Looks like profitability in these two entities will take a lot of time

didnt they said they will cease the business of wholesale lending and will start lending them by through fund business. which they are already best are. I think BMC will do good as soon PAG deal happen.

Once they received funds from the wealth management @2500 cr, this shall resolve BMU profitability issue to the large extent IMO, as most of the losses resulting from BMU.

ECL finance has 8000 cr whole sale book, which they want to reduce it completely over the next couple of year (as they said in one of the ppt), so they will continue to provide for the whole sale book.

I came across this article on Moerus funds (Prominent fund manager from US- Amith Wadhwani) which took position in Edelweiss. Here is the rational he mentioned in this letter.

11 Likes

Yes. They wanted to reduce the whole sale book completely and move it to an AIF Fund.

Last year in Q4 they had taken some 2k cr haircut before moving it to AIF Fund.

In Q3 concall opening remark, Rashesh Shah said they are done with provisioning for wholesale book ,which was encouraging to hear, but I’m confused now why BMU unit would take so long to turn profitable again.

Disc - Holding

This is because they would receive PAG funds in 2 qtrs and reduce interest outgo on PAG/CDPQ debts which will be converted into equity. They plan to buyback costly bonds to reduce any signal of distress in the secondary market. This way they can convince the banks to reduce cost of funding further. These days banks also look at bond pricing in the fixed income market. wholesale book selldown is getting delayed and that is a matter of concern since bond yields have started rising again in USA. They need to work on this before liquidity starts receding. I would not be too negative since real estate market has stopped weakening and they could refinance at good rates.

5 Likes

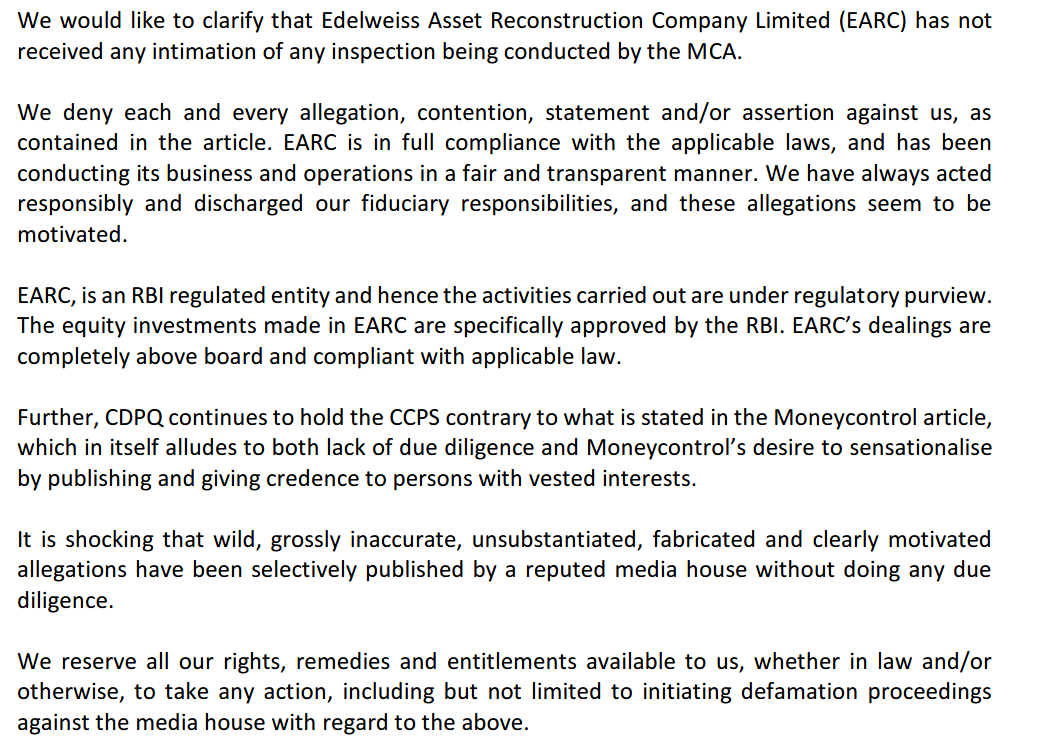

Whistleblower complaint by EARC’s partner to MCA… Seems like someone feels aggrieved…

Yes such a detailed accusation by a senior member sounds like trouble. No smoke without fire. I exited completely at 81 this morning.

