The stock has been on upper circuit since last four to five trading session.i.e. since the release of this report. So actually it has gained at least 20% in last four days.

eimco elecon AR fy17 notes

Topline up by 26%

PBT up by 26%

PAT up by 43%

5 rs dividend

Debt free

74% promoter holding of which 25% is owned by MNC

MF’s hold 4.79%

CIL has targeted for a big leap in the production (approx. 19%) this year to compensate for the last year’s slow growth.

The pressure on the coal subsidiaries to reduce the production cost is forcing them to think about newer technology. This is going to create increased demand for the mass production of machines with ease of selective mining. This opens up a big market for the equipment manufacturers and scope of innovations suiting to the Indian coal deposits and geological challenges.

With the Government’s constant impetus on infrastructure, the construction equipment industry has started showing signs of growth from the continuous falling trend of last three to four years. The Government has instilled a positive outlook in the country by reviving stalled

infrastructure projects, announcing new projects and is also allocating huge investments in infrastructure industry. Also, the major growth drivers for construction equipment industry will be, focus on timely execution of projects through improved governance and easy availability

of finance. Awareness and emphasis on qualitative approach will lead to focus on high quality and technology driven equipment. Growing urbanization and Increasing affordability is expected to further spur up the demand for construction equipment in near future. Based on the recent projections, the ECE (Earthmoving & Construction Equipment) market is expected to grow by around 10 to 12 percent over the next few years.

After a subdued phase of last 4 to 5 years, owing to policy paralysis and

global recession, recently Construction Equipment Industry has started

showing a sign of recovery, at a back drop of increased highway

construction, improved government spending on water revitalization &

building new cities. A number of domestic players, who have expanded

their capabilities or diversified their product portfolios, through

collaboration & tie-up arrangements, have now started take advantage

of these signs of improvement in economic scenario.

Interlinking of rivers has started showing growth results for primary construction equipment (earth-moving) which will further continue for secondary equipment (material handling) on the mid and long term basis. An improved version of AL-120, a mid-sized Compact Wheel Loader with 2.3T

pay load capacity, has been introduced with superior features, which will help it, carve its product positioning among similar equipment presently used by builders & contractors.

A higher capacity Loader AL-520, with pay load of 3.5T has also been introduced in the

market place against heavy competition from national & global players, considering

the higher demand from this segment. Continuous focus on improvement in current distribution network has helped spread this product in certain pockets of the nation, which will be further

improved upon in the days to come.

Skid Steer Loader, a highly versatile machine having a growth potential & primarily used in

Industry material handling as well as infra projects, is also on the

anvil of launch pad.

Additional product lines in Construction Equipment Segment, as proposed by reputed market survey agency, will also help your company realize its growth objectives in years to follow.

Further on, your company is also exploring export potential of construction equipment in market of South East Asia & Africa.

With the all-round revival of coal companies and introduction of state-of-the-art technologies products for mining sector, your Company is expected to do better in the coming years.

The main risk and concern of the company remains that it will continue to depend more on Government clients for some more time.

From the balance-sheet (consolidated)

Current financial Investments 22->55->69 cr over last 3 years.

Receivables 88-> 51 -> 48 cr over last 3 years

Non current financial investments 60.28->70.98->76.79 cr over last 3 years

Valuation Analysis

Mcap = 344 cr

Fin Investments + Cash = 148 cr

EV = 196 cr

PAT = 25 cr

4 Likes

Cash = 150 Cr

Mkt cap = 128 Cr

Dividend Payout is 15% on an average which is less considering cash.

Dividend yield is 3% due to low valuation right now.

With Operating Profit of 15 Cr and a history of decent performance, looks like mkt cap of 250 cr can be justified. Anyone following the stock ?

Recently I have started study on the company. Appointment of Mr. Vishal Begwani seems to be the move in right direction. Dependence on Coal India is a challenge, how company can mitigate the risk. Diversification is the way out and company has plans for the same.

Seek any other information if available with fellow investors

2 Likes

Annual Report

Refer to page 37, piling rigs seems to be the way-forward.

3 Likes

Subsidiary of Elecon engineering which is a 2 billion dollar mcap. It’s listed separately becase of a JV with a Swedish company in 1974. Only Indian company to make underground mining equipment, Coal India is it’s major customer in India. It’s a monopoly business in India.

