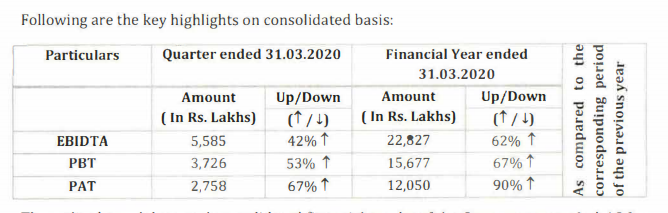

Good result declared by Dixon.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/5e92dadc-d473-466a-ba9b-f962436b3f50.pdf

Good result declared by Dixon.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/5e92dadc-d473-466a-ba9b-f962436b3f50.pdf

Talking Point With Dixon Technologies’ Atul Lall:

Old but very good interview

Cost effect on Dixon

Hi folks,

Was doing a deep-dive on the 2 contract manufacturing firms -

Sales growth

| Name | Mar Cap Rs.Cr. | Sales growth 5Yrs % | Sales growth % |

|---|---|---|---|

| Dixon Technologies | 5787 | 22 | 47 |

| Amber Enterprises | 4667 | 23 | 44 |

Working capital management

a. Amber:

i. Had reported negative CFO in FY 19 at -63 cr.

ii. But with good cash flow management in FY 20, has managed working capital needs well and operating cash flow has turned positive in this FY to 243 cr.

b. Dixon : Free cash flow generated in FY 20 : Rs 91 lakh

Likely headwinds in demand of some products

a. Q1 is traditionally a strong quarter for the company (given higher sales of ACs during summer). Demand likely to be impacted owing to the lockdown.

b. Whether the pent up demand will get addressed in the coming months & how does customer purchase behaviour w.r.t purchase of durables pans out – remains to be seen

Employee cost as a % of sales

a. Amber enjoys a higher operating margin vis-à-vis Dixon

Amber Mar-14 Mar-15 Mar-16 Mar-17 Mar-18 Mar-19 TTM

Sales + 973 1,230 1,089 1,652 2,118 2,718 3,963

Expenses + 898 1,128 975 1,521 1,934 2,504 3,654

Operating Profit 75 103 114 131 184 213 309

OPM % 8% 8% 10% 8% 9% 8% 8%

Dixon Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 Mar-18 Mar-19 TTM

Sales + 767 1,094 1,201 1,389 2,457 2,842 2,984 4,400

Expenses + 746 1,067 1,169 1,331 2,365 2,729 2,848 4,177

Operating Profit 21 26 32 59 92 113 136 223

OPM % 3% 2% 3% 4% 4% 4% 5% 5%

b. Employee cost as a % of sales

However, a further deep dive into the expenses and we see the employee cost as a % of sales for Amber is (1.8% - 2.1%) was lower than that of Dixon (2.9%) in FY 18 and FY 19. It evens out in FY 20 though

| Amber | Mar-16 | Mar-17 | Mar-18 | Mar-19 | Mar-20 |

|---|---|---|---|---|---|

| Employee cost % of sales | 2.7% | 2.8% | 1.9% | 2.1% | 2.6% |

| Dixon Tech | Mar-16 | Mar-17 | Mar-18 | Mar-19 | Mar-20 |

|---|---|---|---|---|---|

| Employee cost % of sales | 3.8% | 2.9% | 2.9% | 2.9% | 2.7% |

c. No. of employees

| No. of employees | Amber | Dixon |

|---|---|---|

| Permanent | 1003 | 894 |

| Contractual | 1797 | 5713 |

| Debtor days | FY 19 | FY 20 |

|---|---|---|

| Amber | 106 | 75 |

| Dixon | 63 | 40 |

| Amber | Dixon | |

|---|---|---|

| All employees | 17% | 10% |

| For employees (other than KMP) | 13% | 15% |

| KMP | Approx ~ 20% |

b. Though the remuneration to KMP is within the ceiling as per the Act.

7. Auditor’s fees

a. Amber enterprises have a reputed audit firm. There has been a steep hike in auditor’s fees though, from Rs 24 Lakh to Rs 40 lakh in FY 19

8. Goodwill as a % of Net worth

| FY 19 | FY20 | |

|---|---|---|

| Goodwill as a % of net worth | 7% | 11% |

Amber has reported a goodwill of 122 cr in FY 20 ; up from 67 cr in FY 19.

