By change, I was referring to replacing Drreddy with Bajaj Finance in my portfolio. I don’t try to guess policy moves, but believe that a portfolio of quality business is antifragile. Corporate tax cut was a completely lucky break for me, if I would have guessed it earlier, I would have replace Drreddy with Bajaj Finance earlier, when it was cheaper price wise, and not now at a higher price point.

2 Likes

What are your thoughts on Kotak Mahindra Bank? Bandhan bank has conducted its IPO just recently and don’t have much history for us to rely on.

PS: I didn’t study Bandhan yet, so probably misjudging it from a far view, but like Kotak very much.

getting bajaj finance into the pf is always a welcome thing , if anything else, for the overall beta of the portfolio…

but i am surprised , your choice to replace dr.reddy

can you please detail the thoughts behind the proposition?

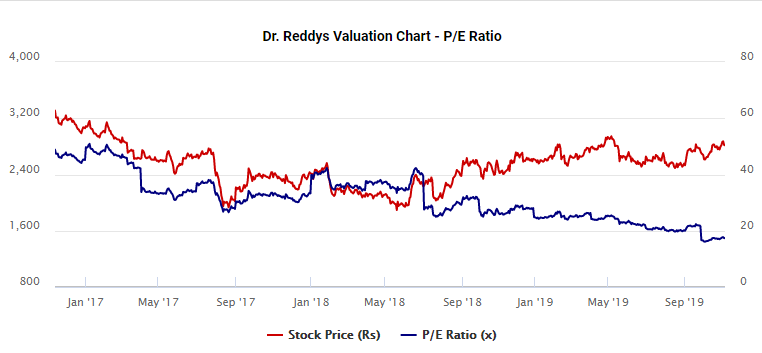

although us focused, but it has a lot of anda in the us pipeline, and recent q results have some some effects of launches , inspite of price erosion…

the price to earnings have been diverging from the price action…

imo this is one of the best bases in pharma sector technically, besides lupin and sun…

i think pharma as a sector has seen the worst, if there is a sentiment improvement coming in the market, pharma is a sector where valuation can be rerated,although domestic focused and api heavy companies are the better bets, but large caps like reddy and mid caps like torrent pharma, should be in the basket…

another point is, regarding MNCs, there is a possibility of rupee depreciation against the dollar, which might help with earnings in US focused companies in coming future

disclaimer… invested and accumulating, torrent, reddy , sun pharma among the names mentioned

not an investing/trading recommendation

these moves in a slowing down economy has been done before i think, and i recall reading a Berkshire Hathaway letter to share holder 1987 edition i suppose, where warren buffet didnt see any real effect on the economy as such because of this move, as if there is no boost to underlying demand, no company is going to invest in that kind of environment…

in india more than 60% of the economy is rural, which is agri based, keeping down agri prices to control urban inflation, is hurting the overall demand, policy measures have been taken to hand cash directly to the base , but are they effective ?

the rural economy is a spender too… i recall a bajaj corp concall somewhere where current scenario was being mentioned as the worst rural slowdown in their entire career…

anyway, i am a listener in this subject, hold no more than leyman knowledge

3 Likes

I do find Kotak Bank excellently managed. They have always proactively identified risks and successfully avoided them. To have a track record like theirs is no small feat. I found a good writeup on Kotak Bank here:

Traditional Banking, if managed by those with integrity and done conservatively, can be a huge wealth creator for all stakeholders. Kotak Bank and HDFC Bank are good example of that. I can certainly consider Kotak Bank as an alternative to HDFC Bank in my portfolio, or maybe have 5% allocation in both to reduce concentration risk. I chose HDFC Bank because of its stronger retail franchise, but it is a difficult choice.

On the other hand, comparing Bandhan to Kotak is an apples to oranges comparison. Their value drivers are different, Bandhan Bank is mainly a microfinance institution, and hence their risks are different. Replacing Bandhan with Kotak will create 20% exposure to traditional banking which I feel is too much exposure to one type of industry.

2 Likes

I agree with all the points you have made in favour of Drreddy, as they were indeed the reason I picked it up in the first place. Having an export oriented stock in my portfolio would also be good for diversification.

