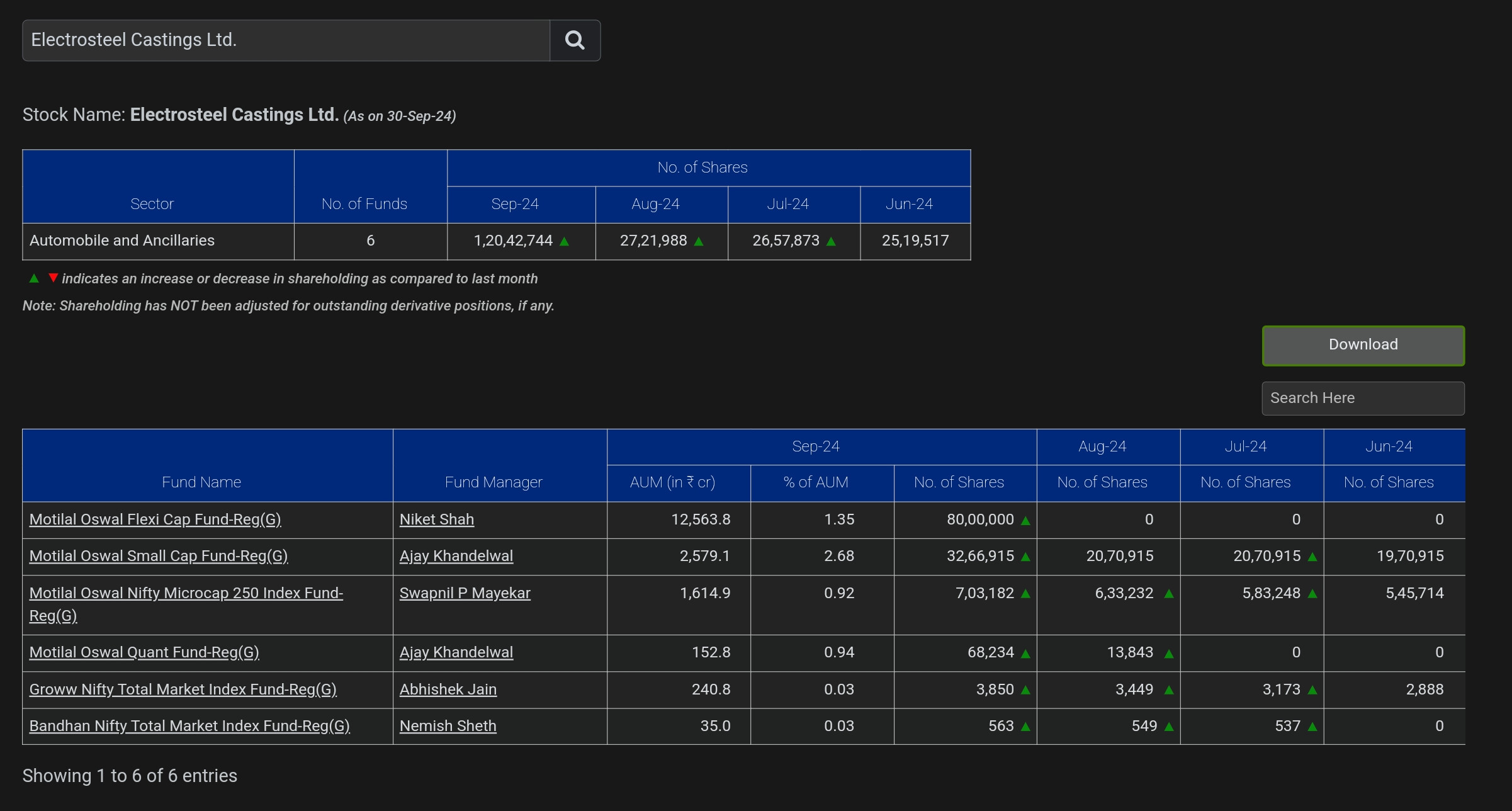

MotilalOswal sells 1.96pc (edited: corrected)

MOS sold 1.96 % out of 5.05 %.

It as sell side transaction not a buy.

It seems Motilal is operator riding this stock. While it sold 1.09 crores of shares in its personal capacity in September, may be part of some PMS or its treasury money, at the same time, through open market, it bought roughly 1 crore of electcast shares in its various mutual funds schemes as seen below

So net, nothing bought or sold, just reshuffled in open market to create margins of safety or price movements desired.

