The sector has a huge opportunity but the companies don’t have a lot to differentiate themselves. Its difficult for any company to build a moat in this industry.

Disclosure: invested with small position relative to the portfolio.

I beg to differ with the point that a company cannot build a moat in this industry.

Please find the points below

A lot depends on how a company goes for bidding. Those who bid aggresively throwing caution to the wind will find themselves saddled with debt when the time comes for execution.

‘Capacity to suffer’ is the most important trait that can differentiate a company in this industry

Being asset light helps

Hands-on approach of the management - Main reason behind the performance of Dilip

Management’s expertise - EPC or BOT, Asset light/Integrated model; Not everyone can excel in both the models

A little bit of luck - as the order allotment is at the mercy of government; But Lucky are those who are prepared enough to grab the opportunity with both the hands as and when it arrives

Please read this post on KNR to understand how to think about this industry

But KNR is small compared to dilip is it? also i believe next theme is infra given the fact of sagarmala and bharatmala…if yes we need to identify those companies which will be atleast 1 or 2x in 2 years? all pls share your thoughts?

This is old resarch report from edelweiss dated Apr’17. Please gothrough if you didnt. You will find a lot of information about dbl and intersting graphs like bidding cost gap(showing not too aggressive), peer comparision,etc.

Also make a note that dbl face value is 10.

From order book you can say it is safe for next 3 years with revenue increasing CAGR 15-20%.

Disc.:Invested.

Absolutely correct…the way of doing business matters rather than the size of the business.

Also the presentation on KNR is a great study on the perils of investing in a business with negative or low operating cashflows…a very important lesson to learn.

Thanks for sharing.

Dilip Buildcon is the best listed construction company in terms of execution.It follows clustering strategy in bidding for projects. This helps in reducing the operating cost. It also owns it’s own equipment, so high debt can be seen in the balance sheet.

I also have this question. How is it possible for a profit making company not to pay tax, that too when it is a public knowledge. Taxmen should have been standing at their gate by now.

Deferred Tax is typically tied to depreciation. Since DBL owns most of its assets, it can claim high depreciation rates. Deferred tax liabilities will be settled in the future, and is sometimes beneficial to keep in the books (corporate tax cuts are hugely advantageous for deferred tax)

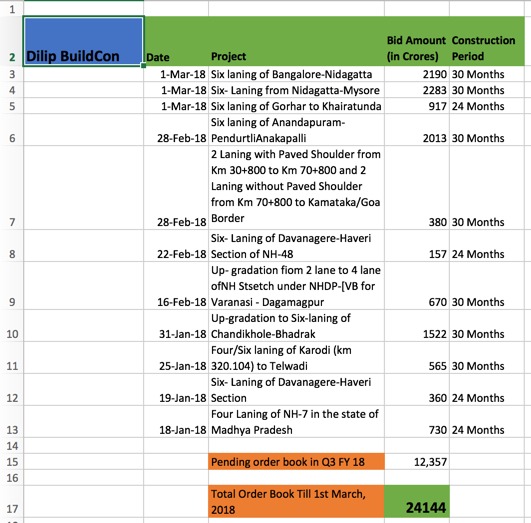

This is a good recording of recent order book Nand! In FY18, Dilip Buildcon is expected to clock a revenue of 7,000 Cr. This means that with recent order wins, Dilip Buildcon has order visibility for almost 3 years

Order winning is one thing, but what concern me the profitability at which these orders will be executed. It’s easy to win them as lowest bidder but is it sustainable to make profit as lowest bidder. Further, as expected after bharatmala, there will be a flood of orders, and we will be falling short of companies able to execute them in the timeline.

Invested…but fingers crossed …cautiously.