The primary reason I replaced it is because I couldn’t get a good grasp of pharma business so as to identify Drreddy’s strength. In comparison, consumer financing was easily understandable, and once I understood Bajaj Finance’s competitive advantages, its reach and processes which enables to quickly assess and disburse loans, it became a clear choice for this portfolio.

As i have said in the beginning, the stocks selected in this portfolio must have a huge opportunity for growth and sustainable competitive advantage to capture profits from the opportunity. This should allow one to not worry about timing the entry/exit and just SIP into the stocks in the portfolio for long term returns. I feel Drreddy doesn’t quite fit that criteria (as per my limited understanding) and would require careful timing of entry/exit depending upon its price action and prospects of pharma sector.

That said, I do have a small allocation in momentum based portfolio, where I am actively trying to time the entry/exit into stocks, so I am certainly interested in the technical analysis you share on this forum. Like you said, domestic focused pharma are better bets at present and Drreddy is still in base formation. Then should we not wait for stock to start trending or some breakout before taking a position. (Disc: have a position in Ipca)

2 Likes

I think we need to separate the two: how tax cut affects the economy and how it affects an individual business.

If government implements corporate tax cut but does not balance fiscal deficit by cutting expenses - then it is not delivering a boost to the economy but merely redistributing the wealth. The way government is spending lakhs of crores of taxpayers money to bail out PSBs and to keep running loss making unnecessary PSU like MTNL, BSNL, Air India, etc, it does not look like tax cut would boost the economy. The increased fiscal deficit will lead to inflation tax which will counteract any price cut resulting from corporate tax cuts.

There is nothing we can do about government policies, its best to focus on how they affect individual businesses, because that is where we can act by adjusting our investments. The corporate tax cut may not benefit economy, but it certainly can boost the profits of a company like Dmart. A slowdown in economy does not seem to affect it much, it would take a severe recession for people to cut down on the consumption of small ticket daily necessities. Infact we can expect more people to shop from Dmart to avail its discounts in slowdown. The tax cut not only boosts its profits in the present year, it would lead to increased future profits despite the high competitiveness of retailing, as I have elaborated in the Dmart thread.

So even if tax cut fails to alleviate slowdown, it certainly benefits some of the businesses I have in my portfolio. The only question is how much of that is already priced.

1 Like

Hello Divyanshu,

Having some questions on 3M. Request you to share your thoughts.

-

Don’t you find 3M India’ margins unpredictable. And the growth also looks cyclical? Just look at how margins turned down for the company during 2010-11 and turned up in 2013-14. Though stock price didn’t correct during those periods, it questions my understanding of the business. Please share your thoughts.

-

Very less info is available due to lack of conf calls. How did you build conviction on the business to buy 10% of your portfolio? They have recently started conf call but unable to buy with just two conf calls transcripts. Just curious if you had been through other resources barring annual reports and conf calls.

-

Did you look up other MnC industrial players like Siemens and ABB? They look strong with next gen technologies portfolio post restructuring. Why do you prefer 3M over these? Siemens doesn’t have conf calls, so hard to dig deeper (atleast for me). But just go through ABB conf calls. They are working on Solar inverters, EV fast charging, Robotics and automation, Industrial IoT…

Discl: I don’t have positions in any of companies mentioned above. Just started studying industrial MnCs and might start taking positions in these companies in coming months.

Many thanks in advance!

2 Likes

Thanks for raising the these questions. They made me do some good introspection.

Your concern is valid. The underlying business is indeed cyclical. It’s possible that margins have peaked right now. On top of that the stock is also trading at very high PE. Making a lumpsum purchase at this point could prove to be a very expensive mistake. But my plan is to build my position over a long period through SIP and hopefully hold it for even longer period. Across business cycles, my returns won’t be affected much by a few shares bought with very bad timing, so cyclicity isn’t that big of a problem, it will depend more upon what ROC and growth opportunities underlying business has, and ofcourse how much of that is not accounted by the purchase price. In that sense it is different from commodity based business where the industry doesn’t grow much over long term but has extreme cyclical fluctuations - they would make a poor choice for accumulation over long term, the only way to make money there will be through timing the cycles. This is not the case with 3M.