Monopoly business in India: Eimco has a near monopoly in the underground coal mining intermediate technology equipment industry in India

Growth triggers: CIL(Coal India Limited) aims to increase production of UG(Underground) coal from ~35 million tonne (MT) in fiscal 2023 to 100 MT in fiscal 2028 and 120 MT in fiscal 2030. That’s a nearly 4x in 6 years which should help Eimco as they are the sole suppliers of some of the machines. CIL’s Capex to quadruple in 6 years and the phasing out of import is also 6 years.

A mid-to-high double-digit trend in growth could continue as the UG coal mining industry shifts towards newer, technologically advanced products such as continuous miner packages. Operating margin also improved to 16.3% from 14.5% in fiscal 2023 due to improved operating leverage and better product mix.

The company has been able to reduce its dependence on the UG coal mining segment (wherein output has faced a downturn in the past) to less than 80% in fiscal 2024 from over 90% in the years leading up to 2022.

R&D: Continuous improvement in the effectiveness of equipment; while catering to diverse applications further aids established market position. Continuous miner was a result of in-house R&D, this was not available in India and is contributing to order book.

Improving margins: Strong in-house research and development team enables continuous improvement in the effectiveness of equipment; while catering to diverse applications further aids established market position.

Positive industry change:

-

CIL will start tapping into abandoned underground mines. Coal India awarded 23 abandoned underground coal mines to private operators: coal india awarded 23 abandoned underground coal mines to private operators | ICICIdirect

-

Start phasing out of mining equipment in India by next 6 years.

Expected increase in orders from Coal India Ltd following its efforts to enhance output from the underground (UG) mines and focus on reducing import of coal mining machineries. Not limited to just coal but also minerals and metal mining.

Product mix change: Reducing dependence on UG equipment, down to 60 percent from 80. Getting into infra equipment as well - need to check the overlap with existing manufacturers(ex: ACE).

Regulatory reforms - Coal production and emphasis is increasing and is supported by the govt:

-

India approves $1bn budget to support coal gasification: India approves $1bn budget to support coal gasification | Latest Market News

-

Coal reforms 3.0: Coal Reforms 30 Centre aims zero imports more coal for nonpower | News - Business Standard

-

Phasing out of all coal reforms by 2025: India aims to phase out coal imports by 2025, focuses on energy security, ET EnergyWorld

One could expect incentives for coal in the budget in July! Incentivizing the industry, and there is only one player.

Ministry report titled “Special focus on domestic production of mining equipment”

“Currently, Coal India Limited (CIL) imports high-capacity equipment, such as Electric Rope Shovels, Hydraulic Shovels, Dumpers, Crawler Dozers, Drills, Motor Graders, and Front-End Loaders Wheel Dozer, valued at Rs 3500 Crores, incurring additional expenses of Rs 1000 Crores in customs duty. To curb these imports and boost domestic manufacturing, CIL has devised a strategic plan to phase out imports gradually over the next six years.” Even if 10 percent of the capex(minus the customs) comes to Eimco, it will double it’s topline(need to check it’s requirements and Eimco’s product match for a more precise number)

Financials - Not much debt. Decent reserves and almost 180Cr of liquidatable investments. Low float stock, can trade from circuit to circuit, not for the faint hearted. Based on the vaahan website data, the June quarter can be a good one. FY2024 revenue is the highest, increase in sales, margin as demand is increasing. PAT trend is also positive.

Risks: As a B2G business it has stretched creditor days, debtor days, inventory days. Client concentration risk.

17 Likes

Q1 results. Excellent numbers.

Disc: Invested

1 Like

Company needs to enter into manufacturing of diverse and more complex mining machines for import substitution and also to be able to increase it’s export footprint.

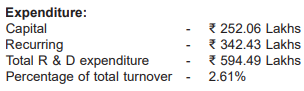

They haven’t announced any capex so far. They have however increased their R&D spend from 2.8Cr to almost 6Cr.

R&D spend FY23:

R&D spend FY24:

So I would assume they haven’t been able to come up with anything tangible from their R&D efforts yet this year. Once they have made progress here they may look at capex. Also their cash seems to be 0, they may have to raise capital for any further capex depending on the quantum of it.

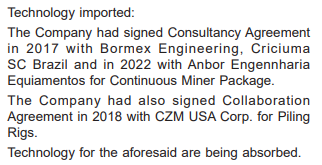

Their recent products, Continuous Miner and the Piling Rig seems to be a product of their collaboration with overseas companies. It’s imported technology that is being absorbed and to be adapted to Indian conditions:

Does this mean they don’t have the competency to come up with new tech on their own? And that warrants the increased R&D spend.

