Absolutely correct.Why merge,pay valuation fees,list and then delist.The purpose is apparently to consolidate the software units in India and grow from here.

1 Like

MNCs also dont stop paying dividend for no reason and say they are yet to formulate a dividend policy.

What is wrong in disclosing the past 5 years turnover and profitability and come clean.

EPS has no ramification when you compare the net worths of the merging entities.Need to see the components of networth of unlisted cos.

The group has in the last two years acted unprofessionally how much so ever they may try to disprove it.

1 Like

SEBI should investigate the buyers of the last 5 weeks.The leak could have occured from somewhere given the large volume increase and price ramp up.The exchanges had sent a notice to the company on the sharp price movement and the company had informed that there was nothing of consequence to relate this movement with the cos workings.

Now that the merger is announced, there was something to link this unusual activity in the counter and the exchanges/ SEBI will be justified in launching an enquiry.

3 Likes

“459 fully paid-up equity shares of INR 10 (Indian Rupees Ten) each of the Transferee Company for every 10 equity shares of INR 10 (Indian Rupees Ten) each held in the Transferor Company 1.”

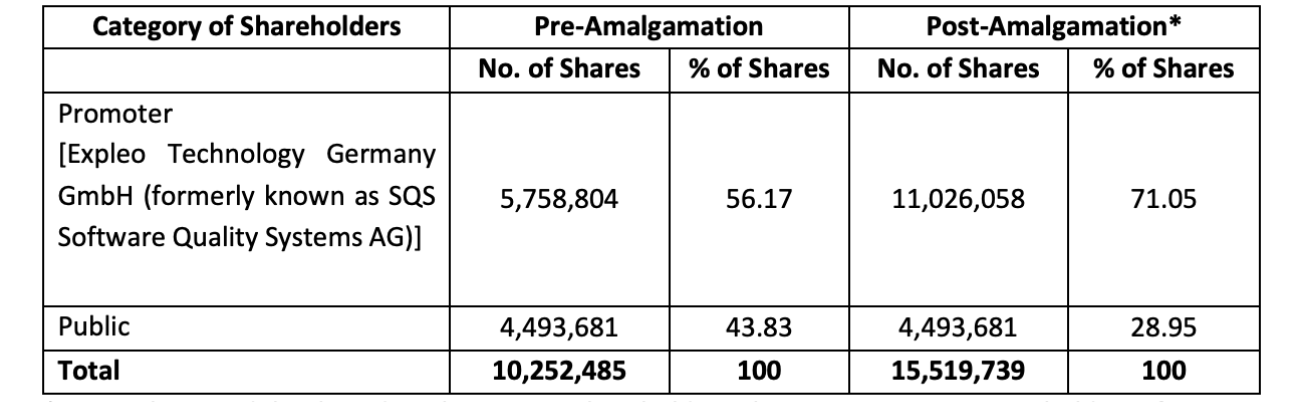

The way the equation for the minority shareholder is going to change from 44% to 29% and the way the promoters are consolidating their shareholding from 56% to 71% is affecting my conviction in holding the company in a negative way. Wont the Earnings per share come down?

44% for the minority shareholders was almost close to the 56%. Now the promoters has simply consolidated by a share swap without any cash transfer and emerged stronger and made the position of the minority weaker.

This is a merger without any cash consideration. Would Expleo Solutions endup with a lot of Goodwill in their books by overpaying for the assets in the private companies being bought (merged) ?

1 Like

How does the absense of cash consideration matter? There are real money making businesses that are getting added for the dilution. The sales per unit of equity will go up by about 33% (Sales have gone up 90% and equity base broadened by about 50%) Earnings per unit of equity will likely go up too, so long as the companies being merged were even half as profitable as the listed entity.

Well we have to be sure about how real are these " real money making businesses" since this is a no cash merger. The assets can be overpaid and the promoters might benefit due to this.

The minority dont get the benefit, they only get weaker due to dilution.

