Stephen H Penman in his book Financial Statement Analysis and Security Valuation talks about the concept of manufactured dividend. You just sell a few shares and taken the dividend you think is appropriate. The same book also deals with dividend irrelevance concept. Look it up on amazon if you are interested.

2 Likes

I think one must be clear if one wants to have dividend or partial profits. There is nothing wrong in partial profits. Infact, now I have started somewhat believing in this even in good/great stocks. It gives you liquidity to buy more when they fall. However, dividend is to be taken when no intent to sell. Strategy to sell has to be clear is what I have learnt…yet to practice this new learning though. Thanks

Dividends reduce the value of the ownership as well. In that sense, whether you sell some shares or the company gives you dividends, both actions reduce the value of your ownership in the company.

1 Like

Sir,

Stocks need to be bought not for dividend but for share price appreciation. Thats lesson 101 of stock market investing. Following are the points in favour of my argument:

- Dividends are very tax inefficient - a company first earns 100 Rs profit before tax and then pays 30% tax on that and then pays another 22% DDT - which means that for every 100 rs of profit before tax, only 55 Rs reaches the investor and 45 Rs goes to the government. Better companies either go for buybacks or invest capital wisely, thereby saving taxes for the investors and increasing the share price. In case your portfolio is big and your dividend is more than 10 lakhs per year - you pay additional 10% dividend surcharge which has been introduced few years back.

Infact rather than paying 22% taxes on dividend, one can always sell a part of the portfolio and pay only 10% on long term capital gains.

-

Unlike a bond where the company is contractually obligated to pay a certain % as interest, no dividends are guaranteed in the long term.

-

Most high paying dividend companies are anyways PSUs which have proven to be bad stocks in the long term (although they can be excellent in short/medium term if one has the ability to time and buy at low enough valuation). In many other cases, high dividend paying companies have almost got very little ability to grow. Both of these factors run against the prospects of share price appreciation.

-

Also, I saw a lot of names with 2-3% dividend yield - if you are doing that then you are primarily anyways doing growth investing as 2-3% is too less from an Indian context and you are betting on the earnings to rise - not different from regular investing.

To the extent that in many cases, dividends indicate management intention to share wealth with minority shareholders and signify that earnings are not fudged - some dividend is however good.

The other commonly heard argument is that for high dividend paying companies, generally the yield supports the fall in the stock price - this might be true but then the stocks are not bought for the purpose of only to save oneself from fall in stock price but are and should be bought primarily for wealth creation.

So overall my advice is kindly look for companies which have good prospects over the long term and are available at a decent price. You can always sell some shares to create liquidity if you need some on a regular basis.

13 Likes

I agree with your points. Why do companies pay dividend at all then? I read some reasons mentioned by you like management intent to share wealth and make investors believe that profits are real…is that the only major reason? Are dividends given for goodwill? I am just thinking loud…

I have read many reputed investor say that they look for dividends because of above goodwill reasons and also that they would like to see dividends rise…so is dividend only a tool used by management to attract and hold investors? Is it only a measure to fulfil needs of certain section of investors or promoters themselves…does it make no business sense at all?

A company must aim to maximize shareholder value. If the company cannot reinvest at the required rate, they must pay it to shareholders so that they can utilize it to get the required return on capital. That is the theory behind it but what happens is not always linked to theory.

1 Like

If the management does not find it efficient to reinvest the cash, then they could buyback their own stock.

Some companies are able to generate good returns on capital… They still give Dividends.

They can buyback if the price of stock is depressed. Otherwise it will be a bad decision!

Somewhere in this forum or any place else I have read that dividend improves ROE while buyback improves ROCE. So in case the cash equivalents are more with the company, they will see ROE and ROCE. Whatever they want to improve upon, maybe they will decide whether to go for dividend route or buyback route.

Cos pay a dividend for a variety of reasons some of which I have already alluded to in my post. In India, given the tax inefficiency of dividends vs buybacks, logically it makes sense from a tax point of view to do buybacks and not dividends. In countries outside of India where the tax rules might be different - may be it makes sense to even pay a dividend over buybacks. But in India reverse is the case - at least as of now given current tax rules.

Also, many categories of investors prefer dividends for reasons including dumbness or ignorance to even sophisticated investors like some insurance companies preferring to invest only in dividend-paying companies.

Bottomline is that very few companies are run to maximize the per share intrinsic value of its shares (Berkshire Hathway certainly is run that way). And many investors are also not looking to maximize returns on their investments but seek other soothing candies like dividends even though it may be meaningless in most cases. Also, many people just don’t know or care.

So in an ideal world, one should seek to invest in companies which are focused on maximizing per-share intrinsic value of its shares Investors should work hard towards finding such companies (I certainly know a few of them ![]() ). Such companies in the current Indian context would not pay any meaningful dividend even if they have the cash but will do buybacks or chase other high return/low-risk avenues of deploying money. But the world we stay in is far from ideal.

). Such companies in the current Indian context would not pay any meaningful dividend even if they have the cash but will do buybacks or chase other high return/low-risk avenues of deploying money. But the world we stay in is far from ideal.