3 Likes

May be @Tar @Worldlywiseinvestors can be add their observations here.

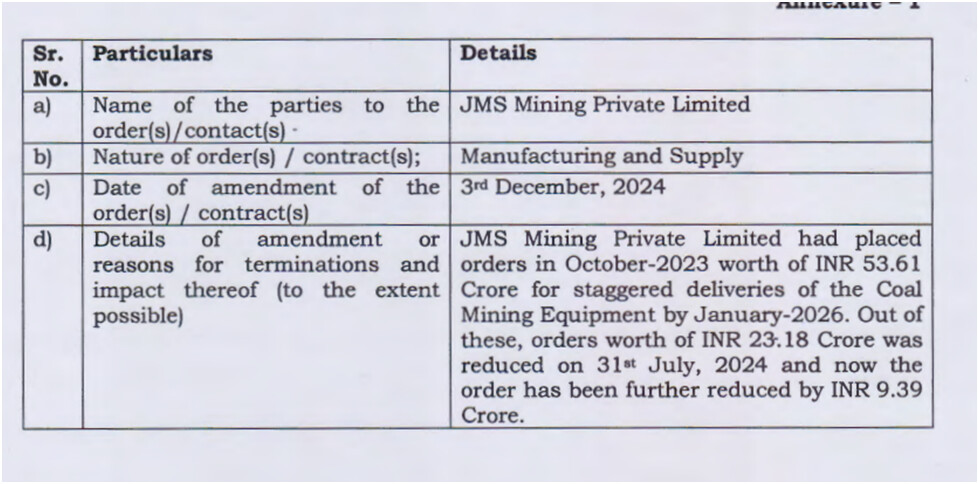

Eimco Elecon (India) Limited announces a reduction in awarded orders from JMS Mining Private Limited by INR 9.39 Crore, impacting deliveries scheduled for FY2025-26.

This follows a previous reduction of INR 23.18 Crore reported on 31st July 2024, reflecting ongoing adjustments in contract terms.

3 Likes

any idea why the reduction happened. Is it similar to order cacnellation?

These orders were related tio Continuous Mining Packeges?

Compiled some notes from AGM of 2024 & AGM of 2023. Also made some notes. Highlighting thesis & antithesis.

Sharing the doc file.

EImco Elecon.docx (534.9 KB)

Also pasting it here

AGM 2024

- Your company has achieved the highest ever revenue of 227.28 crores during the financial year 23, 24, which shows increased by around 31.60% as against rupees 172.70 crores for the previous year 2023. The net profit after tax for the financial year was rupees 40.41 crores as against 20.87 crores for the financial year 23, 24, registering a growth of 94%.

- Major highlight of the year were receipt of a couple of large orders for continuous minor miners and the components thereof. The successful execution of these orders will enable the company to improve its capabilities and tap the future opportunities.

- In the underground mining sector, the coming days will witness increase in demand for equipment catering to blast free technology in underground coal mines and big big size loaders and low profile dump trucks in the metal mines.

- Therefore, the future of the underground mining equipment market looks promising with opportunities in coal, mineral, and metal mining industries. Your company has been taking several research and development initiatives to develop new and advanced equipment to cater the growing demand for underground coal and metal mining industry. The government of India has made in infrastructure creation a major pillar for sustainable growth. The initiatives of the of the present government in promoting domestic players through Make in India initiatives has encouraged many domestic and international player to invest in infrastructure equipment industry. Your company has also taken the lead in manufacturing of piling rigs, which is a high end engineering product and for the cast in place piles, diaphragm walls, and foundation reinforced enforcement of buildings.

- Continuous mining (CM): It’s a very high productive business. It’s a blast free technique. CIL is moving towards this

- There are MNC players starting in CM tree now. One player will make some of the machines soon not the full packege. One needs to have minimum one year of CM products to be in service for tendering to CIL.

- 100 CM packeges for CIL in next 5 years. How many will come up actually depends on their execution capabilities. Right now we are not fully qualified but in next one year we’ll be fully eligible. We aspire to get all 100. Not all 100 will come to us. Right now we are trying to get qualified.

- For all our products we compete with the MNCs. We’ll give better value to our customers.

- Orderbook: (from latest credit report) The benefit to Eimco’s operations is evident from the growth in its order book to Rs 152 crore (highest ever increase; executable over the next two fiscals) as on December 31, 2023, from ~Rs 50 crore in March 2023. 70% comtains cm package. Not all of these orders are executable this year. 80% is executable in this f. year.