Acquisitions in FY 19

Sidwal Refrigeration - AC & refrigeration for defence, metro, etc – revenue contribution of 176 cr in 9M FY 20

Ever Electronics (Pune based co - PCB designing services) – revenue contribution of 214 cr in 9M FY 20

To quote another case, Symphony which acquired Climate Technologies - Australia’s leading

manufacturer of cooling and heating appliances – Has reported a goodwill arising out of it at 130 cr in FY 19

Views welcome from friends …

This is just a collation of figures from the Annual report + investor ppt. It is not a buy or sell recommendation for any stocks.

Disclaimer: Not holding any of these stocks. Only tracking

A very nice management interview with Nirmal Bang. They are guiding 20-25% growth over the next few years.

")

Thanks for the link! he is also saying that FY21 will be flat vs FY20 but mr market has already rewarded it significantly for its prospects.

Washout qtr for Dixon. Result down on every parameter.

Disc - Invested

Hi bimalb,

I couldn’t find the cash flow statement for this qtr…

Can you help if available with you?

Cash flow statement and Balance sheet are published with half year and full year earning. Hence in this case you will have to wait for the September quarter result.

Dixon appears to be very interestingly placed at the center of several mega trends and strategic priorities for the government: Make in India, Aatmanirbhar Bharat, global supply chain diversification and China de-risking, and growth of contract manufacturing + private label brands. The recently announced PLI scheme is very smart and can be a game changer for Make in India.

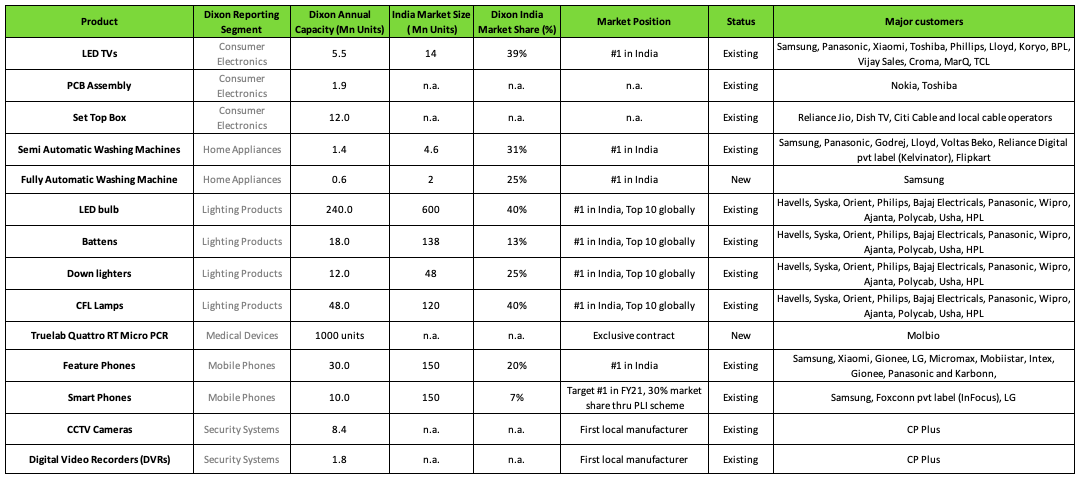

Below is the latest product portfolio, capacity, key client list and market position of Dixon sourced from various broker reports and company filings. What’s clear from studying Dixon is that they have been able to continually enter new product categories with their existing clients, aggressively ramp up capacity with minimal capex and attain market leadership while maintaining a well diversified pool of clients.