Be wary of such operator runned stocks.

1 Like

This did not age well. It’s down 10% in a single session today. The stock nosedived into stage 4 before anyone could figure out what was happening. I’m invested and facing a significant loss.

Some important points from the November 2024 concall:

Risks

● Raw Material Price Volatility: While recent trends show a downward correction in raw material prices, especially coking coal, this volatility remains a risk factor. Electrosteel mitigates this by using back-to-back contracts for 5-6 months of their order book, but a sudden surge in prices could impact profitability, especially for the 25% of the order book that remains open.

● Competition: The DI pipe market is witnessing increased competition. While Electrosteel is a leader with a 19% market share, new entrants or aggressive expansion by existing players could pressure margins.

● Government Policy Changes: Government initiatives like Jal Jeevan Mission and AMRUT 2.0 are significant demand drivers for Electrosteel. Any policy changes or funding cuts to these programs could impact order inflow.

● Geopolitical Risks and Ocean Freight: Electrosteel aims to increase its presence in export markets. Geopolitical uncertainties and fluctuations in ocean freight costs can impact export volumes and profitability. The Russia-Ukraine conflict is a relevant example impacting global trade and shipping costs.

● Blast Furnace Stability: The recent shutdown and slower-than-anticipated stabilization of the blast furnace at the Srikalahasthi unit highlight operational risks. While management is working on solutions, recurring issues could impact production targets and profitability.

● Execution of Greenfield Project: Electrosteel is investing in a Greenfield project to expand capacity. Delays or cost overruns in this project could strain finances and impact future growth prospects.

Future Sales and Margins

● Sales Volume: Electrosteel expects to reach a sales volume of around 850,000 tonnes in FY25, a 13.8% growth compared to FY24. The company aims for 900,000 tonnes per annum by FY26 and 1 million tonnes by FY27, demonstrating a growth-oriented strategy.

● EBITDA Margin: Management expects to maintain an EBITDA per tonne of INR 15,000 to 16,000 in the near to medium term. This translates to an EBITDA margin range of 16% to 18%. They believe this is achievable due to stable demand, operational efficiencies, and potential benefits from softening raw material prices.

Overall:

Electrosteel Castings Limited presents a positive outlook on sales growth driven by government initiatives, capacity expansion, and a robust order book. Management is optimistic about sustaining healthy EBITDA margins. However, risks like raw material price volatility, competition, and successful execution of growth plans need careful monitoring.

3 Likes

Even I am surprised at the fall but fundamentals are intact so it is a good time to average or buy.

Exited a while back.

Heavy selling from Motilal Oswal.

Saw somewhere that they are selling from one fund & buying from another - haven’t fact checked this.

Are the FIIs selling or just Motilal funds

Is it a Value Trap . Seems too cheap

sir any specific reason of motilal oswal fund ???

The stock has corrected by 45% from its high… Fundamentals are attractive and looks cheap. Any particular reason for major sell off?

1 Like

With recent SEBI order there is a direct involvement of company management and promoter in inside trading. Clear equation of “Corporate Governance” issue.

Bad management and Bad timing.

SEBI Order link

2 Likes

MoneyLife had shared the insider trading news on Electrosteel. Insider Trading in Electrosteel Casting by Promoter Group Entities before Merger with Srikalahasthi Pipes?

SEBI is really doing a shoddy job, announcing the result of this investigation almost 4 years later. I guess Ms Puri was busy with the colocation scam and decided to release these as her tenure was not renewed so she would not financially benefit any longer for these cover ups.

The stock has run up from 35 odd to 230 which certainly seems some kind of circular trading or pump dump operation is at work on the stock currently. Valuation wise the stock is cheap compared to the market and competitors if the financials are not fradulent. But given that the promotors wanted do a 8 Cr fraud in 2020, chances are high that the stock run up is artificial or the profit and loss numbers are madeup. If it were not so then at such ridiculously cheap valuations it would be a major target for acquisitions by AIA/Mahindra CIE/Ramkrishna etc.

Is it worth buying, maybe if you have risky money, but certainly at Rs 35 or lower.

4 Likes

There are three parts to this stock

- Valuation is cheaper - P/E - 10.5; Company has business in 100+ country and its very old company

- last quarter results were very low EPS fell to 1.44; similar EPS was recorded in June 2023.

Bigger point here is price of its material (DI pipes) have also fallen after rally of 2 years - Promoter credibility is not so good due to insider trading

Disc: Have holding in these stocks

2 Likes