1 Like

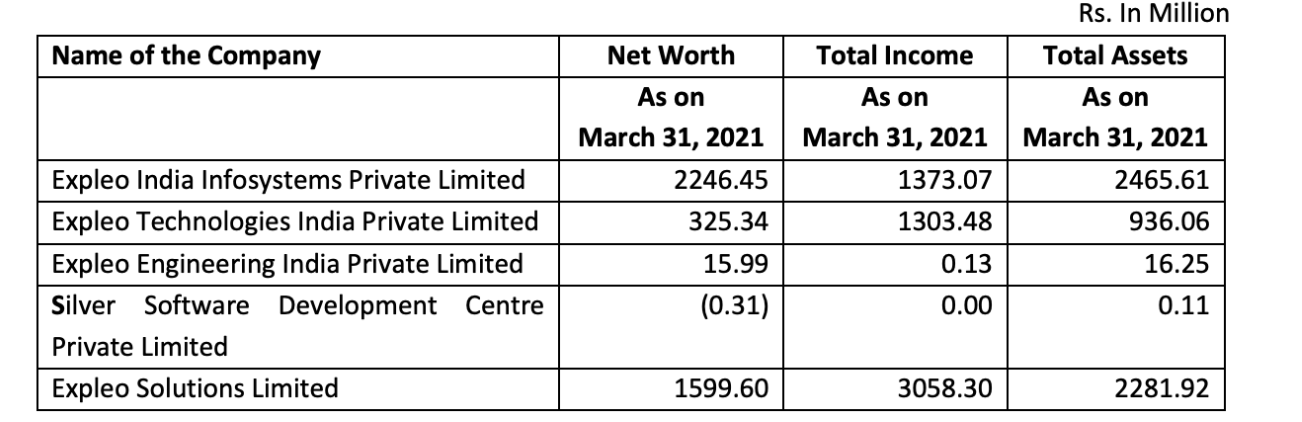

Expleo infosystems & Expleo Technologies are cash cows & generate cash flows though the contribution of former is substantially higher.

Expleo infosystem has a global delivery center at Pune with a head count capacity of 5000 & around 2.5 lakh sqft, & caters to both BFSI & non BFSI segments of telecom, Retail, manufacturing, Energy, etc

The engineering & silver software units ,are babies with virtually Nil contributions as of now, but can be easily ramped & are future cash cows.

The promoter increasing stake is a plus point, infact I would be alarmed if they were to reduce stake.

So all are cash or money spinners & the cash in books as well as their assets would go to the amalgamated entity.

IMO , there are no good will valuations, as all entities come under the Expleo brand umbrella.

5 Likes

What #Visanty is saying is goodwill in the merged entity which looks like will happen. The total value of assets transferred is Rs3417 cr but value of shares issued in the listed entity as per yesterdays price of Expleo(price of Expleo on the date of approval of merger is Rs912) is 52.67 lac shares @Rs912 valued at Rs4803 crs. and the difference will go to goodwill in the merged entity.Need to wait and see the valuation report and reason for such exchange ratio and also if it gets approval of exchange/SEBI and shareholders.

I tried hard to understand the amalgamation deal but couldn’t understand how it will actually work . Can someone explain it please ?

Few doubts -

1- 459 fully paid-up equity shares of INR 10 (Indian Rupees Ten) each of the Transferee Company for every 10 equity shares of INR 10 (Indian Rupees Ten) each held in the Transferor Company 1.

Why share swap is mentioned for only Transferor company 1 ? Why not other 3 companies.

Does this mean 459 shares of listed Expleo Solutions are equal to 10 shares of Transferor company 1.

2- After amalgamation the equity base of listed company will increase and all the shares of 4 companies will go to promoters? That’s how promoter shareholding is increasing to 71%?

3- I went through other member’s comments and some mentioned that EPS and margin will decrease after amalgamation? How did they arrive at this calculation?

4- Merged entities have more assets but low turnover . What does this tell us? Is data available for last 5 years for those subsidiaries ?

Any other info anyone can provide about this amalgamation ?

@Balki Your response will be highly appreciated.

Sorry for my ignorance.

1 Like

Company 1 has subsidiaries which is company2 and company3 and Company4 is a subsidiary of I think company2.So on a consolidated basis shares will be issued only to company 1.

Equity of company1 will be swapped for equity of listed co.

Other answers quoted were based on some one guessing.The company has just released the investor presentation and the name of advisors(JM Finance- a reputed co apart from Bansi Mehta) in M&A and the merger is EPS accretive post merger.

1 Like

Dear itsnithin ,in simple words ,all 4 cash rich private entities of Expleo group viz

- Expleo infosystems pune

- Expleo Technologies

3)Expleo engineering - Silver software development

Will be amalgamated with Expleo solutions & will become fully owned subsidiaries of Expleo solutions , such that equity capital will increase from ₹10.25 cr to 15.51 cr , with the parent stake increasing from 56.17 to 71.05 percent, while public holding will reduce from 43.83 to 28.95 percent.

Now I see floating stock at 18 percent as Rajasthan global securities, AIF & HNIs hold around 11 percent.

Now, all the private entities are cash & asset rich & Zero debt . They are all cash cows , however certain non BFSI segments like Retail, energy, manufacturing & engineering have been affected in the past year, due to covid lock downs , though the BFSI business has done well.

The pune unit is a global delivery center & derives almost 55 percent from the BFSI segment & 45 percent from the Non BFSI segment.

Being an MNC owned by Europe’s largest PE investor, managing & running over 135 companies, there are no window dressing or fudging of accounts or diversion of cash & all accounts have been audited & there are no corporate governance issues with Ardian.

4 Likes

In Particular, IT sector is in cusps of growth, driven by necessity in Digitalization, cloud, security surveillance, Data analytics etc & post amalgamation, turnover, profit margins as well as EPS are expected to increase substantially on synergies, perhaps even at 2.5 X.

Now 5 year financials are available for all private entities of Expleo, as they are audited & corporate & other taxes paid, though not in public domain, being a private entity.