Disc. Invested

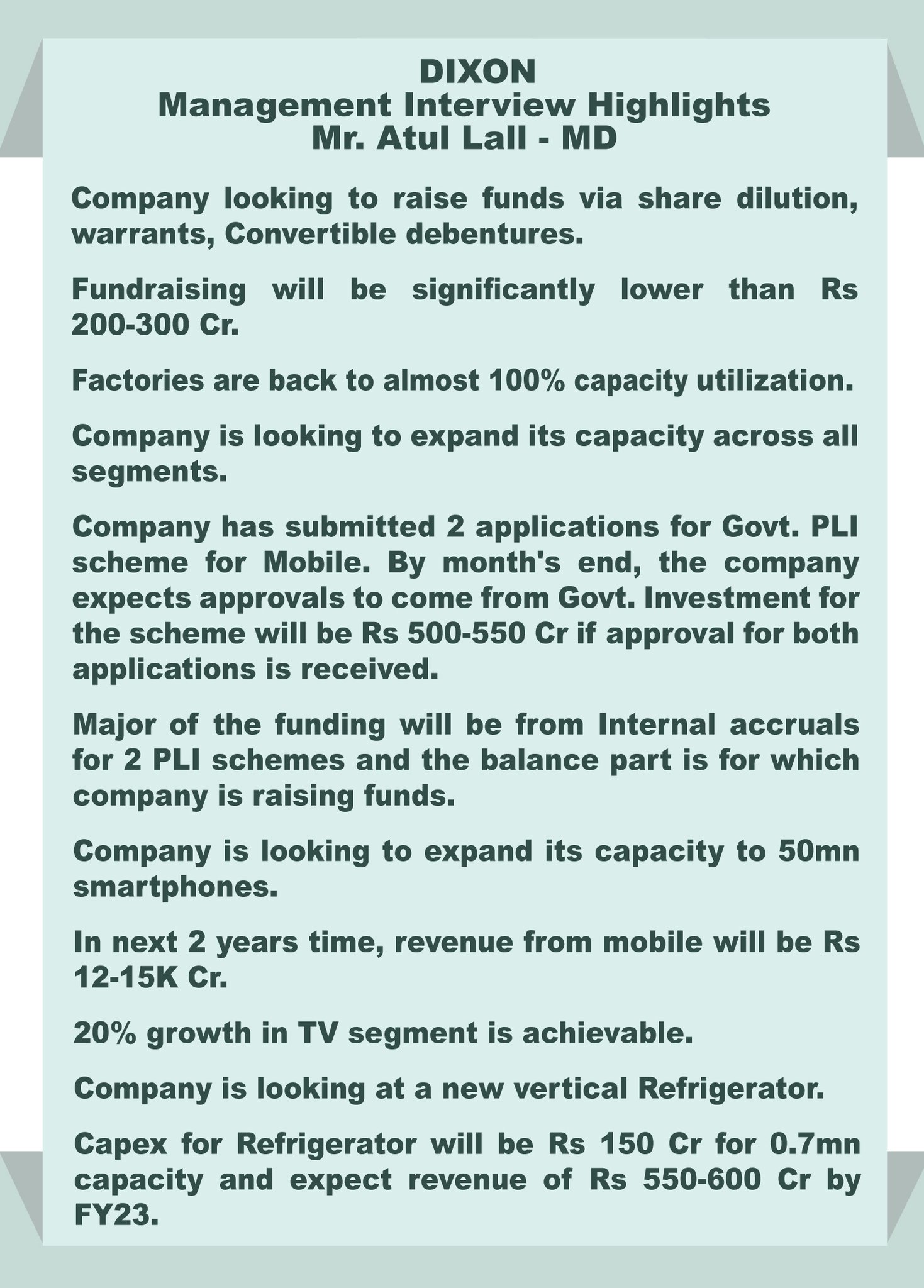

Dixon raising a small amount of equity for PLI linked capex. Interesting interview with Atul Lall - he is guiding for 12,000 - 15,000 cr revenue from mobile segment only in next 2 years on the back of i) expanded capacities and ii) new large customers for exports and domestic market. Mobile segment revenue was 536 cr in FY 20 and Dixon’s total revenue was 4,400 cr.

Edit: Summary of the interview from @ analystmohalla on Twitter

Disc. Invested

This is huge. And they had earlier mentioned that mobile segements EBIDTA will be higher considering PLI incentive. So, EBIDTA margins can be 8-10% or higher.

This can easily translate to EBIDTA of 1000-1500cr.

Refrigerator will be the new vertical. Considering the market share they have captured in other verticals, it will be reasonable to expect that they will grow big in refrigerators too

One should not consider new margins to be old margins + PLI incentive. They will most likely pass on a good part of that incentive.

In Q1FY21 concall, management has stated that they expect margins under the PLI scheme would be higher, but not substantially higher.

I understand that some value of PLI scheme will be pass through. However som benefits will accrue.

Currently mobile EBIDTA margins are in the range of 4%.

With PLI scheme, there will be two factors:

But yes, 10% is a little far fetched. But it should graduate towards 7-8% slowly

Dixon is a contract manufacturer like Foxconn. This traditionally means very low margin business (Which is why Foxconn and others have tried to launch their own brands). Their bargaining power is limited with manufacturers and they don’t hold any of the IP. It is a pure play cost game

Agreed. There is going to be manufacturing shift from China. India is encouraging manufacturing in India. PLI is coming up.

This is a business with 3-5% operating margin that Dixon has. The P/E has already doubled from the beginning of the year. Seems like the stock is almost more than fully priced all the positives

Risks are huge

For a company with no IP creation and low OPM%, I would be wary of buying at these prices.

Today Dixon has announced its Wholly Owned Subsidiary –Padget Electronics, received

approval under PLI scheme of Government of India

Padget Electronics is one of the 16 Companies (Domestic & International) which has

been granted approval under PLI scheme of Government of India for manufacturing of mobile phones (Domestic Companies);