E-waste recycling has been made mandatory by GOI last year, this is the trigger for demand, and e-waste is a very real problem that needs to be addressed.

Mgmt is talking about growing their revenues 3.5x next year and then doubling in the subsequent year. So you can do the math.

Plus EPR revenues will also come in a major way. they have not given a figure on the EPR fees, but even if you take Rs 30/kg fees. Its still a decent number.

Execution is something we as an investor we are betting on.

SO even if you ascribe a 25 P/E on FY25 earnings, which is very fair given the growth prospects. There is a lot of upside

Well the actual trigger has been the release of the new Producer norms for recycling. What that has done is forced big ticket Electronic and Electrical companies to make sure they procure back a percentage of all the items they sold and sell it to established recyclers in the organised sector. So far in the absence of these rules, Eco Recycling was not seeing much growth in business as they were competing against unorganised ‘kabbadiwalas’ - Now the corporates will deal only with compliance recyclers like Eco Recycing who will be assured of a large quantity of quality scrap which they in turn will sell. This is the big change leading to almost 300% increase in valuations in the past year alone. Whether this is justified time will tell - I don’t think the management has been the most ethical one in the past and there is not much of a management team, so all depends upon execution and transparency

If someone understands, how the EPR credits works, can you please explain?

The management mentioned in the Q3 FY24, that they missed 6 crores of top line due to CPCB portal not being ready and they also mentioned that they had roughly 600 MT, which gives 100 Rs/ KG for EPR. They also mentioned that 100 rupees can be divided into two parts, one is just EPR fees and other part is the missed quality material. Does that mean that EPR fees would vary so much depending on the material processed during recycling? Can someone please explain this part, if they understand it better?

In the Q2 FY24, Mr Soni had mentioned that they would be able to punch in all the numbers from April 2023 till date and in CPCB portal and would be able to generate EPR credits from April 2023. Is that understanding still correct?

In the three quarters of FY24, they had processed roughly 1800 MT, wherein Mr Soni mentions that company is recycling only mobiles, laptops and medical devices. In the Q4, he mentions that company would do 700 MT, which gives a figure of 2500 MT for FY24.

He is very confident of achieving 8000 MT for FY25 and 18000 MT for FY26. All these numbers, he is confident of processing only within the company. I believe for the company to process such high volumes, they would have to start processing large home goods, which would reduce the margins and also lower EPR fees as mentioned by Mr Soni (when asked why is not processing huge volumes) and it would also increase the transport costs, resulting in much lower EBITDA.

Only hope could be that high margins and high EPR of recycling mobiles, laptops and medical devices could act as a cushion for the comparatively lower margins and costs of recycling heavy goods

Disc: Invested and cautiously optimistic and nervous about valuations

This alliance between Eco Recycling and TERRA has the potential to make Eco Recycling realise their full potential and the capacity utilisation that we were waiting for.

EPR (Extended Producer Responsibility) service revenue will start from Q4 FY24.

Guidance: (Total capacity after expansion: 25200MT) Current year (FY24) capacity utilization- 4,000 MT. FY25 target- 12000MT. FY26 target- 25000MT. Minimum margin in the business: 40%.

Eco is maintaining around 60-70%.

you are looking at sales

but they have a margin for 60%+.

they are targetting 300 Cr of sales with 60% margins, which comes to 180 cr EBITDA

