Any thoughts on company getting GST notices frequently

Is anyone able to access the tender document for this CETP project?

keen to understand the eligibility and technical guidelines

1 Like

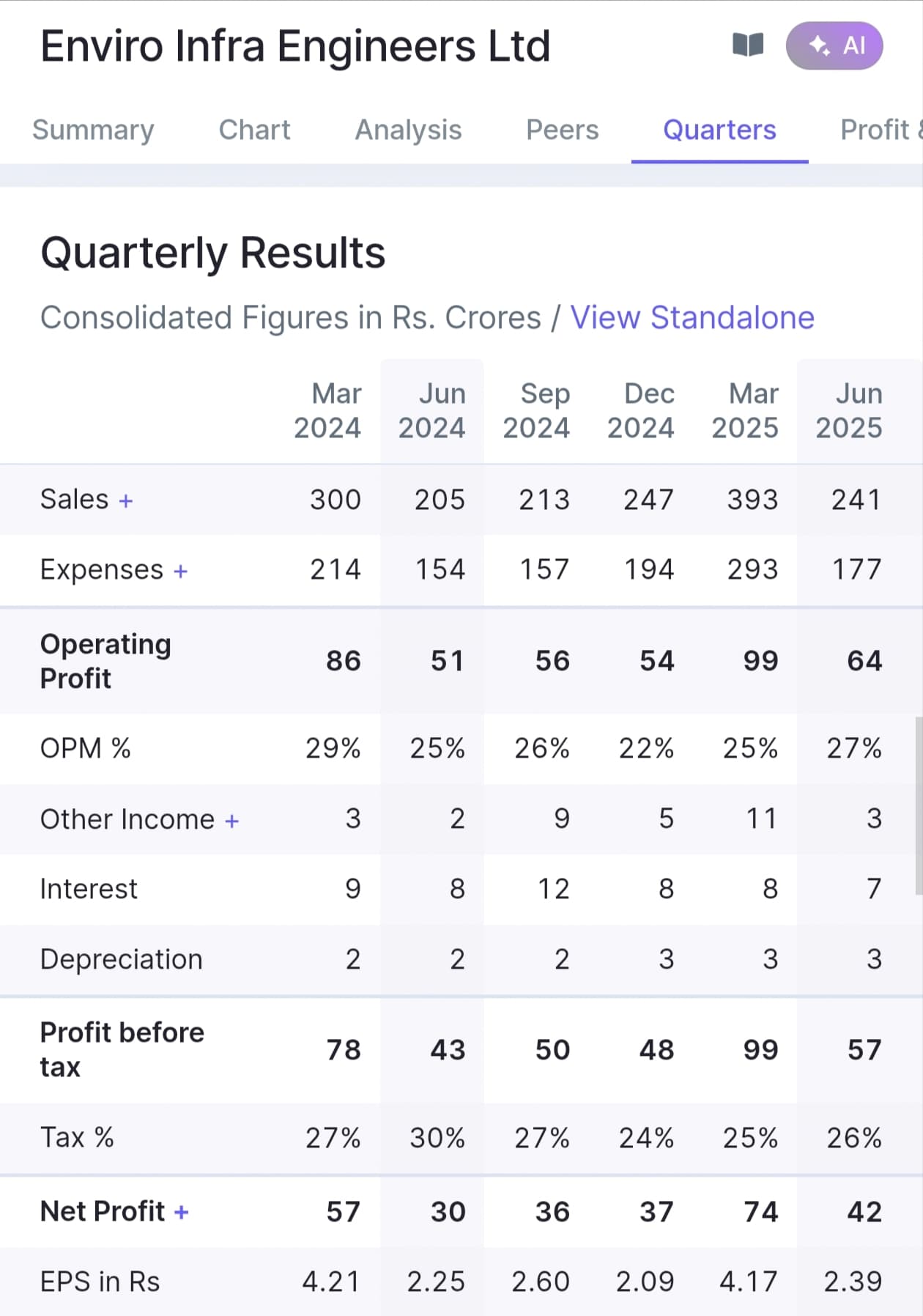

The company has won orders worth 1178 crores since the beginning of the financial year.

3 Likes

#EIEL is where #Transrail was a few months ago.

With 40% growth

Fy26 PAT 247cr

Exit P/E can be 30 because management expects better than 35-40% growth in Fy27

So Fy26 expected Mcap 7434

Current Mcap 4288

Upside ~ 73%

242 —> 418

Management Interview ~ https://youtu.be/-QzLQp6b5DI?si=ECXlFQ1sQOaxIudy

#EnviroInfra

Concall Link ~

21:07 ~ We expect the company to grow at 35-40% for atleast 4-5 years.