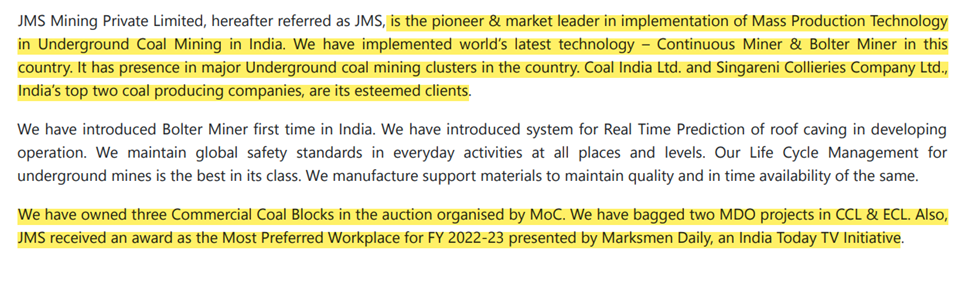

- JMS mining: esteemed customer of us.working with them for long.

- Sales breakup in FY24:

10% metal mining

10% CM package & components

35% spares business - Margins: And going forward, we look to maintain those these, levels of margins. Of course, there’ll be further expenditure on ramping up the support services going forward so that we’ll keep the margins levels in check going forward. So it will be challenging to increase it, further. On the CapEx, there were some questions. I mean, this year, we look to do similar on routine CapEx only to 10 crores.

- Related party: distrubution fee of 19 cr to related party it’s high. This is 10-11% quite high for distrubution. MTC is in sales network front. We have no marketing department. Cash on balance sheet:

- A CM packege costs 100-110 cr but it has other expenses also. Our older products have value of 1-3 cr. Opportunity size has increased. Typical CM package we are selling is about 40 cr.

- Typical CM package, what we are selling is around 40 crore. And, yes, our machines will, get approval, but it is not that easy also. It is a task in hand, and we know the complexity of, getting approval. And we the team you have to believe on the team that is working behind that. And, that is the immediate job in our hand.

- We’ll supply 2 continues Miners in this FY for which we got orders. This is to a private customer.

- What mgmt thinks in next 3-4 years horizon: Actually, we are developing the new products in, all the field, which has been asked, coal mines, the non coal mines and the construction business. We are, planning to keep the growth momentum of, say, 10 to 15% every year to year, continuously. And, I think, we are striving to achieve that.

- So, I think, there were questions about the piling rig also. The piling rig is under tremendous pressure with the Chinese competition. The quantity is growing, and we are developing more, piling rig, more models also to compete in the market. And, there is hardly any support from the government in that field on the import duty because import duty is hardly 7.5% on that. And, most of our competitors are Chinese. They are ruling almost, say, 95% of the market. And, we are the only one standing there. I can say the second one after Chinese who are able to compete with them.

- So order book at the start of the year, we have been, carrying around 140 to 150 crores worth of orders. So these were mainly comprised of the large orders which we got, which we announced, recently as well as last year. So and mainly, this, almost around 70% of the orders are for the CM package. Out of this order book, almost 80% we look to execute in this current year. Now on the revenue breakup, for the last year, there are some questions.

AGM 2023

- can do 400 cr revenue with existing facility.

- FY24 margin guidance was 12-15%. did 18%. revenue guidance was more than 15% but did 30%.

- I would like to share the key achievements of your company during fiscal 2022-23. Our indigenously developed roof motor, which is part of the continuous miner package, has been established successfully. Whereas the shuttle car, which is another component of the continuous miner package, is under trial and running successfully. We have successfully installed the man riding system in metal mine, which is the first time ever in India. We have executed the major order received for biggest size diesel loaders of 7 tons from Uranium Corporation of India Limited.

- We have developed new models of firing rig, namely EC 267 and EC 125. These are promising products and successful developments of these products augurs well for the growth of the company. The company also focus is also focused on developing new products, underground mining machinery and construction industry in the coming years

- Your company has also taken lead by manufacturing piling rig, which is high end engineering product used for cast in place tiles, die diaphragm walls and foundation reinforcement of buildings. These machines will find its market in all major infrastructure projects like road or railways or bridges, high rise buildings, dams, metros, and other infrastructure structures.