even on a 10x EV/EBITDA, which is very conservative

you are looking at 1800 Cr m-cap

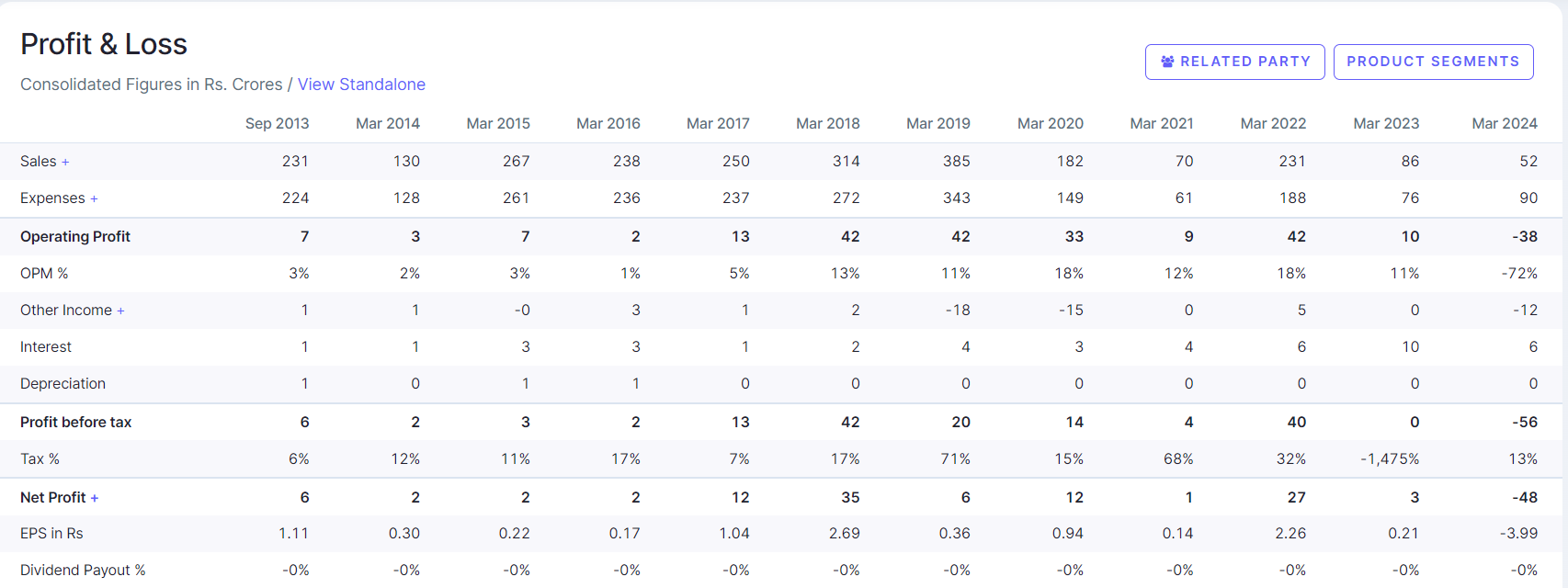

How can you use one metric to justify a stock? Take an example of this company has a price to sales of just 6.42 but then a PE of close to 80, it made 18Cr profit last year on a topline of 224Cr, 10Cr less than EcoReco which made 18Cr profit over a topline of 28Cr.

Just one metric doesn’t suffice, usually.

I think the company seems to be on the cusp of great growth but not sure if they can actually capitalise. They made some weird comments in the concall - when someone asked why the utilisation was so low, Mr Soni kept saying he is chasing margins and not volumes - that begs the question - why has he expanded capacity from 2,500 tons some time back to 40,000 tons if he is not chasing volumes. Also, the Other Income is a bit strange - they have generated 4 cr from investments in just one quarter - but their investments are not enough to generate this kind of return…Plus they have made an advance of 1.8 crores to a related party

See, the demand is there and they are in a very strong position to capture the demand, Look at their certifications and quality checks.

They are experienced as well,

Q4 numbers were underwhelming, but lets see how next quarter turns out.

Their investments were mostly equity investmetns which i think they are yet to divest fully.

● Established a new e-waste recycling facility with a capacity of 18,000 metric tons in Vasa, Maharashtra.

● Achieved recognition from the Prime Minister and a central government minister for its sustainable practices.

● Successfully conducted a collection drive for individual consumers, gathering over 10,940 kg of e-waste.

● Ecoreco is confident that its commitment to compliance and best practices will position it as a preferred partner for e-waste management.

