diluted in the future.

1 Like

Paid up equity of EEIPL- Rs87.35 lacs

Equity of ETIPL—Rs14.04 crs

Paid up equity of Silver software devp centre-Rs2.5 crs

These figs are for global entity. They may be having huge reserves

So this is for the Year 2020 only. The following are the questions that we can ponder on

- What about the performance of the group in the previous years? Were they performing well before or were they loosing like they are now?

- Software companies usually carry intangible assets along with fixed assets. So how were they valued?

- Is there a solid management in place other than the Private equity player ( who are usually there for a short term )? Is the present management committed like the previous management who build SQS India?

- What will happen if Minority shareholders who own 48% don’t want their earnings get diluted voted against this proposal? ( This is just an a hypothetical question ) At least they would get to change the exchange ratio from 468 shares to a figure which is the average of the last three years. ( I might be wrong here because the valuation report is not yet in the public domain )

i think anyone with any doubt about merger should grab this opportunity to ask the managment

1 Like

The most important question to ask by any one will be

- will the company ask SEBI to investigate insider trading in the shares of the co?

No one can deny insider trading( up 85% in last 75 days).If co denies insider trading, it is not admitting what is obvious and if it refuses to lodge a request it means they dont respect shareholders/ investors.Anyone who participates in concall and gets a chance to ask the management should put this right on top.

2 Likes

Last years figs are given to compare.In the AGM one shareholder of Assystem asked when will the co get back to profitability of 2019 levels and the co says it wont be before 2022-23.

Another shareholder has asked when will Assystem exit expleo and the board has said it will exit together with Ardian as and when Ardian decides.

The first qtr '22 results shows good recovery but the co has attributed it to the nuclear power division which has been bagging large contracts.

The qtrly results is not showing the expleo part separately.

The half yearly results are due on 15sep.

Sorry.It should read 75 days.

1 Like

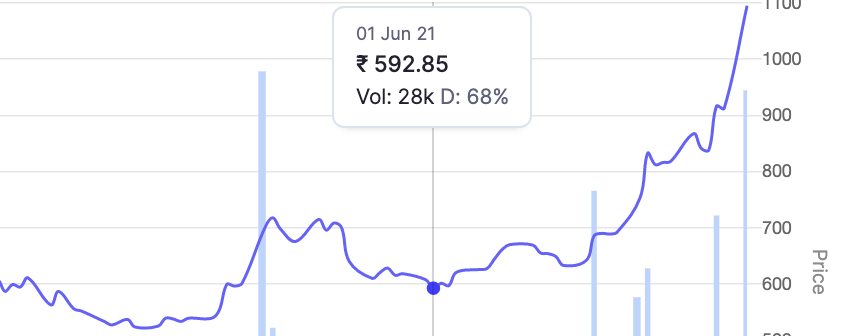

True.1June is Rs592 and on 3 May is Rs539.

The co will know better when they decided to do the merger and how the prices moved up since then.

1 Like

How are the subsidiaries unprofitable? Please go through the investor presentation. The subsidiaries are perfectly profitable with a PAT margin of 19%.

available at MCA with a small payment.

1 Like

Summary of concall -E&OE

KTAs of Merger call.

• ETL - Bangalore – Revenue - 97-100 – totally from engineering services – PAT – 12 cr

• EIS - Pune – Revenue - 150-155 – around 15 % from engineering services – PAT - 25 cr

• Unlisted entity revenue around 230 cr in FY20 , NW of unlisted entities is around 257 cr .

• Combined entity cash - 277 cr – March 2021, Combined EPS would be Rs. 60 on FY21 as against 49 in FY21 standalone. Total shares (combined entity) would be 15mn shares, equity 15 crores.

• Headcount - 2600 3200+ ppl, building a 5000 ppl org by 2023. Headcount growth to revenue not linear. 90% growth in Headcount can translate into roughly 65% revenue.

• Current group revenue is around 33%, direct business – 66%. In future – group 42%, direct 58%

• E R&D services will include – software + mechanical – automotive+ aerospace – setting up plant, to software. Will compete with Tata Elxsi (direct market perspective)

• Cost synergies – shared services right away, no cost cutting, will not add capacity as merger allows growth with current capacity.

• Group level - $1bn - YoY 12% growth. Best shore leverage is small – scaling up India operation. India growth will go up as sourcing from India will improve. Targeting larger deals.

• Cash distribution policy would be updated in next call. No acquisition being evaluated would be finalised in next couple of quarters.

• Related party loan of 20cr outstanding. why? UK subsidiary to french group entity. Given to them for better interest rates. Cash pool arrangement, repayable/available on call.

• 3000 out of 14000 employees in India. Last 3 yrs not expanded. Best shore capabilities of India is largest so far, hence merger. Bulk of volumes will go to India. Overall off shoring today is in single digit, objective is to take that to 25-30% in next 3 -5 yrs.(?)

• No goodwill in books, just additional issue of shares. Shares are being issued at par.

12 Likes

How can there not be goodwill when the value of shares issued is higher than the value of assets transferred? Neither the questioner understood nor the respondent.The value of shares is the price of the shares on a closing basis on the date the board approved the merger.

“Any excess of the amount of the consideration over the value of the

net assets of the transferor company acquired by the transferee company

should be recognised in the transferee company’s financial statements as

goodwill arising on amalgamation. If the amount of the consideration is

lower than the value of the net assets acquired, the difference should be

treated as Capital Reserve.”

1 Like