- Sandvik and Eimco Elecon are partners in the Indian company Eimco Elecon (India) Limited, which manufactures and sells mining and construction equipment

- Also, the metal mining sector would particularly. And, in India, the metal mining sector is also under expansion. So there will be growth in the demand for the our, non coal, products also. As already addressed by the chairman that, the filing segment, we are launching new products and our growth plan is to launch more and more products in the filing. Definitely, the construction segment is under the cost pressure because of because there is hardly any resistance by the government in construction machinery for, buying from China.

- The other questions were related to the CM product, products already. Chairman sir has informed that out of the 3 machines, what we developed in the package, one has already proven in the market and accepted by the market. The second product, which is under trials.

And, very soon, market acceptance also will be there. When I say market accept acceptance, it means that as, other customers also giving the order for that machine. And also the for pilot, for the continuous minor, the coal India, we are in touch with the coal India. And, definitely, we are working closely with them because their tender conditions are hindering us from putting it for trial in their minutes. So, that also will be resolved. - The main competitor for Continuous Miner are as Sandvik, Joy Global, they are the 2 big one, one more South African company and 1, company from the Germany is also there with a few products. Chinese are, of course, there and there will be, one more, Indian companies which are in advanced stage of developing it.

- I assure that the market of the continuous minor package is going to be sufficiently big for us to, get the major market share in that slowly. The product launch, as we have, as has been asked by, many, shareholders. Our product launch, we are having the products lined up for both blast free technologies and for the non coal mining and also for the piling rig. So we are expanding our bouquet from, what we have launched till now, and, we are targeting to launch the product regularly and in very aggressive way.

- The replacement cycle for most of these products for the last 3 technology product is almost 9 years. Whereas, the replacement cycle last, for our regular product is, 5 to 9 years. Different. And our major product till now is the LHD or the poll and non whole market.

- Revenue Breakup of FY23:

Construction: 15%

Non Coal: 35%

In terms of revenue mix, last year, we had, almost 42% from mining and 43% from our spare business, and construction was around 15%. Within mining, almost 50%. So the growth, which you see in the last year mainly came from the new products over, piling rig as well as, our LSTs for developed recently for the metal mining. So those these, the contribution of these products contributed to the growth in the last year. - Our plan is to slowly diversify more and more towards the non call sector, but still keep the leadership in the call sector. Our leadership in the traditional business Is our market share is almost 80% in the conventional products of the, the board and pillar, technology that is for

- What I would like to also tell the shareholders is that Eimco Elecon is at a juncture where they have taken up huge development. The machines that are being today developed and implemented or installed in the non ferrous mines or non coal mines, I would put it this way. Non coal mines, especially for zinc or copper, these are large capacity machines, and they are going they have been built for the first time in India by our design engineers. And I am proud to say that they have been working reasonably very well.

And this would compete with Sandvik and Atlas Copco. We are the only Indian company, who has developed these, and, we are proud that they would be not only, cost effective, but also functionally extremely good and reliable. Apart from that, the continuous miner, which has been developed by your company, is today, in the international market, there are hardly 2 or 3 players in the world who have developed these kind of products. We are proud that we have done it with the support of, Brazilian team, and, this also is reasonably successful. Together with the continuous miner, we have, the, a roof boulder. So and the shuttle car. So, these three products are also unique because, not only they have been built for the first time in India, but, as I told you, there are hardly 2 or 3 companies in the world who develop these kind of products.

They are very tricky, and I am very proud that our design engineers have done a tremendous, development in this area. Not only that, the support from our sister organizations, including the Elicon gear portion, they have been able to develop the, specialized gear unit, which is also very tricky for the continuous miner. So all these are new developments which your company has taken up. Yes, we have taken a bit longer to develop these. But once they go into the market, I believe that we will have a great future.

It is only a matter of time before we will be able to harness and exploit, these products and give them to Coal India, the contractors, as well as the piling rig also, which is, as you know, as we are the only Indian company, who has developed that. So all in all, we believe that the future is going to be very, very positive. Okay? And, we should see the next 5 years, we should be great for the, company. So I presume that this, gives you an idea of, the future.

And, as I told you, I will I feel extremely proud that we, as a company, an Indian company, are doing a lot for make in India, and we will continue doing so.

I would like to also add that the reason why I am not putting in any figures as to how much, we would be able to sell in the underground coal mines or the nonferrous or sorry. The non, non coal mines or the piling rig is because the market is dynamic. And, quite often, the tenders come in late from coal India as well as the government, bodies, and quite often, they take time to, conclude them. So it is difficult to lay out, the exact values, but I’m sure that the next 5 years, you will see a lot more happening and, the turnover also growing in the near future. Thank you.

