Co. plans to manufacture covid related medical equipments ![]()

https://www.bseindia.com/xml-data/corpfiling/AttachLive/4cf14285-8fc8-433e-9f5d-a68234c3013a.pdf

recording of Investors call

2 Likes

Stalwarts Mr Kela and Singhania have bought this company. What is cooking??

Company has 3 business segments

Aerospace :

Mfg high precision airframe and aerostructures for Airbus, Beoing, Bell, HAL.

Tier-1 supplier of flap track beams to Airbus A-330 and sole supplier to A-320 (supplies to spirit aero system)

35% consolidated revenue but 70% to overall EBIDTA. Margins ranges from 25-31%.

Consistently grown the business from ~140cr in 2012 to ~500cr in FY20 (first time de-growth in FY21 due to order delay)

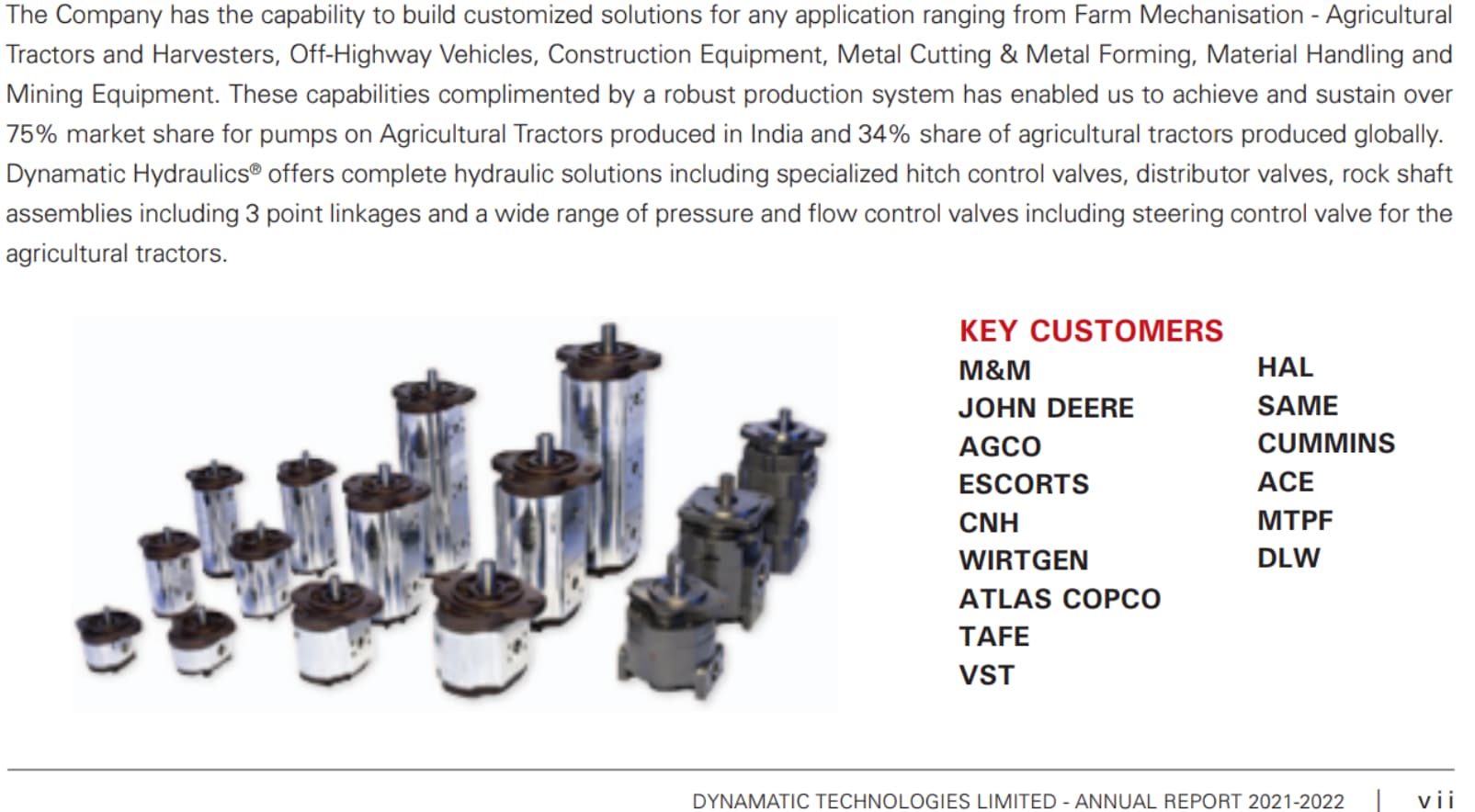

Hydraulics growth:

Supplies hydrulic gear pumps to tractors, construction equipments.