Fy28 pat could be 450-500crores

800 -1000 price in next 2.5 - 3 years is very much possible.

#EnviroInfra #EIEL

Above 391.6 ~ IPO base high 601 levels opens up

3 Likes

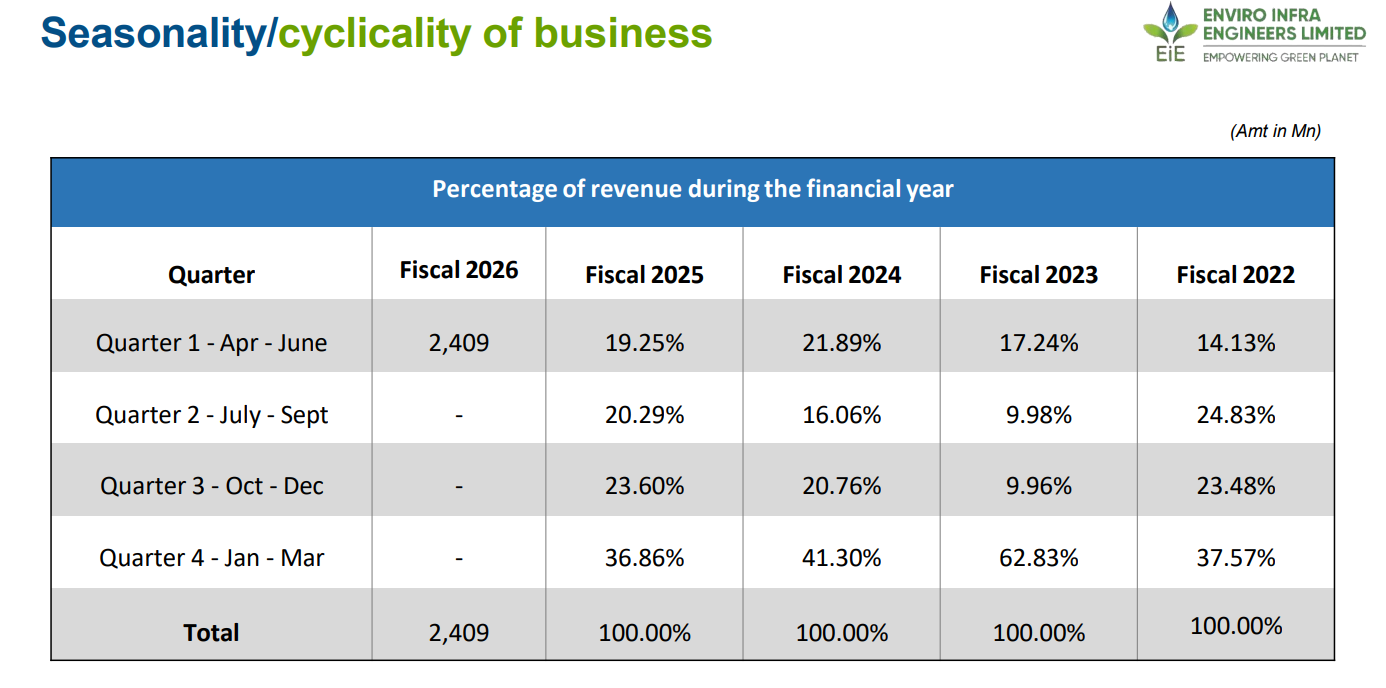

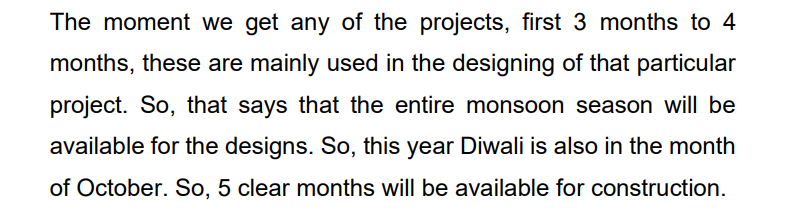

The company has presented a very optimistic picture in its recent call. The company is projecting 35 to 40 % CAGR growth for the next 5 years and EBITDA guidance in the range 22 to 24 %. The company has explained the seasonality of the business well.

Usually, the projects execution picks up in the last 5 months of the year.

So far this year, they have been received orders worth 1178 crores this year. Most interesting of them is the MIDC ZLD order, which marks its foray into ZLD space. This year many of the STP players EMS Ltd, VA Tech Wabag have been reporting good order inflow.

EIL doesn’t have any de-salination projects, but has plans to venture into this field with some other partners.

The company is also L1 in many other projects and expects more order inflow.

They also mentioned that they prefer projects where land is readily available.

10 Likes