What option is this referring to?

Any views on the valuation of EWM:

I am assuming 250cr NTM Net Income @ 25x multiple gives 6250cr in Mcap for EWM.

2400cr stake of EFSL - which will be spunoff and listed seprately.

What option is this referring to?

Any views on the valuation of EWM:

I am assuming 250cr NTM Net Income @ 25x multiple gives 6250cr in Mcap for EWM.

2400cr stake of EFSL - which will be spunoff and listed seprately.

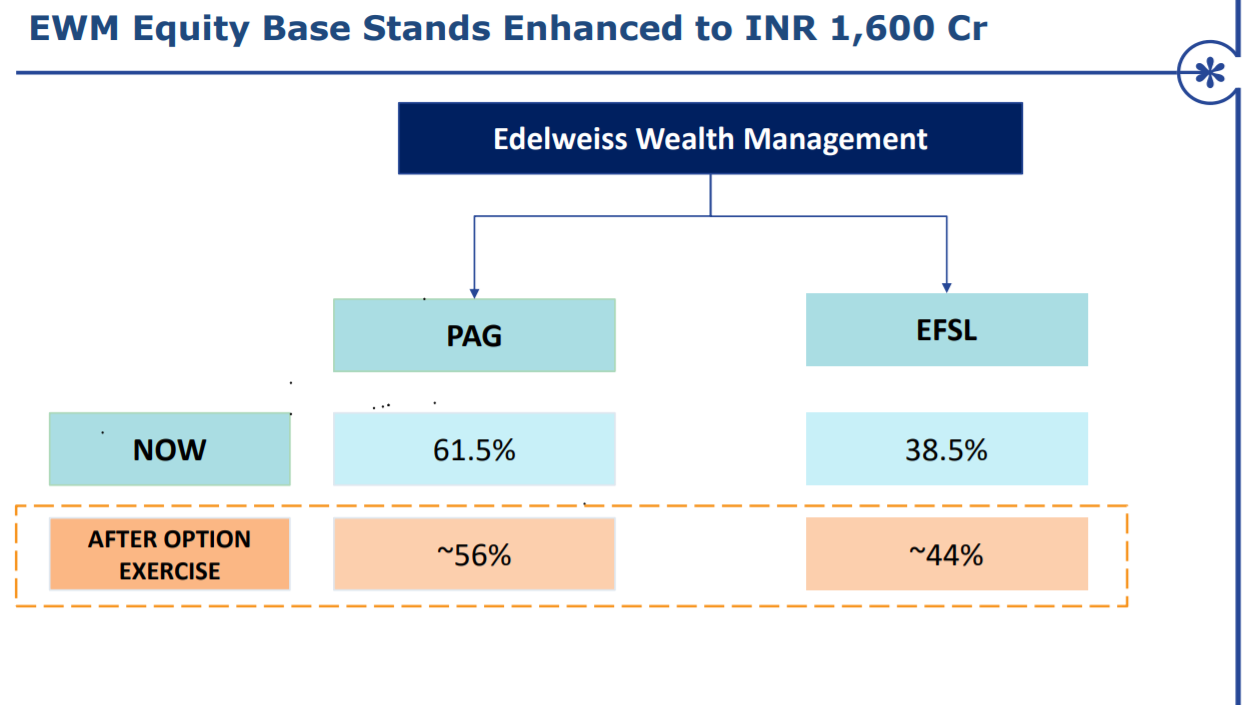

it is a call option that EFSL has to increase its shareholding from 38.5% to 44%… however i am not sure if the conditions for exercise, premium or strike price are in public domain…

I’ve recently invested at 65 levels due to following reasons

Mohnish Pabrai is invested in this,one filter I like to have is someone wiser is there in stock.

They have good amount of cash, looking at there market cap

and last is value unlocking with wealth management listing

also there MF buisness is one of the fastset growing in the industry

Worries I have though are :-

Management always say they have raised enough capital and go for capital raise the next quarter

also the corporate governance issues like Anugrah scam,the recent one with the ARC buisness.

Would love to know views, specially on negative sides

@Namanpathania Quite a good writeup. Thank you for sharing the views.

Also, 100% allocation on this stock reminds me of Munger’s Tenneco investment. I hope it works out for you. And for me too (just its 10% bet in my portfolio)

I have one question on the Margin of safety point.

Current price is 62rs, PAG deal gives 30rs

For the Remaining 32Rs book value So, do you mean to say even if it goes down by half i.e. to 16rs,

overall, we still have

30rs from pag deal + 16rs = 46rs per share

Is my understanding correct?

Also, the book you mentioned, is it this one?

https://www.amazon.co.uk/Reading-Between-Lines-Understanding-Inference/dp/0863889697

Dear Namanpathania,

few thoughts on what you said…

Diversification is protection against “UNKNOWN” and there are many unknown unknowns’ out there… some can completely wipe of our capital… I would urge you to reconsider your portfolio philosophy… I understand the contradiction - to create wealth you want concentration … diversification eat in to returns… but they key is balance… not easy but worth the effort…

few other points

Very interesting write up.