70% market share in indian tractor business but wallet share is less.

India and UK business. Indian business margins is around 13-16% where as UK business margins around 6-9%. Together, hydrualics margins hovers around 10-12%.

~300cr top line. 26% revenue contribution and 19% EBIDTA contribution.

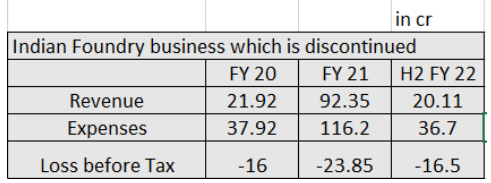

Foundry &Indian foundry:

mfg complex metallurgical products for automotive engines and turo chargers to leading global OEMs. Though company claims high precision work for leading OEMs like BMW, Audi etc.

Germany foundry business and Indian Automotive business → germany foundry margins are only around 4-6% whereas indian foundry is loss making. Last year company divested indian foundry for ~75cr

40% of revenue and less than 10% EBIDTA contribution.

High margin aerospace business and medium margin hydraulic business is completely masked by low margin (rather loss making) automotive/foundry business. Consolidated operating margins are in the range of 10-14% depending on business mix.

On an average company is generating an EBIDTA of 140-160cr. But half of it is going to banks in the form of interest cost.

Now lets look at the growth triggers for company:

Aerospace:

Sole supplier of Flap track beams for A-320, A-330. Civilian aircraft business impacted badly last year as lot many orders postponed. However now Airbus is sitting on record order book. Key investments made in UK facility (robotic line) which started operational in Nov-21 (delayed by >12 months).

Redesigned the flap tract assembly for airbus which will give cost benefits.

Two new projects from Boeing (F-15x model aircraft, T-7 Red hawk) apart from existing two (CH-47 chinook, P-8 models)

Incremental order flow from HAL. HAL is acting as system integrator and out sourcing more business to private players (L&T and Dynamatic are prominent) for all its Tejas and Sukhoi orders; 41k cr order book)

Hydraulics growth:

Higher wallet share going forward; power steering for tractor (which can double revenue/pump). few new complementary products developed which are in customer approvals.

New integrated hydraulic product by UK team for construction/farm machine (cost is 1.3L), expecting 5000 units of peak sales per year

Management is guiding for 3-4 times growth in hydraulic division in next few years and 18-20% margins (highly optimistic figures, have to track)

Non core divestment:

Sold JKM foundry for almost 65-70cr. Selling land at Coimbattor which can fetch 45-50cr.

Losses in indian foundry (JKM) business averted. Accumulated losses can be offset for future profits which can result in tax rate reduction. Working capital reduction

Converting german foundry for aerospace components/castings:

Waiting for certification (can be expected shortly)

high demand for aerospace casting and metallurgy services ( but can take time, thinking is in right direction).

Debt & Interest cost reduction:

~320 cr long term debt debt + 6 million euro, Some other part of debt in balance sheet is lease liabilities which is not actual debt.

Out of 320, around 191 cr debt is converted to foreign currency debt which can reduce the interest cost (10% to 5%). Rest, some part of debt will be repaid by divestment money from land sale.

10cr rent saving by moving from Peenya industrial estate to devanahalli (own building) and subsequent reduction in lease liability.

In nutshell management is taking few steps which seems to be in right direction,

- there will be a improvement in balance sheet (debt reduction & interest cost saving),

- divesting of non core (land selling) & loss making business (Indian foundry business),

- repurposing automotive German foundry business to aerospace components manufacturer augurs well for the company.

- And finally good visibility on core business growth i.e. aerospace and hydraulics.

Now it all depends on management ability to execute…will have to see if they walk the talk.

9 Likes

Very well summarized Sreenadh. Thanks

The company is a turnaround candidate and if the management really walks the talk (as you said) this company has huge upside - The order for the front fuselage for Tejas from HAL itself would be huge and give proper visibility of earnings for the next 3-5 years. I think the management has taken the right steps in terms of hiving off non-core assets and focused on debt reduction and interest savings - We will start to see the impact of these measures in the next Q3 numbers itself

1 Like

While there are Defence orders being allotted to multiple companies like BEL, HAL, Zen Tech. etc., why not even a single order is flowing to this company?