1 Like

Promoters, employees cannot sell their shares, and want to get paid, so the management resorts to dividends. It is inefficient but the only way.

Also, some funds have a lock in period, so to get their participants to see some cash … Dividends.

It is a very inefficient way. Buyback is always so much better, no matter at what price.

@8sarveshg Thank you for the information provided.

However, when we are analysing companies to invest and to see where they are financially strong, we look at dividend yield / dividend growth also. If the company is not paying out dividend it is considered as negative.

Dividend should be seen in this perspective , when you look at current prices with respect to dividend its 1-2% kind of levels, you have to look after a long period with respect to the price you paid initially.

4 Likes

Looking at dividend yield with respect to original price is inaccurate way of looking at it. Consider fixed deposit in bank, lets say Rs. 100 was invested 10 years back at 10% yield, and today the principal and interest makes it to Rs. 259. Hypothetically bank asks customer to put the total amount in saving bank with 4% yield and inform the customer that their original amount was Rs. 100 so they would still get Rs. 10.36 (4% of259) interest which comes to 10% of the original amount. Who in their right mind would go for this!

So why to anchor yourself to price of the stock originally paid. Dividend yield should be calculated as per current market price as that’s what the capital you have. If capital can be shifted to some other stock with better growth perspective in compare to what you have ( including dividend yield at current price) then it should be moved, it makes more sense financially.

5 Likes

For long term investor who invests for dividends … Dividend Growth is very relevant metric …

It is Real cash flow a investor generates without been subjected to making decision of selling right . So it is should be compared with alternative FD or fixed income options

Lets say you had invested in HPCL in 2013/14 , post bonus its current price is around 40 odd and you get dividend of Rs 17 ie 30% on your paid price in 2013 . Assume alternative if you had invested in any PSU corporate bond like SBI bonds in 2013 you would have recd pre tax 10% and post tax around 7%/8% .

Power Utilities ( and to good extent also OMC in India ) are often called Quasi bond for this very nature .

5 Likes

HPCL dividend yield since 2013 has never crossed 6 %. The maximum yield was 5.71 % in the year 2017 . So even post tax return every year were more in FD than dividend from HPCL. The benefit to hold on to HPCL comes from stock price appreciation not from dividend. If there is a stock which has better growth than HPCL ,then HPCL doesnt deserve to be in portfolio even if the dividend yield of the next stock is less.

![]()

( ref: https://www.valueresearchonline.com/stocks/Finnance_Annual.asp?code=1578)

Kindly read my earlier post carefully …

then check effective post bonus price of HPCL in value research online in 2013 it is around Rs 37 to Rs 44 in Sept 2013 …

Then go to check what is current dividend per share data in value research site … it is Rs 17 per share …

Then divide 17 ( dividend per share ) / 42 ( Effective Avg price I paid in 2013 ) = Dividend Yield for me is 40%

1 Like

I never said what you wrote is wrong you are calculating yield based on 2013 price and i am calculating based on each year closing price.The right matrix should be based on the stock price at the time of calculation not what was originally paid. To hold on to stock just for dividend doesnt make sense, if the company is not growing.

That depends on the requirement on the investor. If the objective is wealth protection, these bond kind of investments make a lot of sense. When someone builds a house and looks at rental yield, they don’t mark-to-market their house every year, nor do they flip it based on yield. The objective here is low-risk, low-return, low-churn, low-maintenance and in that sense, I can understand calculating yields based on invested price. I believe it is for this reason that Buffett still holds Coca Cola because he looks at yield on a cost-basis and not opportunity cost basis or mark-to-market basis. Again the key differentiator is the requirement of wealth protection vs wealth creation.

9 Likes

When we talk about HPCL, hpcl dividend yield based on original price appreciated to 40% only because HPCL has grown EPS by leaps and bound every year and it has lead to better dividend and higher stock price.

![]()

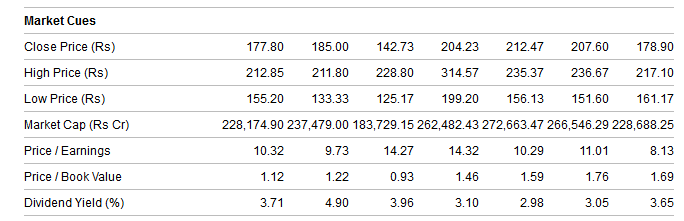

If someone was aware in 2013, that HPCL would grow like that it was sensible to hold on to it for last 5 years or so. But to say in future HPCL would grow at same rate, some one needs to understand the company and its business. IF in 2013, instead of HPCL someone would have bought ONGC for wealth protection lets see how he would have done

Price paid in year 2013; 151 ( assuming lowest of year, highest was 207), price in year 2019: 152, dividend yield in year 2013 : 3.05% and dividend yield 2019: 3.71%. Just choosing ONGC would have destroyed capital ( taking inflation into consideration), dividend every year less than FD, so whats the difference between HPCL and ONGC, the growth which made all the differences, not the dividend.

1 Like