1 Like

Agreed, but the complaint seems more of a case of the group allegedly granting favourable terms to a certain party and the other feeling aggrieved… Doesn’t seem to have much of an impact for the co. as a whole imo.

Disclosure: Invested, will see how this plays out and jump in/out depending on the outcome

samjh nhi aa rha, as far as i understand this doesnt sound like fraud case this sound like mismanagement. 1) allegation of allowing CDPQ to convert its CCPS to equity seems baseless, because as far as i know they didnt converted their CCPS yet.

The guy seems to be an influential one and acting agrived since there is no secondary market for his ARC equity holding. His antics might be to presssurise the management in settling a good exit price. Some of the biz decisions can not be questioned even if ARC paid 95% of the value to acquire wholesale loans from Edel NBFC. One allegation is factually wrong.

4 Likes

i know its risky now, yet i decided to hold the stock… will increase my stake if it goes below 45. it cant be sold below their value EFS business minus 1800cr (as alleged )

2 Likes

this article from bloomberg explain everything on the whistleblower allegation on edelweiss. Edelweiss ARC Lands In The Middle Of Whistleblower Allegations, Shareholder Tiff

what I come up with reading that Mr. Kuhad and Edelweiss promoter was having a spat since edelweiss didnt invited pratik kuhad for the right issue of ARC in 2016.

and another poing is RBI did recive the complaint of Mr. kuhad and decided to investigate EARC book, but they didnt find anything so they are not complled to disclose anything.

only point which could be issue is allowing CDPQ to convert its CCPS. and what i think is completely false…

My finding could be bias as i am heavily invested.

2 Likes

The article mentions that Kuhad raised a complaint to the Audit committee but those never showed up on the annual report. Isn’t this is an issue of transparency considering Kuhad is a major shareholder in the ARC ?

1 Like

Yes, I agree with that. They seem to be not transparent about it. But, I am not able to conclude anything with that, positive or negative.

As I don’t know the character of Mr. Pratik Kuhad, maybe his intention was to damage company image, thus he purposely just wanted to raise complaint. So it can damage annual report and the company audit decided to not mention his allegation, as they were completely baseless. I am making this assumption by keeping in mind that he wanted to raise his stake in the company, it shows the company balance sheet and work was/is healthy…

I fully agree, it shows my biasness. but I decided to go with this story. criticism invited.

And somewhere in moneycontrol article,according to Mr. Kuhad, the right value of EARC is 4k crs (20% for 800 crs) which CDPQ has got it @500 cr for 20% of EARC. Assuming he is right only this part (though I am waiting for more information on other points) you can buy whole Edelweiss financial companies @7.5k crs so all other businesses in 3.5k crs.

Disc. Invested.

He can be right on other points but not CDPQ one, as CDPQ hasn’t converted it CCPS yet. instead, they want ccps to convert their ccps so the interest amount wouldnt be drag in balance sheet. in short they havent converted its ccps. that is sure.

Let’s not discount the letter completely. One allegation which has got my interest is their inter subsidiary transfer of RE loan at 95% of book value. It is also true that they seek 50% discount from other sellers such as banks. You need to keep in mind that CDPQ won’t mind this since they also own upto 20% in their NBFC. Both Edel holding company and CDPQ will see this value neutral but for ARC’s minorities this will be oppressive. This arrangement may be called inappropriate at best but I don’t think this can be called illegal. This allegation will do two things - funds from banks will slow down again which started to pick up and most importantly hit ARC’s ability to ramp up AuM immediately. Valuation is not challenged but that is only due to lack of growth prospects in the near term

2 Likes

Strangely, they are looking to distribute some dividend from this money. Don’t understand this urgency for cash when your house was on fire not very long ago.

3 Likes