Ardian is known to ruthlessly ramp growth & profitability & that’s why the Expleo brand umbrella has been created .

1 Like

The promoter increasing stake is a plus point, in fact I would be alarmed if they were to reduce stake.

Maybe it is a plus point for the promoter since they are benefitted due to their share holding of both the transferee and transferor companies. But as minority holders of the Expleo Solution, it looks like the dilution of our shareholding does not seem beneficial to the minority right now.

Ardian is known to ruthlessly ramp growth & profitability & that’s why the Expleo brand umbrella has been created .

The growth and profitability of Expleo solutions has been excellent in the past. Hopefully if they are able to do the same after merger, presuming Ardian will be successful to ramp up growth and profits in the case of Expleo, then all the shareholders stand to benefit.

Reflecting to the new development, I find this situation counter intuitive. That is on one hand the minority shareholding is getting diluted, and on the other, they stand to benefit if the company performs and earns well as they have done in the past.

I will not comment on the dilution ratio , however amalgamation is legal tender & sebi is in for protecting minority shareholders.

You have not made clear, how it is not beneficial to minority shareholders. Do you mean to say that dilution of equity should be less & parents shareholding should be capped at 60 percent, instead of 71 percent.

Ultimately what matters is capital appreciation in share prices, ( for minority shareholders ) , which is brought about by increasing growth & profitability.

A high promoters stake will ensure, more involvement of the parent, in ramping profits.

The question you have raised is whether the valuation of private firms of Expleo group to be amalgamated with Expleo solutions in lieu for parents stake in Expleo solutions to 71.10 percent through share exchange between the transferor & transferee company in the given ratio is fair or not?

Well, that’s for sebi regulations to play out,& protect minority shareholders, in case the valuation are unfair.

3 Likes

Let’s take a worst case scenario like when the transferee company might have overpaid for acquiring the assets of the transferor companies. I understand this is a pessimistic view of taking this development but certainly not improbable.In such case, the dilution resulting due to the merger would be detrimental to the minority group.

Ultimately what matters is capital appreciation in share prices, ( for minority shareholders ) , which is brought about by increasing growth & profitability.

A high promoters stake will ensure, more involvement of the parent, in ramping profits.

Yes sir, Capital appreciation will be what all the shareholders would want. And yes, High Promoter stake will ensure it. Lets hope that the company performs well after the merger. There is nothing wrong in waiting and seeing how it pans out since it has a good track record. It’s just that I am not comfortable with the dilution.

Thanks!! What do you mean by EPS Accretive merger?

As you rightly said, the excess amount paid for acquiring the assets becomes the goodwill. Since transferor and transferor have the same parent, they are overpaying for the asset. Would’nt it better for expleo solution’s shareholders to pay 3417 crs instead of 4803 crs without any goodwill ( I am not sure if this option is possible) ? There are counter intuitive point of views presuming what happened in the past would likely continue in the future. I am happy with the company’s performance but this acquisition would weaken my conviction.

It looks like the minority shareholders are being squeezed out by diluting their shareholding;

Please refer How Majority Shareholders Can Remove Minority Shareholders or Reduce Their Value.

There are several methods for reducing a minority shareholder’s value in the company, including:

- Encouraging or forcing a share buyout at a discount price;

- Diluting the holder’s stock shares;

- Restricting the shareholder’s access to corporate records, financial information, or key business records;

- Discontinuing distributions to minority holders; and

- Voting to terminate the shareholder.

Often, majority holders use multiple methods to remove a minority shareholder or reduce their influence in the company.

I’d request all to please see the investor presentation. The total PAT of the merging entities is 379 crores and PAT of the listed entity is 504 cr. That’s an increase of 75% for the consolidated entity.

The share dilution is almost exactly 50% for us. So the EPS is now 1.75/1.5 of the present EPS which is an increase of 16.6%. It is a good deal.

5 Likes

Let us wait and see the valuation by the valuers.

How do you know whether the merging unlisted cos were not window dressed to make it more attractive?

There needs to be a trend to conclude.Also paying Rs1400 more for the assets is a concern.

There has to be more information to make an opinion.

1 Like

Hi ,itsnithin

All the 4 private Expleo entities are in the field of BFSI & non BFSI segments of quality assurance, security surveillance,managed services solutions, cloud computing, data analytics, Robotic process automation, mobile testing applications, internet of things.

Silver software development is for developing & delivering software tailored to specific requirements.

The whole world, manufacturing industries to logistics to shipping, aerospace & automobiles, telecom etc is running on software, which will require updates & security surveillance.

So all 4 private entities have business synergies related to software, though it belongs to BFSI & non BFSI segments.

Post amalgamation , Turnover, profitability & EPS are anticipated to increase.I foresee EPS at ₹100 plus levels.

Regarding equity dilution, valuation & share exchange ratio of transferor & transferee , Goodwill if any, minority shareholders protection, all are to be decided by SEBI Regulations.

1 Like