Thesis

- Business has good operating leverage because no capex is needed for upto 400 cr revenue.

- Even with 15% growth they can show better bottom line growth.

- Under-promise and over deliver type mgmt.

Antithesis:

- Order REDUCTION from JMS mines: is related to Continues Mining machines? If yes it can hamper the growth story. Since the thesis is on CM products. The stock price corrected from first announcement of order reduction in July. The after Q2 earnings stock corrected further.

- Delay in getting orders from CIL.

- Lack of communication from the company.

4 Likes

There’s no mention of type of machinery involved in this order. But 60% of an order getting cancelled and that from a old customer is not a good sign. May be some slowdown in the sector or other suppliers have come up.

Recent report from Aequitas PMS (owned by Siddharth Bhaiya) published report where they put data on current Power sector situation.

Summary of report: There might be over investment in power sector as whole as of today because power demand is not rising much.

Aequitas too had held eimco elecon till March 2024 and have sold all their holdings as per the share holder pattern.

On the stock price front the biggest promoter Tamrock Great Britain Holding Ltd has sold around 14000 shares in Dec 2024 via open market sale.

@Tar @Worldlywiseinvestors if you guys can add your opinions it would be a learning experience.

2 Likes

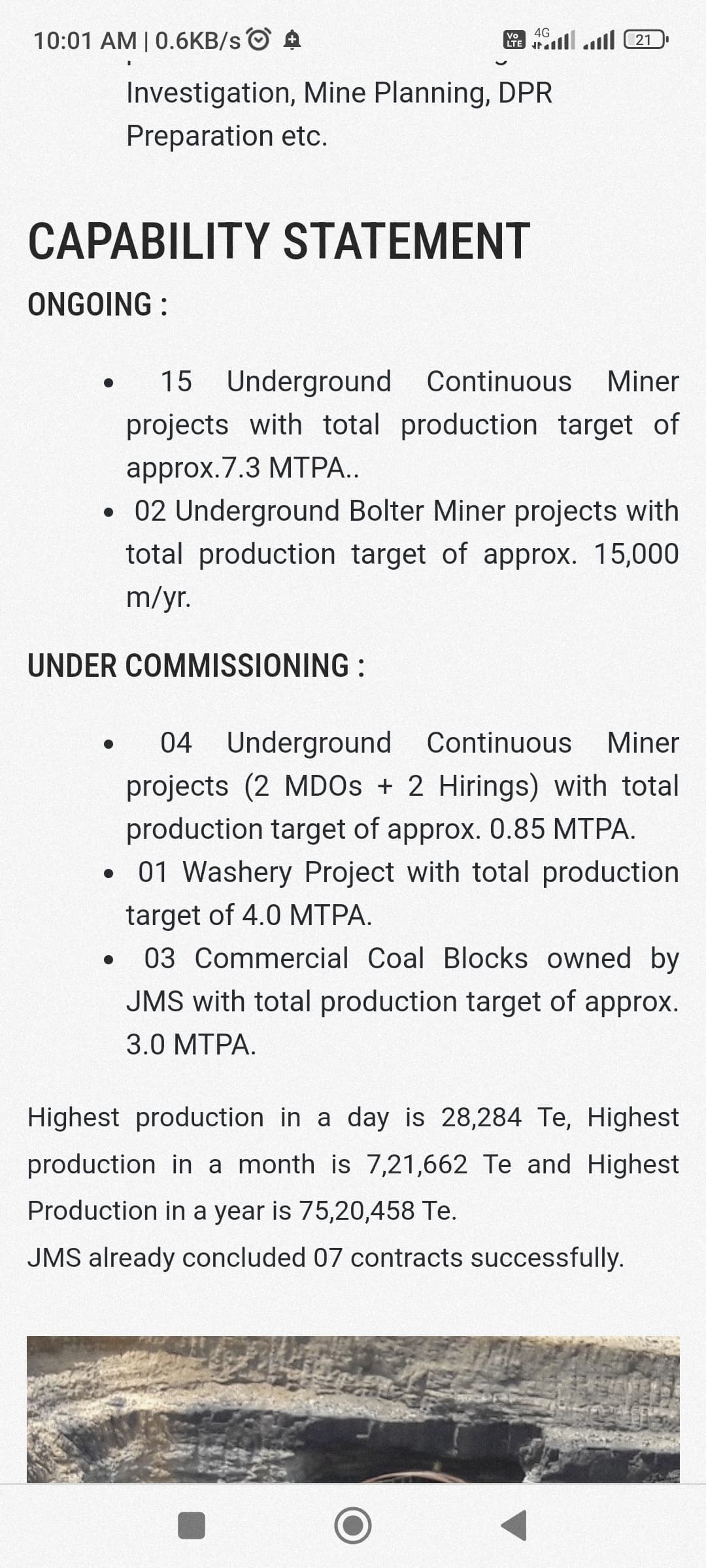

Most probably it’s continuous mining machines. This is what I found from JMS mines website. They are having 4 continuous mining projects under commisioning.

Disclosure: having a 1% allocation. Will increase if there is a sign of bottom formation on charts. When there is lack of information I take the help of charts to find if bottom formation is going on.

EIMCO ELECON: A potential multibaggar in a slow growing coal mining sector.

BUSINESS MODEL OF EIMCO ELECON:

Eimco Elecon manufactures mining equipments like Continuous miner, Feeder breaker, Roof bolter, various types of LHDs and Load haul dumpers, Shuttle car, Coal hauler, Side dump loader, Air motor, Universal drill machines, Rocker shovel loader, Hopper loader, Articulated wheel loader etc (pictures along with specifications are available on thier official website eimcoelecon.in). 80% of thier sales come from underground mining equipments. Coal India is a major customer.

BRIEF UNDERSTANDING OF INDIAN COAL INDUSTRY:

Indian coal production grew by almost 10% in FY 24. Coal india 774 MT, Captive+commercial coal blocks 154 MT, SCCL 70 MT and Imports 268 MT.

Govt want to reduce import bill and enhance coal mining capacity. ( Renewable will take over in long run but we need more coal for next 10-20 years. Country is also going throgh massive infra building which needs steel, and steel needs coal for blast furnaces)