Can you share the Pabrai letter you referred to? Or DM it to me.

Thanks.

I was reading it on some site and i forget to download the letter and now it has been removed because Pabrai dont want people other than his investors reading his investment ideas.

But the information was really great as he explained his bet on fiat and other indian companies.

Admire your conviction and bravery. Seems like you are inspired by the Dhandho approach. While I do agree that the risk reward is very compelling and Edelweiss may deserve a reasonable allocation, I vehemently disagree with your approach of going all in on this one stock as I feel there are a lot of unknowns and uncontrollables which we the public just don;t know of, and which you yourself have alluded to. That said, I sincerely hope it works out for you.

Pity that the Pabrai letter is not available anymore. Would have loved to have a read. I am invested in Sunteck and Rain in large quantities, on both of which Pabrai’s views and thesis are widely available through his interviews. I haven’t found him speaking / writing too much about Edelweiss though, don’t think he’s spoken a lot about it publically. So apart from this letter, have you come across any other content on Pabrai’s theses on Edelweiss? If yes, please do share it for us to build the same level of conviction too.

worth a watch … ![]()

fully agree with your conviction, even i wanted to mention all this point but felt lazy so haven’t written anything. another thing i want to mention is there is going to have some news like lil bit scam in every company like commodity and arc scam in this, but point to notice is there is no promoter involed taking out money from the company. plus it is not the first time edelweiss facing this situation, i have read 2012 AR report it was almost same that time but they were able to overcome, so i think they will do that again. Why i think rashesh cant do any scam? because i have listened ton of his interview and realised he just to make money in long term. he is fan of ben graham and warren buffet, so he is creating wealth but it taking time. if rashesh shah had to scam, then he wouldnt waited that long.

Quick question for those focused on the financials.

Guys, all of Pabrai’s letters are available on reddit, just google it.

Basically he’s betting on their non-credit businesses and says that he is vary of their leverage activities and will be keeping a close eye on how the co. goes on to delever it. Also says leverage is dangerous and was the single biggest takeaway he got from Buffett during his lunch with him.

Btw, you’ll also notice that his returns have lagged a bit in recent years and one of his fund actually trails the benchmark by quite some percentage points.

I think the investors shouldn’t only look at mohnish stake, investor should have their own conviction. you can be happy that mohnish also has some stake in the company, so management quality and the balance sheet can be trusted nothing else. Mohnish and other investors enter and exit lots of stocks whenever they want. Sometimes they go wrong sometimes not.

some quarters back mohnish had stake in IEX, Repco finance, and many more companies but now he exited. so we investor should think on our own

Adding to this, rakesh jhunjhunwala also has some stake in it, but he isnt raising his stake. So in a way that also a red sign from my point of view. So, i think we should have our own conviction.

Why do you think investors are only looking at Mohnish’s stake and don’t have their own conviction?

If anything, the fact that a notable investor has conviction in one of your investments only adds further to your conviction. And like you said, it does give you confidence about the quality of management and governance practices which are difficult to gauge accurately for retail investors.

I feel at times many of us are guilty of over-intellectualizing the investment process, and we forget that the objective of investing at its core is not to be proven the smartest person in the world, but to make money.

So when a notable investor buys or sells something that we have an interest in as well, it is only sensible to take note of it and find out what his / her reasons may be for taking that action. This will help you either validate or disprove your own thesis. Remember, they have access to more information than us, and so there is no shame in following their actions closely.

No, I don’t think investors are only looking at Mohnish stake, but yet some comment only asking for Mohnish conviction put me off. It gives me signal that even myself can be under influence of confirmation which I really want to avoid.

Having said that, I feel it’s okay to have some confirmation but discussion should be around valuation and company quality not big investors stake.

I agree with you !! In a Mohnish Pabrai’s words I’m too a shameless cloner. I keep such stocks in watchlist.I enter at the price near they entered.I look at the downside more importantly. I use it as an additional filter to have a super investor or a guru like Mohnish.It builds more to my conviction and bet size.

Mohnish cute .6% stake in edelweiss.

Yes, he has cut some small stake in Kolte Patil and Sunteck as well. No change in Rain. Hasn’t spoken about it anywhere yet so not sure if its an allocation call or something fundamental. But the fact that he has cut some stake after recently raising stake substantially in the past two quarters is strange

All 3 cos have almost 100% exposure to India, one of the worst covid affected countries in the world. Rain derives majority of its revenue from its foreign subsidiaries especially USA, which will have an accelerated economic growth (thereby directly/indirectly helping Rain) due to rapid vaccinations and Biden’s $2trn infra boost. Seems like he’s underweight India now, which is quite understandable.

Doesn’t makes sense to me. Anywhere he mentioned this?