No, I do not have any informational edge. I base my decisions over publically available information, mostly obtained over internet. I try to get a sense of the business first by going over reviews of its clients/consumers, see what employees have to say about its culture, what other industry experts/investors say about it, and if it looks promising, only then comes the study of management’s commentry from annual reports and conference calls.

I am not betting on their product portfolio, I am betting on the culture of innovation which has produced these products. Most industrial technologies have short lifespan, they will be disrupted by their successors just like how they have disrupted their predecessors. Besides being first to develop next gen technology does not guarantee profitability either. That is where 3M stands out, they have used some very simple technologies to create profitable products through their customer centric approach. Innovation does not always have to be related to some futuristic technology.

My bet is that their culture will ensure that they are the ones disrupting instead of getting disrupted. This will ensure their profitability and sustain high ROCE. Though I haven’t studied ABB and Siemens so cannot say how they compare. Also my conviction in its culture is built upon the information and track record available for parent 3M. The assumption is that they will build the same culture in 3M India, besides selling the innovative products developed by parent through their indian subsidiary at favorable terms.

7 Likes

Portfolio update:

I started this portfolio on 1st April 2019, its close to one year since then. The portfolio is up by 18.67% as against a return of -6.62% in NIFTY500 in the same period.

In the light of recent developments, I have decided to cut my position in Bandhan Bank by half, so its weight will become 3.46%. It is because of the following risks:

- Assam Microfinance crisis: Though the crisis is limited to few districts of Assam for now, it is undeniable that the root cause of the crisis lies in overlending by MFI coupled with economic stagnation of borrowers. Debt cycles are unavoidable, and down cycle are necessary to weed out lenders taking excessive risk. I don’t believe that to be a risk for Bandhan. But, in India, situation can complicate by political intervention, like what happened in Andhra MFI crisis. Bail out expectations can lead to mass delinquencies, which will destroy the credit profiles of Bandhan’s clients and cripple its future in the region.

- Coronavirus: Yes, there are very few reported cases in India as of date, but It is increasingly looking like an inevitable catastrophe.

A virus which kills quickly and has very high mortality rate is easy to contain, as its hosts die or are identified before being able to infect others. But COVID19 can keep many infected with almost no or mild symptoms making it impossible to contain. Yet, it can make ~15% infected require hospitalisation, which can create massive burden on healthcare in the event of an outbreak. That makes economic recession very likely. As in every recession, banking and finance will be sharply impacted, and Bandhan in particular, as it serves the population which is most vulnerable to both virus and recession.

That said, though COVID19 can cause a recession, it has a low mortality rate. It’s not the end of the world. Good business will recover and thrive. and I don’t see much loss in their long term value, except for Bandhan. In case of Bandhan, the credit discipline it has been nurturing over a decade would be destroyed and we don’t know how much it will be able to recover from the blow. Unlike other stocks, there is a significant risk of permanent loss of capital in Bandhan. Hence I am cutting Bandhan’s position by half, which I intend to move back when the risk look lower.

3 Likes

Performance update:

An entire year’s gain wiped in just one month! Such is the nature of markets. My portfolio ended the year with a negative return of -2.70% as against -27.81% return from S&P BSE 500 index.

It may appear that my portfolio has fallen by the same amount as index during March, since the absolute difference between return has stayed the same, but that would be an incorrect way of measuring this difference. Remember - it takes 100% gain to recover from a loss of 50%. In the same manner, I can calculate how much excess return market has to generate to get par with my portfolio. On March 6 it was 27%, now it is 34.7%. I take this relative strength during correction as a good sign.

I haven’t made any changes to my portfolio since cutting Bandhan’s position in half on 6th March. Though I have changed my asset allocation. I wasn’t underestimating this virus, but I was pretty confident in long term value of business I hold. Hence I went into this crisis with 50% equity exposure.