In 2019, our Parliament passed a bill that removed end-use restrictions for participating in coal mine auctions and open up the coal sector fully for commercial mining. So far 107 coal blocks have been successfully auctioned with peak rated capacity of 250 MT.

METHODS OF COAL MINING IN INDIA:

There are 2 methods of coal mining in india, Opencast (UC) coal mining (currently 96%) and Underground (UG) coal mining (currently 04%)

ADVANTAGES OF UG COAL MINING:

UG coal is superior in quality compared with OC and reduces the import burden for higher grades of coal. Further, UG mining is minimally invasive on land, detours land acquisition, avoiding its degradation, environmentally clean, and is society friendly. India has huge untapped potential for UG miming. Around 70% of the country’s coal reserves are amenable to UG mining, which delivers several advantages. So far, the primary

reason for slow-pedalling UG mining was loss-incurring production due to conservative and manual operations, which lead to low productivity.

However, now the technology upgradation to BLAST FREE TECHNOLOGY has opened up new avenues.

If we compare with global trends, UG mines accounted for more than 90% in China, about 37% in USA and 50% in South Africa. Europe has stopped open-cast mining and has relied mostly on underground production. Almost 50% of the world coal comes from UG mines.

SNIPPETS FROM COAL INDIA AR 2024:

Coal india plans to quadruple its production volume from ~26 MT to 100 MT over next 5 years. To achieve 100 MT, they aim to deploy 140 Continuous Miner (CM) equipment package with each package costing INR ~100 Cr including service. This opens up market size of 14000 crores for these underground mining equipments.

MAKE IN INDIA MISSION IN MINING:

Coal India has devised a strategic plan to phase out imports of heavy earth-moving machinery (HEMM) and underground mining equipment over the next 5 years.

Currently, Coal India imports high-capacity equipment, such as electric rope shovels, hydraulic shovels, dumpers, crawler dozers, drills, motor graders, and front-end loaders wheel dozers, valued at Rs 3,500 crore, incurring additional expenses of Rs 1,000 crore in customs duty.

CURRENT STATUS OF CONTINUOUS MINER PRODUCTION IN INDIA:

Currently Gainwell, a Panagarh based company under license from Catterpiller and JMS have been able to make continuous miners locally. Eimco Elecon has also been able to make the entire continuous miner package i.e continuous miner along with associated equipments like roof bolter, feeder breaker and shuttle cars. Thier continuous miner had some minor issues, which has been rectified now and the final approvals may take another 2-3 quarters.

