"The merger between the two companies was initially announced in August 2020, with the Competition Commission of India (CCI) granting approval in February 2021. Following this, the Bengaluru bench of the National Company Law Tribunal (NCLT) also gave its approval.

However, the deal faced its first obstacle in March 2023 when the Chandigarh bench of the NCLT halted the merger due to concerns raised by the income tax department. In response, Indiabulls decided to challenge the NCLT Chandigarh ruling at the NCLAT.

After extended deliberations, the NCLAT has now approved the merger, dismissing the concerns raised by the income tax department and other parties. This ruling aims to resolve the issue that has spanned over four years."

What implication does this order will have? How do you read the order in terms of Revenue potential from this merger and any unexpected positive outcome you believe can be created here going forward?

By ‘culprits’ I assume you mean Tejo. IMHO he has no locus standi. His plea has been rejected by SEBI, NCLT and NCLAT summarily, I don’t see why SC will entertain him. He tried going to HC as well earlier but was told that HC wasn’t the right forum for his complaint.

Do note that NCLT Chandigarh, did not reject the merger plan because of the objections put forth by Tejo but because of IT Dept and the later won’t be going to SC because they have informed the NCLAT that they are ok with the merger till their interests (tax due to them) are taken care off. For that, the Company has filled affidavit that they will ensure payment of all taxes due.

I agree with the other members that the Hon’ble Supreme Court would not indulge itself or even entertain a plea in this matter now at the lower courts have released a very detailed speaking order in the matter concern and as far as Appellete is concerned, it will be presumed that all the QUESTIONS OF FACT have been scrutinized duly. In order to invoke SC jurisdiction the appellants will have to explore any QUESTION OF LAW wherein Interpretation needs to be pondered upon. So I believe appellants wont stand before SC

Embassy Developments Ltd. (EDL), via its subsidiary, has signed agreements with Lam Research India to sub-lease and later divest ~25 acres in Whitefield, Bengaluru, for ₹1,125 Cr, pending regulatory approvals. A significant deal in Bengaluru’s real estate and semiconductor space!

company had raised ~1000+Crs through conversion of warrants issued to to Blackstone, Microlabs and Embassy promoters. Exercise price was 111 per share.

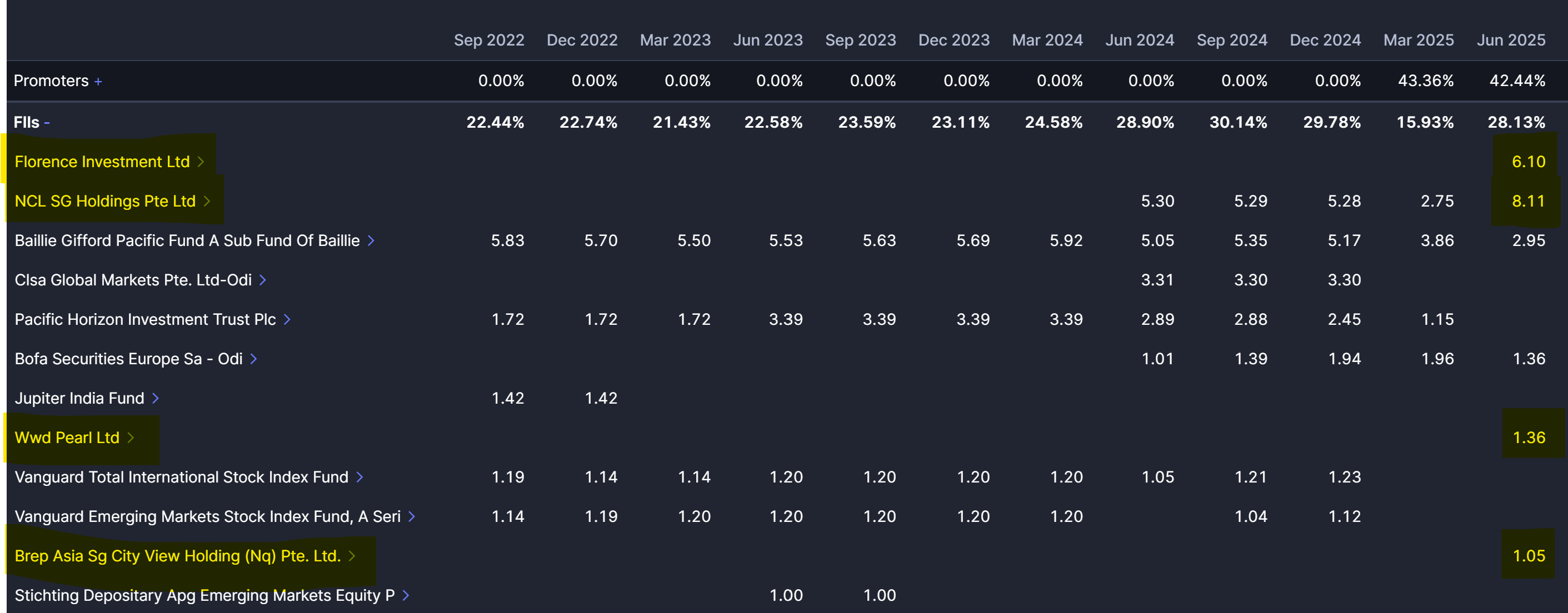

FII has significantly increased stake btw in Q1

This is a critical development. The erstwhile promoters had given guarantee to Canara Bank for a facility to group company via Indiabulls which is now Equinox. Pls note that EMBASY Group had taken over the Indiabulls post proper IBC process via NCLT. The group company defaulted in 2017!!. Now Canara Bank has approached NCLT for resolution post management change. India’s IBC is still a difficult process. There are still lot of loopholes still available in IBC that makes it really difficult for a new management to takeover.

What’s the outlook looking like on this? Good idea to continue holding or just sell at any price and completely exit? My initial buy price was 54 and current average is 78 so still not at a huge loss tbs.

Not sure. Don’t have concerns about Embassy as a group, but the liability involved is quite significant — the claim amounts to around ₹300 crore. Another point to note is that with this filing in the NCLT, there’s a possibility that other old creditors might also approach the tribunal with their claims, which could further add to the contingent liabilities. Need to monitor the case closely to see how the decision unfolds. For now, I’m continuing to hold my position.