One thing I noticed is that Duke hasn’t given a notice to BSE about results date before declaring results in the past as there has been no such data in corporate announcement section. Is it normal or should we ask the management to give a notice to BSE for results declaration date.

Adding to it had a talk with CS on two instances( October last week and November first week), both weeks was told that results were due next week.

Duke has mostly declared results on time in the past. This time it seems to be delaying. Don’t know what’s taking them so long

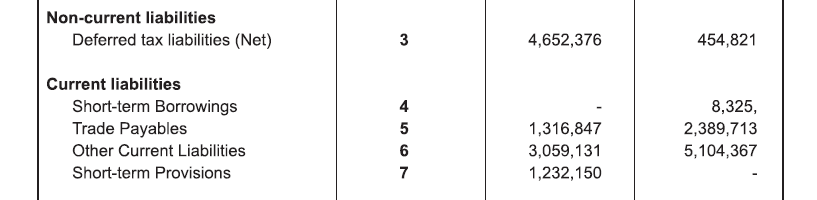

The results should be compared Y-o-Y as it is a seasonal business (mentioned in result footnotes also). Though Y-o-Y the loss has widened due to lower sales. Employee costs have gone up (This I feel should be compared Q-o-Q); Depreciation cost has gone down.

The major kick in sales should come once they acquire another OPV for which the CFO has already said that they are in advanced talks and we can expect a notification on the same very soon.

Disc: Invested. Looking to add more at dips of 15-20%

Had a talk with the management about poor results. These were the answers:

Last year q2 they had few contracts from South, this time they didn have any contracts from the south because of monsoon.

In q2 for both last year and this year they didn’t get contracts from the western part of the country . This is a general trend as monsoons are strong.

Management sounded pretty positive about the next two quarters and future growth.

New contracts have already started from the month of October.

OPV deal is still in process and should be done by December.

Just wanted to check if you have an opinion about Aban Offshore. I don’t follow this industry but was just looking at long term charts for some contrarian bets. Aban is testing multi-year lows and valuation wise it seems to be quite attractive.

Had some views (not necessarily on Aban), so just sharing.

I personally have a limit of 20% to allocate to value buys and turnarounds.

Few things at the top of my mind that I look for in a turnaround or value buys (not in any particular order and not all the below features one maybe able to find in a single company).

Things can’t get worst for the company from here on (busines performance wise and technically too most of the selling done and the stock has bottomed out).

Valuations are very cheap and downsides minimal/limited.

If one can arrive at a conclusion that if market goes down then this stock will outperform, then all the more better.

A new jockey at the helm of affairs who comes in with a good reputation and credibility.

A stated and visible change in the underlying business structure to remedy the problems of the past.

Favorable business scenario for the company in future (things can only get better and one can map that to a personally suitable timeframe).

Cash flow situation looks like improving in future.

Positive policy initiatives from the government for the sector.

De-leveraging balance sheet possible and visible in future.

Company holding out and performing decently in a bad business environment for the sector.

Visible initiatives to bring in operational efficiencies and to keep operational costs and other expenses down.

Would the expected returns cover the opportunity cost lost and in fact give decently more returns than the opportunity cost, for the specified duration that one intends to hold.

There will be more criterias as well. Had these at the top of my mind.

Answering these questions may help you in taking a call with respect to Aban.

@hrfacebuk - that’s a nice list. I had some of those (not all) in mind when I started looking for some down and out sectors/stocks. Coincidentally, there was some news about this sector yesterday -

I am not sure about monsoon story. Monsoon was week this year. So, why this affected more this year. As soon as qtr ended, they got the job in Oct!

How, do you feel about 6 cr reserve? Is that enough for new vessal! How much debt it need to take if not?

I am convinced about the reasons given by the management for the poor results.

They might have started the contracts in September end.

Depends upon the kind of vessel the company buys shoukd cost between 4-6crs.

Management doesn’t like to carry debt on books and both the CFO and CS reiterated that the company is looking to raise QIP once the company gets good valuation.

“Duke has secured a contract to provide 10 high speed boats and been appointed as official vendor for same by ministry of defence for Indian Navy’s International Feet Review,” the company says in its filing to exchange."

A huge achievement I feel.

More good news should follow soon I feel. As per Management all the things are on track

Today’s announcement on closer scrutiny has left me somewhat concerned. What is the contract worth in terms of revenues to the Co.? Why has the mgt. chosen to be silent about it ? What is the duration of this International Fleet review ? Is it 15 days or 6 months ?

A bigger concern is that these 10 high speed boats seem to be the same ones that were earlier leased to the Navy to petrol around the harbour. Are these now lying idle or has that contract with the Navy been renewed? I fear it’s the former.

For me the crucial event will be the acquisition of the second OPV. At the AGM, the mgt had indicated that it should happen around December / January. Hopefully, it will happen on schedule n the Co. could continue with its onward journey, though the Co. chose to be silent about it in today’s announcement. Keeping my fingers crossed!

I’m not sure how the FIC fleet allocation is handled. If the existing ones are used to patrol Mumbai harbor, then they cannot be allocated to IFR because the event is in Vishakapatnam, in which case it is likely these additional craft may be obtained on a lease. What I’m unsure about is whether the contract or tender is for 5 days only or more than 5. I suspect it is the latter.

Costs for the entire event have not been divulged to the press; this is from ET. But it is by no means a low-cost event with the State government allocating 74 crores. 70-90 ships are expected at this event, so costs for security are not expected to be low. I pulled up tender values for hire rates of FICs, and going by this tender, the rate is around 165k per day for 7 craft. Of course, that is a ballpark figure for estimating the contract value for IFR.

I believe I found the tender awarded to the company. I’ll admit I got the info about the type of boat wrong - the tender is not for FICs. I didn’t see any tenders for FIC issued by the DEO. Instead it is for fast passenger boats, so the question of FICs remaining idle probably does not arise. The tender mentions the minimum number as 10 boats, and similar tenders have differing quantities, so this is the most likely one.

The tender award amount is not mentioned. I’ll make an educated guess based on the Earnest Money Deposit of 5.5 lakhs, because there are guidelines for the tender issuer to determine the EMD. It is around 2 to 5 percent of the estimated value (going by either Defence Procurement Manual or Ministry of Finance manual for procurement of goods), which gives me a bound of 1.10-2.75 crores as revenue. This is quite substantial IMHO, given it’s effect on EPS, even if it is a one-time event.