Playing devil’s advocate :

-

Brand loyalty : I used to think the same but recently I joined the r/indiabikes, the biggest Indian bikes reddit sub. Opinions on RE are mixed at best, so brand factor may not be as strong as we thought.

-

New engines : No comments.

-

Exports : India is the biggest growth market. A lot of overseas markets ( such as US) are pretty stable, i.e no growth in motorcycle market. This means RE has to dislodge incumbents to gain lead. Not sure how well it can do that. And even if it does, the TAM( guessing) would be smaller compared to India.

-

Accessories : I doubt accessory business would do well if sales are not doing well, it’s called accessory for a reason after all.

Disc : Eicher is a small part of my portfolio, was looking to add more on corrections, but now I’m thinking maybe I should wait for the results. All said I agree with you guys that long term RE will likely out execute others.

2 Likes

I am quite a regular follower of motorcycle landscape and have been holding Eicher since 26/11/2020. This is before the launch of the J series 350 cc engine, the new 450 CC engine, and after the launch of the 650 parallel twin.

All 3 engines have upped the game. Since that time Eicher has launched following

- Meteor 350, Classic 350, Hunter 350, Bullet 350 on J series 350CC engine

- Scarm 411 on old himalyan 411cc engine

- Super Meteor 650 on 650 parallel twins, along with face-lifted continental and interceptor

- Himalyan 450

Each of the above has received very good reviews from with some improvement areas.

Upcoming bikes

- 350 CC Bobber,

- Shotgun 650,

- Scram 450

Besides this, they have invested in an EV bike Spanish company with a Board seat. https://starkfuture.com/en-us-IN

Overall it looks like the only company with a focused direction.

Invested and hugely biased because of Siddhartha Lal.

4 Likes

The new Himalayan 450 seems to have stellar reviews across the board. Is this category a meaningful volume generator for the company? Should Q4 see better volumes due to this launch?

RE super meteor 650 retails around 5 lakhs (on road). It sells around 1000 pieces per month. I don’t know how many other brands can convince these many people to spend such a huge sum (a sum at which you can get a decent car out and running on road) for a bike.Triumphs and harleys at around 8-10 lakh range barely sell 100 bikes per month. I strongly believe 650cc will take off in coming decade. In India next set of growth may come from migration of 350cc customers to 650cc or 450cc.Classic 650 which is right now in rumor stage will be a good inflection point for the change.

Also Latin american market and east asian market may be a good growth engine as they can give some respectable numbers.

Dominance in European and north American market helps in building a premiumness to the brand rather than bringing raw sales numbers.

One thing which baffles me why brand is not trying to enter China given it has huge appetite for premium products.

China is feature feature-conscious market or brand market. Raw specs are not great for Royal Enfield, nor is the brand pull in china.

1 Like

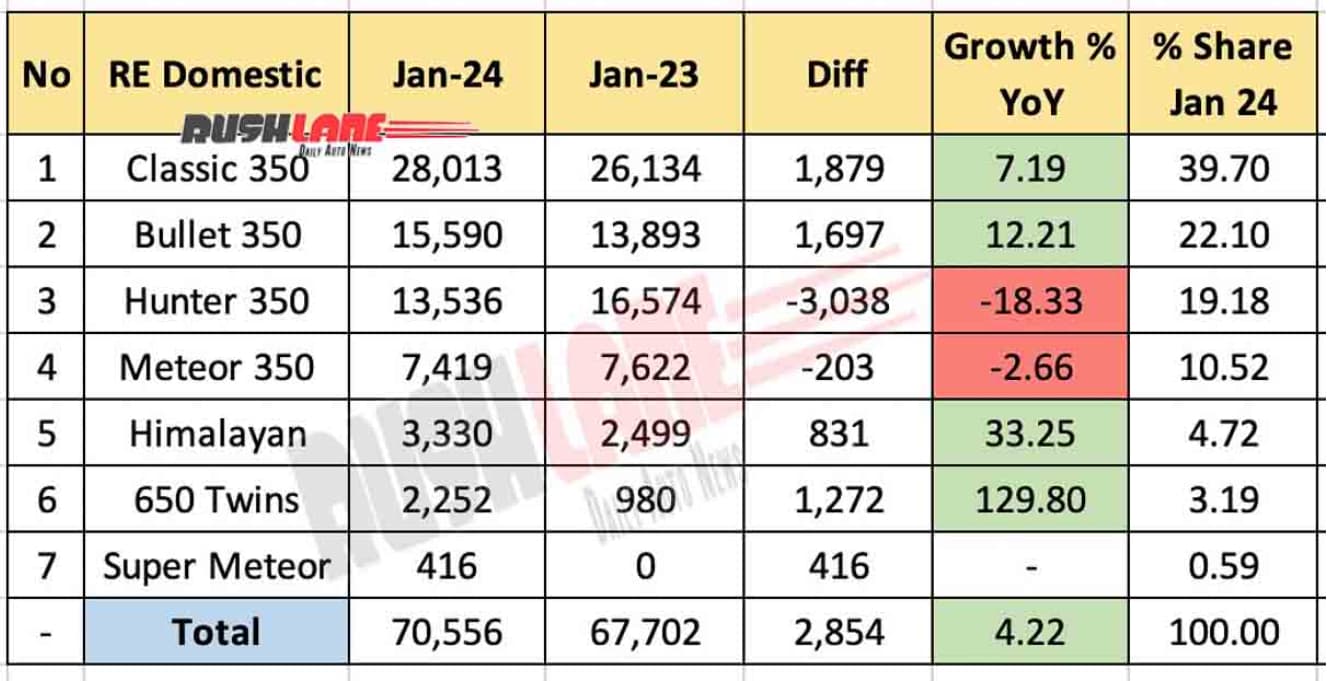

Good to see 650 cc segment growing .Its important to get good numbers in 650cc and 450cc because 350 segment now has cutthroat competition with all major manufacturers putting up a good show.

2 Likes

@laxman_sreekumar these numbers will vary month to month. I think RE intentionally keeps shifting between motorcycles and between export and domestic. For each motorcycle, they figure out what the ideal waiting period is. They don’t want to make it too long that customers lose patience nor do they want to make it too short to maintain the perception of demand supply gap. We should look at quarters or yearly numbers only.

2 Likes

please share the reserach report if available.