● The company is exploring opportunities in emerging markets to serve multinational corporations.

● Ecoreco believes its focus on innovation and ethical practices will lead to significant growth in the future.

● The increasing generation of e-waste, along with government policies, is expected to drive long-term demand for its services.

● The existing plant’s capacity utilization is around 60%. The company expects to reach 75-80% utilization in the coming quarter and further increase utilization with the new facility.

● The decrease in other income is due to a combination of factors, including income from investments and fair value adjustments.

● Ecoreco currently produces black mass from lithium-ion batteries and is exploring partnerships for future chemical processing.

● The company expects to see a rise in EPR revenue as the EPR portal adoption grows.

● The portal was shut down for 15 days (from 19th March to 20th of April 24), impacting revenue collection.

● Recyclers didn’t fulfill their obligations faced delays in EPR fee collection (restart on 22nd appeal to 27th appeal). These delays explain the difference in EPR fees compared to previous quarters.

● There wasn’t a significant ramp-up in tonnage (quantity of materials recycled) in Q4 because the company prioritizes higher-margin items (electronic devices) over freezers and washing machines with lower profitability (around 10%).

● They believe focusing on high-margin items offers better returns even at lower volumes.

● The company focuses on securing deals with manufacturers who agree to their profitability requirements.

● The company will continue dealing in black mass. Technology acquired from CMax allows for future potential of metal recovery, but economics of supply and demand need to align first.

● Around 10% of the business involved data destruction/recycling in the previous quarter. The company expects this to remain between 10-12% in the current quarter.

● Investors are concerned about the recent decrease in profit margin despite high EBITA (earnings before interest, taxes, depreciation, and amortization). Management attributes this to a one-off event and a focus on high-value materials with potentially lower capacity utilization.

● Capacity Utilization suggests a range of Rs 30-40 per kg for profitability calculations.

● Future revenue and capacity utilization. Management maintains a hopeful outlook for achieving 100% capacity utilization by March 2026 and suggests a range of Rs 40-50 crore for future profitability.

● The 18,000-ton capacity addition is already set up and on track for 50% utilization by March 2025 and close to 100% by March 2026.

● Management doesn’t see collection centers as an efficient way to acquire high-value materials like phones and laptops. They believe direct courier partnerships are more effective.

● Difficulty in modeling future revenue due to the focus on high-value materials with potentially lower capacity utilization.

● Emphasizes the importance of high-value materials for long-term profitability. Provides a range for future profitability calculations (Rs 30-40 per kg).

My point in this post was to evaluate Ecoreco’s right to win here?

It doesn’t matter what Cerebra is today, but rather bringing into consideration, that someone with 13x more capacity and important technical qualification is already present.

It is also noteworthy to look at Cerebra’s journey to understand the nuances in this field.

FY19 Cerebra did a turnover of 385cr, Eco reco was at 12. The following collapse is another case study.

I did not get, whats the importance of a team here, also Eco reco is largely a 1 man show lead by Mr. Soni.

I am not sure, whats the trap her? pls enlighten.

Disclosure: I have a token exposure in Eco Recycling. Have sold some shares in last 30 days.

My intension was to check for cerebra performance over decade. When sector is heating up but cerebra is going against odds. Neither I am invested in Eco Recro nor in Cerebra.

Eco recro already rallied too much and even they didn’t utilized existing capacity but expanded for 18000 ton capacity. Not sure how will they utilize this.

Woundering no big competetors are in E waste recycle space. There are many I found for other waste managment except e-waste management.

Don’t think Cerebra and Eco are comparable just bec they are in the same industry. Management quality makes a big diff. Cerebra has so many red flags including in their Audit Reports that it is more or less a fraudulent sort of operation. While Eco’s governance standards are no where near top quality, they are far better than Cerebra. Eco has last year received a govt grant for 6cr as also mention by PM in his radio address - this puts additional pressure on Eco management to make sure they don’t do anything unethical as there will be repercussions…