FUTURE SCENARIO FOR EIMCO:

In the underground mining sector, the coming days will witness increase in demand for equipment catering to blast-free technology in underground coal mines and bigger size loaders and low profile dump trucks in the metal mines namely Zinc, Copper and Uranium.

Intermediate technology continues to be the backbone of UG with around 65 percent of the total UG Coal production being met by SDLs and

LHDs supplied by Eimco. Thier indigenously developed CM package sales are likely to start in FY 2025-26. Also the introduction of high capacity underground loaders for the metal mines will add to thier revenues. Thier bigger size LHD of 7 Tone and 10 Tone capacities have been established successfully. Recently, they have received and executed several orders for bigger size diesel loaders from UCIL and other leading mine contractors.

ORDER BOOK:

The present order book stands at 140 Cr, with a 4 to 6 month execution cycle. There are promising enquiry levels. A recent order valued at 33 Cr on 19th June has already been fulfilled.

CAPACITY:

The current plant capacity is 370 (3 production lines) loaders, having produced 200 last year. All the lines are interchangeable. No fixed production number can be allocated as they can also execute orders through job work.

INVESTMENTS IN METAL MINING:

Eimco intends to further expand its product offerings in the metal mining segment, including 15 and 30-ton machines. They are developing customized machines for MOIL.

EXPANSION PLANS:

The manufacturing plant is equipped with state-of-the-art machinery from Mazak. They are considering potential investments in technological upgrades.

EIMCO ENTRY INTO CONSTRUCTION EQUIPMENT INDUSTRY:

The Indian construction equipment industry, which

aspires to become the world’s second largest by 2030 is poised for remarkable expansion.

Eimco have now made significant inroads by manufacturing Piling rig under make in India initiative with the technical collaboration with CZM from USA. The performance is better when compared to rivals. They are adding further models to this range to meet market demands for some particular applications and increase the product portfolio.

FUTURE ESTIMATES OF FY 27 NUMBERS:

Realistic assumptions of 20% growth in base business and 25% market share in CM package is used while calculating future estimates. Base business EBIDTA margins are likely to sustain while CM package EBIDTA margins are likeky to be higher at 25%. Cost of CM psckage is considered as 50 crores while cost of maintenance is considered to be part of base business.

FY 27 EXPECTED OUTCOME:

Sales from base business: 390 crores

Sales from CM: 250 crores

Total sales: 640 crores

EBIDTA from base business: 78 crores

EBIDTA from CM: 63 crores

Total EBIDTA: 141 crores.

Current TTM EBIDTA is 48 crores.

A growth of 3x in EBIDTA is expected in next 2 years (FY 27).

For further study, sharing few links.

Disclosure: Invested with meaningful allocation.

6 Likes

I think some 50 crs order was cancelled from jms mines. So orderbook can be around 100 cr

That is not very relevant right now. Order inflow is likely to accelerate once final approvals for Continuous miner fructifies. It appears like Kavach opprtunity. Huge addressable market size with max 3-4 players

3 Likes

73e47c28-e52c-41fa-a2fb-30aeb6846201.pdf

There has been a termination of shareholders’ agreement between SANDVIK and Elecon. Does anyone have a view on this and long term impact on Eimco Elecon?

1 Like

Noted and approved the execution of Termination Agreement between

Sandvik Mining and Construction OY (formerly Tamrock OY) , Tamrock

Great Britain Holdings Limited (“Tamrock GBH”), BP Group (i.e. the

persons listed in Schedule - 1), Elecon Engineering Company Limited

(“Elecon Engineering”), Eimco Elecon (India) Limited (“the Company”),

and ·other Sandvik companies (i.e. the persons listed in Schedule - 2),

collectively called as “Parties”, to terminate the shareholders agreement

(i.e the agreement dated 28th February 1992 executed between SMC OY,

Elecon Engineering and the BP Group as amended by the supplemental

~greement dated 11th August 2011 executed by the Parties) which

governed their inter-se relationship and their rights & obligations as

shareholders/ promoters of the Company with respect to the operation

and management of the Company and all other agreements, arrangements and contracts existing between the Parties and other

matters in connection therewith. What would be the future implications??

1 Like

@niraj

Are you aware of any recent developments about the testing phase of CM package of Eimco Elecon. I talked to a Deputy Manager at ECL (subsidiary of CIL). He told that they plan to deploy 2 CM this year but both of them will be from Gainwell Commosales

2 Likes