I bought aggressively on the nifty fall below 8000, and increased my equity exposure to 60%, but that was before the lockdown announcement. Until that point, I was assuming it would turn out like South Korea. That people wouldn’t take it seriously, leading to initial spike in infection numbers, but that will eventually cause people to panic and take precautions, like wearing masks, avoid going outside as much as possible and regular hand wash. This coupled with extensive testing and contact tracing/selective quarantine would drastically reduce the rate of new infections, just as it did in Korea. Turns out that was quite the optimistic view. After seeing millions leaving cities because of a sudden national lockdown and all supply chains being disrupted, I couldn’t help but brace for a much more significant and long lasting impact on economy. I can only blame my lack of imagination for not foreseeing this level of disruption, even though I was pretty certain that virus will eventually spread in India too. Thankfully, the markets bounced back and I was able to cut down my equity exposure to 40%. I was able to do so easily as I wasn’t in any loss overall. Had my portfolio been in 25-30% loss like the index, this wouldn’t have been an easy decision.

4 Likes

Bro, Can u post your latest portfolio? I have been reading your thread and interested to know the latest stocks you hold now .

Thanks

Excellent point made by @sincyvarghese

Regulatory risk is a significant factor in India, and the moment government shows intention of interfering in some sector, it is wise to get out of it. That said, there hasn’t been any move yet on the retail sector, and just the entry of Reliance isn’t good enough reason for me to exit Dmart.

https://mises.org/library/bylund-silicon-valley-bad-entrepreneurship

The article is a must read for any value investor, especially to grasp the following insight.

The key is to remember the Austrian principle that value in any stage of the production chain is made possible only if there is consumer value at the end of the chain.

Value does not comes from the means of production, but from the end consumer. This is especially true for the minority shareholders, as they cannot liquidate the said means of production, to free up the said value. What assets a company holds is of less relevance than what opportunity it is tapping to serve the consumers, and what factors will ensure that its consumers are not taken away by the competition.

2 Likes

The current dip in pharma is a good opportunity to reduce my exposure to micro/retail finance. At present, I am 4% in Bandhan Bank and 11% in Bajaj Finance. I started with the same same weight (10%) for both in 2019. While Bajaj has performed well (price wise), Bandhan has lagged, and hence the present weights.

Both companies have capable managements with high integrity. But both are going through bad business environment. The earnings of a lot of people are in stress due to lockdowns and restrictions. This is reflected in the recent rise in NPAs for them.

But their price action is opposite. While Bajaj finance is making high despite bad result, Bandhan continues to sink. The conventional wisdom in this case is to cut your losers and stick to your winners. If the price is close to all time highs despite bad result, it is a bullish sign, as lot of average investors would have sold just on the superficial basis of bad results, and yet the price is not much effected which shows strong hands at work. However, I am finding it very difficult psychologically to close my position in Bandhan. Instead I have sold half of my position in Bajaj Finance, and replaced it with DrReddy. Thoughts?

1 Like

After much deliberation, I have decided to reduce my position in Bandhan and allocate it to Ajanta Pharma. My reasons:

- Micro-financing is facing headwinds while Pharma has tailwind behind it.

- Bandhan’s price is not doing well technically. Even the entire finance sector is facing challenges due to lockdowns/restrictions, the stock prices of other finance companies in my portfolio (HDFC Bank, Kotak Bank, Bajaj Finance) are doing well. Only Bandhan is lagging behind. On the other hand, Ajanta’s price is showing bullish divergence from other sector stock like Drreddy.

2 Likes

Interesting read of your thoughts, would be good to know the changes & evolution to portfolio over last year…

Thank you. I made this portfolio for my father keeping in mind that I won’t be able to actively manage it. So I picked some secular growth stories and identified the companies with durable competitive advantage. So far, I have made only slight changes to the portfolio, keeping most of the stocks that I picked initially. Despite not being able to pay much attention to indian market and keeping a passive portfolio, it has easily beaten the index in terms of returns, repaying my faith in picking these long term compounders.

The current portfolio is:

| COMPANY_NAME | WEIGHT |

|---|---|

| Avenue Supermarts Ltd | 16.79% |

| Bandhan Bank Ltd | 1.23% |

| Page Industries Limited | 7.35% |

| Asian Paints Ltd | 10.95% |

| Pidilite Industries Limited | 10.03% |

| 3M India Ltd | 5.36% |

| Info Edge (India) Ltd | 19.24% |

| HDFC Bank Limited | 3.65% |

| Kotak Mahindra Bank Ltd | 3.41% |

| Nestle India Limited | 8.74% |

| Bajaj Finance Ltd | 6.59% |

| Dr Reddy’s Laboratories Ltd | 4.39% |

| Ajanta Pharma Ltd | 2.26% |

It has almost doubled, returning 99%, at a CAGR of 30.98% since its inception in April, 2019, beating the index which has given a CAGR of 20% in the same period.