In last con call, management said that good news are on the way and we need to have patience but now this is really testing the pattience big time.

Also, no news of the land being sold for debt reduction or any other order inflows from MNC cos. like Boeing or Airbus considering that many contries like germany are now doing big deals with other cos. like Lokheed who have further already allocated orders downstream to cos. like Avantel.

Discl. - Invested

Dynametic Technology

Profits are already past peak profits- price is yet to catch up.

What is changing -

-

Aero and defense transition (reducing share of low margin auto biz) ,

-

Balance sheet deleverage(via land sale and subsidiaries exit/restructure)

-

Strong hands entering - Abacuss, HDFC(been there)

-

Major wins with global aerospace opening up

-

Global subsidiaries restructuring -

-

Key capabilities - for a small cap their clientele is very impressive with all whos who of Aero, Defense, Tractors. Pricing power is quite visible(standalone entity margins have been 20%+). Critical components and sole supplier in many parts. Supplier approval and registration is a lengthy process for these global biggies, and not easy to replace - esp if one is design to delivery and has backward integration.

Engineering play with critical component as sole supplier to marquee global names(Major tractor OEMs with 34% global market share in Hydraulics, aero & defense -Boeing, Airbus, Bell helicopter, HAL, BEL etc). Recently won a multiyear contract with spirit - Belgium. Have been a supplier of Tejas-LCA etc and working on number of projects in defense sector(AR has more details).

- Here is the conversation between mgmt and Abacuss - Sunil Singhania.

- AR 22 is a good read - some snippets

The Dynamatic-Oldland Aerospace® (DOA) Research & Development is engaged state-of-the-art 3D designs using software such as CATIA V5 and Unigraphics NX, Mastercam for their design and development activities meeting to global OEM standards. The Company has been successful in bringing value addition in reducing cycle time, concession reduction, technology absorption and indigenisation of technological products and developing special manufacturing processes. Indigenisation of Foldable Strut for HAL ALH DHRUV Helicopter developed a foldable strut mechanism for opening and closing of the helicopter door during rugged environmental conditions and is single source supplier for this product to HAL . The sub-assembly has been developed with various specialized aerospace alloys and is manufactured and tested in accordance to the aerospace standards to meet CEMILAC approval for series production. DOA team has also received a patent for the development of the foldable strut. Development of complex machined beams and frames for Bharat Electronics Limited: Designed and developed a high precision solution for complex machined beams and test rig for high pressure leak and pressure testing. This engagement is a key milestone for DOA towards ‘make in India’ and indigenisation efforts undertaken by Indian Companies.

Potential for some rerating and growth based upside exists, mgmt. intent is visible, execution stays key - steps in right direction so far. Standalone margins are 20%+ and with deleverage bottom line can significantly move up.

Risks to watch for - Shifting focus areas, subsidiaries restructuring & deleveraging - not a small step and takes its own time.

Initial positions & studying

2 Likes

The promoter appeared very confident.

Company has secured a $70 million contract with Airbus to manufacture aircraft components. According to management this is just the beginning.

Over the last decade, they’ve built a world-class aerospace business.

They’re tier-one manufacturer for Bell Helicopter, Airbus, and Boeing, winning the Supplier of the Year award from Boeing this year, and from Airbus two years ago. They have consistently been the best supplier for Bell.

The new contract with Airbus involves producing smaller, detailed parts. They are the sole global supplier to Airbus for the parts they provide.

Over the next 18 months, we can expect to see operating leverage in play, as they already have the human and manufacturing capacity in place to execute large orders when they come.

Disclosure: Not invested

Feel free to correct me if there are any mistakes.

1 Like

Why are the Npm’s so bad here. Completely dependent on other income. And why is inventory and Receivables so high. Combined almost 50% of Annual Revenues are stuck here. Have never checked this company before so any ideas on these.

Recent presentation video. Looks good.

1 Like

HDFC reduced stake from 7.5% to 5.49%.

Dynamatic Technologies Ltd. has developed the Cheel VTOL drone powered by the Orbital 150cc Heavy Fuel Engine. The engine supports multiple fuels, delivers 11.5 hp, and ensures efficiency with a fuel consumption of under 330 g/kWh. The drone offers an impressive endurance of 8 hours, making it ideal for tactical and military operations in varied conditions.

4 Likes