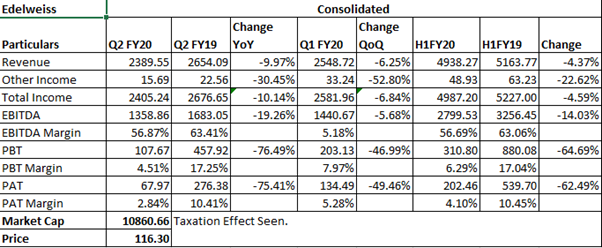

Q2 Fy20 Highlights:

Concall:

We have been degrowing the balance sheet. We have been shrinking a little bit. We also have – the cost of funding is still that transmission is not happening. So cost of funding still remains a bit elevated. But the good news is, there is enough funding available. But for us also, at this cost of funding, we don’t want to grow very easily. [Total] has been – we continue to provide a lot more conservatively on our credit cost because we do think that given the liquidity crunch that has been there, we should be more conservative in making sure we have more than enough provided. And the feedback we have got from long-term investors has been that it is always better to be conservative at this time and get some flowbacks in the future rather than try and optimize on credit cost at this time because the book is what it is. What we are finding is, as we’ve been saying again and again, the collateral cover is still healthy, but the cash flows of a lot of our customers on the wholesale side have become erratic especially on real estate because – and that is why we have launched our completion financing fund, which I’ll speak about in a little bit.

So very eventful quarters. The good news on this quarter has been – we continue to strengthen the balance sheet. Our customer assets continue to grow. So on that side, it’s a little bit of degrowth on the balance sheet side, but some growth on the customer asset side. As a result of all this, obviously, P&L has taken a hit. I think this is – and we’ve been saying it for the last, almost a few quarters that the P&L will remain challenging. We do believe until March 2020, our growth in P&L earnings is not on the horizon because as you clean up, as you strengthen, as you don’t grow very aggressively and we have not cut costs. We have not [made] of people because we do think that in the long term, this is a temporary blip in the cycle. And especially in key areas like technology, retail, creative, wealth management, asset management, we have made sure that not only are we not cutting back, we continue to invest because we don’t want to lose the momentum on that.

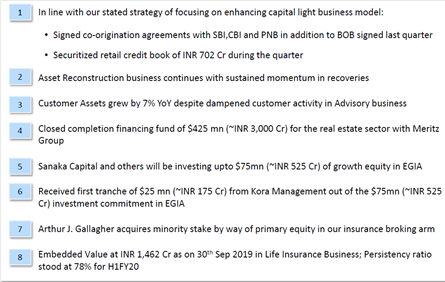

So as a result of that, you would have seen cost income ratios are also elevated. So this quarter, I think all of those have been the factors which have resulted in a lower P&L. But on the other side, the balance sheet in this quarter has got stronger. And as we recently – in the last quarter, we announced the capital raise from Kora, and we have said this was about $150 million target amount, $75 million will raise on Kora. We have announced the remaining $75 million with Sanaka Capital. And the good thing in this quarter has been, there has been a lot of investor interest in investing in this opportunity. Along with that, we also leased liquidity. Liquidity position remains strong. We have also announced the last mile real estate completion financing partnership along with Meritz, which we think, a, is very timely because that is a great opportunity because a lot of real estate projects are economically viable but have been suffering from last mile financing. And we’ve been saying that but we also have been one of the early ones to be able to raise capital on that and bring it to fruition. Along with that, this also gives us a liquidity window because some of our current loans could also get transferred to the AIF that we have set up. So it also releases liquidity as have been required for us. So I think on the balance sheet front, very happy. Things have got stronger though it has been hit on the P&L side. We also reduced our margin funding and the loan of against shares book because as the environment has been more volatile, our customers also, it isn’t their interests not to be very geared up at this point of time. And that is why you would have seen a little bit of degrowth on that side also.

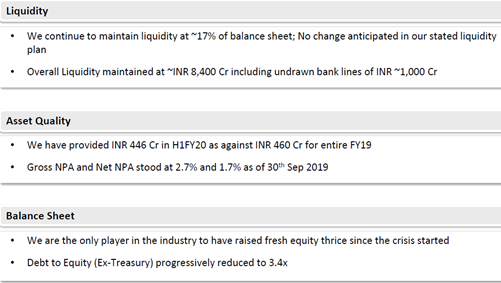

Our focus on liquidity wins. We continue to remain in 365-day horizon planning window for liquidity. Before the crisis started, we used to be 180-days horizon planning, and we have changed our gears for the last 4 quarters. So to go from 180 days to 365 days. Our feeling is, until March, we’ll remain in 365-day liquidity planning focus. The impact of that is that our, I think, liquidity holding costs will continue to remain elevated. Our focus on this will make sure – will ensure that we have enough liquidity, but we come with an earnings drag. So that will, I think, until March 2020, our current outlook is that we should remain in that mode.

So lastly, a couple of words on the environment. We do think August onwards, the environment has improved largely because of the equity infusion that government did in the banks, largely because of the interested cut cycle that RBI has been on for the last 5, 6 months. Partly because of the liquidity surplus that the system is somewhere now between 2 lakhs and 2.5 lakh crores of liquidity surplus, which eventually will trickle down and a little bit of the – create the cost of funding coming down is a result of that. I think liquidity has eased off. We are still a long way away from the normalcy, but it is starting to improve, August onwards. September and October have been good months, and we are seeing traction on that.

We are also seeing the foreign investors coming back. I think there is maybe a risk on – mentality is coming back, which is good for India because we need the foreigners to start investing again in equity markets, which is also coming back. So I think we’re seeing early green shoots on the horizon. This quarter is an important one, October, November, December. But I think India may have seen the worst in terms of GDP growth of 5% in Q1 and we’ll wait for the Q2 numbers. But most economists think it will also not be a very exciting number. But we do think Q3, Q4 onwards, GDP growth should also start inching back. The extreme slowdown we have seen will start to reverse and maybe '21 should be a normalcy year and '22 onwards will be a growth year for India. But I think from now to getting to normalcy which will be a big achievement because India has had one of the [serious-lest] slow down, one of the biggest dislocations in the financial markets we have seen in the last 4 quarters.

I think what we saw last year, FY '19, it should be like a base case because as you correctly said, FY '20, there have been 4, 5 datas on that. I think the data of credit cost. I think credit costs, both the nonrecognition of income as well as the provisioning and write-offs have been an extra INR 500 crores over normal in this year. And all other – the cost of liquidity, cost of borrowing, plus the lower level of activity is another 300-odd crore for this year. So we would say about INR 800 crores is what would call, at a pretax level, an exceptional fall, which can translate into EUR 500 crores, INR 600 crores of real fall. So I think the idea would be that once this normalcy happens, you should get back to that. And then our target has been about 20% growth. We see that possible in retail credit. I think our target in retail credit is actually 20% growth because we are really very small. So I think on that base, that growth is possible. Asset invent should grow at least 20% to 22%. Invent – sorry, in asset, as I explained earlier, a lot of our income and profit have not yet come in because we have not deployed INR 10,000 crores and we have not started getting the carry income, which we expect also coming in from 2021 onwards. So I think some profitability from that coming in. So I would say '21 should be a normal profitability year. And '22 onwards should be growth. I don’t think all of us think all NBFCs as well as financial services companies will grow to a 30%, 35% growth in a hurry. But I think getting back to 20%, 22% growth should be possible after '21.

Disc: Invested