It is tempting to try and time the market by selling the stocks that have run up a lot, for example, Dmart. But I don’t have any faith in my market timing skills. If I was trying to time the market, I may not have picked Dmart as its price had always seemed ahead of fundamentals. All I know is that over the long run, say a decade or two, the effect of initial overvaluation disappears and returns approximates the return on incremental capital invested in the business, that means, we will do fine just by remaining invested in companies that can invest money in their business for high returns.

5 Likes

Thats great, yes I re-read your entire thread again yesterday and it was great to go through it from beginning. My journey has also been like your this portfolio’s, with similar thought process, except that the portfolio is for self…

I see from last 1 year or so, you have not bought any new stock and neither completely exit any…thats great, only proves that your initial investment thesis was right for you…

The current percentage of individual stocks - are they result of simple holding like coffee can or any rebalancing you did among the existing picks?

Also, as you said this portfolio is for your father and I read somewhere up that you have other more high risk high gain small caps for yourself like some Chemicals/Organics and GMM Pflauder etc. …in this context…would be great if you can share your own portfolio, the evolution of that in last 2 years (you may mention from earlier also if significant) and also how its performance fared as compared to your father’s portfolio during the same last 2 years…It will help us learn and understand better how two different hats can be worn by same investor…Thanks!

2 Likes

Yes, they are result of simple holding.

I have tried various approaches over the years. When I first started investing (2015), PE ratio was the only tool in my repository. Like a naive investor, I assumed that low PE stocks are cheap and one should wait for index PE to be less than 15 in order to put big amount in markets. I bought many cheap commodity stocks (like Vedanta, NMDC, Tata steel, etc) during that period only to see them become cheaper. Learned hard way that there is usually a reason for stock to have low PE. But since it was a small allocation, I just stopped paying attention to market, checked back sometime in 2016 when the prices have recovered a lot, exited my investments and decided to study more before investing. In doing so I avoided a major pitfall of not taking personal responsibility. A lot of people blame others (operators, advisors, etc) for not doing well in the market. Only by realizing your own incompetence can you work on fixing it.

As I studied, my respect for markets grew. Market may have irrational bursts from time to time, but over long period they are mostly correct, and they are much better forecaster of future than any single human can ever hope to be. Just as those low PE stocks were cheap for a reason, I realised that many high PE stocks may also have good reason to appear expensive. That there may be good investments hiding in plain sight, appearing expensive superficially because of high PE, but they may very strong competitive advantage which justifies their expensive PE. In doing so, I avoided a second major pitfall. Most people who read widely are obviously smart, but when their theories are at odds with the market, they blame it on the foolishness of masses, instead of revising their theory to figure out what the market is saying. I am open to have my theories falsified to figure out which narrative explains market.

From 2017 onwards, I started doing qualitative analysis of those quantitatively expensive stocks, to identify such hidden in plain sight gems. It is from these stocks that I made my father’s portfolio, and they had my major allocation. I also tried other approaches. One was to try bottom picking in good companies. They were usually okayish companies that were highly priced before they started falling (eg Khadim). Turns out I’m not good at it and only made ~4% cagr in this approach. thankfully it was less than 10% of my allocation. The other approach was momentum (again ~10% allocation), where I bought good companies whose business was improving. GMM Pfaudler is one such example. These weren’t the kind of business that I would buy even if its price dips. Nor was I trying to do any bottom fishing. So I would keep a stop loss, and exit them on reasonable gains. I made about ~20% cagr in this approach, but yes, it is lacking compared to my father’s portfolio. My biggest allocation have been to these quality compounders. These are the stocks I am happy to buy at market dips. The only difference from my father’s portfolio is the allocation. Instead of equal allocation, I had much more of Dmart, Bandhan, and InfoEdge, and little of 3M, Page, Nestle. The allocation depends upon how much conviction I have in their story. Thankfully I am making 40% cagr in this portion, so I can say that my unequal allocation has paid nicely.

10 Likes