Hi,

Yes the viewership of CNBC channels and also money control app has increased substantially.the new premium feature of money control is also cheap which is fueling that.

Thanks,

Deb

Hi,

Yes the viewership of CNBC channels and also money control app has increased substantially.the new premium feature of money control is also cheap which is fueling that.

Thanks,

Deb

Yes off course that is the case, I was talking about the rally from last two days. but network18 is in UC from few days. lets see what happen next.

So I was actually thinking and searching this for few days but no luck. Will someone here plz explain me 2 things 1)how the proposed merger going to help Network18 and Tv18?

2) what are the future prospects of this industry going forward? Yes I know it was discussed in this forum but explain to me in a very simple layman language as you will explain to a school boy.

Please.

Thank You

Hemant Ghai had the advance information about the recommendation to be made on the “stock 20-20” show, co-hosted by him, and that he directly or indirectly used it to his advantage, Sebi said in an interim order.

A careful study of results of last few years will reflect that:

You will also find another interesting thing. Den is traded at less than cash value on books. Hathaway is 70% cash value. I am amazed at this.

Lack of clarity regarding the competition intensity is main reason and overall landscape in India is still vague when looked in the context of consolidation of global media houses. Media jigsaw puzzle is very unclear as the fate of Zee Entertainment is still hanging.

Arbitrage Opportunity

Den networks

Its current share price is Rs. 40.45

Market cap = Rs 1,930 crores

Target = Rs 51.15 (return of 26%)

Short term opportunity based on price/ value mismatch.

Working:

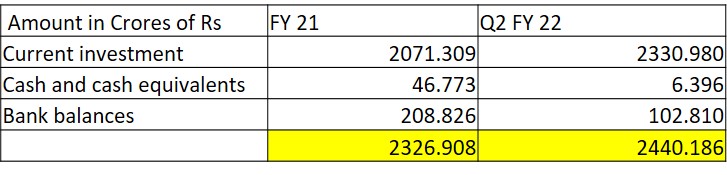

Here is the Data of Liquid assets that Den networks own

In October-2018 it has issued shares to Reliance industries at Rs. 72.66 and raised 2,045 crores of Rupees.

Here is the Position as on 31st March – 2021 and 30th September 2021

In current investment we can check the FY 21 annual report, it has invested mainly in Debt mutual funds. (Page no 81, FY 21 annual report) which means these investments can be considered as good as cash (very liquid)

Its current share price is Rs. 40.45

Market cap = Rs 1,930 crores

The logic here is, that the share price should ATLEAST trade equal to the value of the liquid investment it has. Here in this case potential market cap of Rs. 2,440 crores (price of 51.15)

Meaning an Upside potential of 26%

Why I think this discount will narrow down?

What I feel about this opportunity?

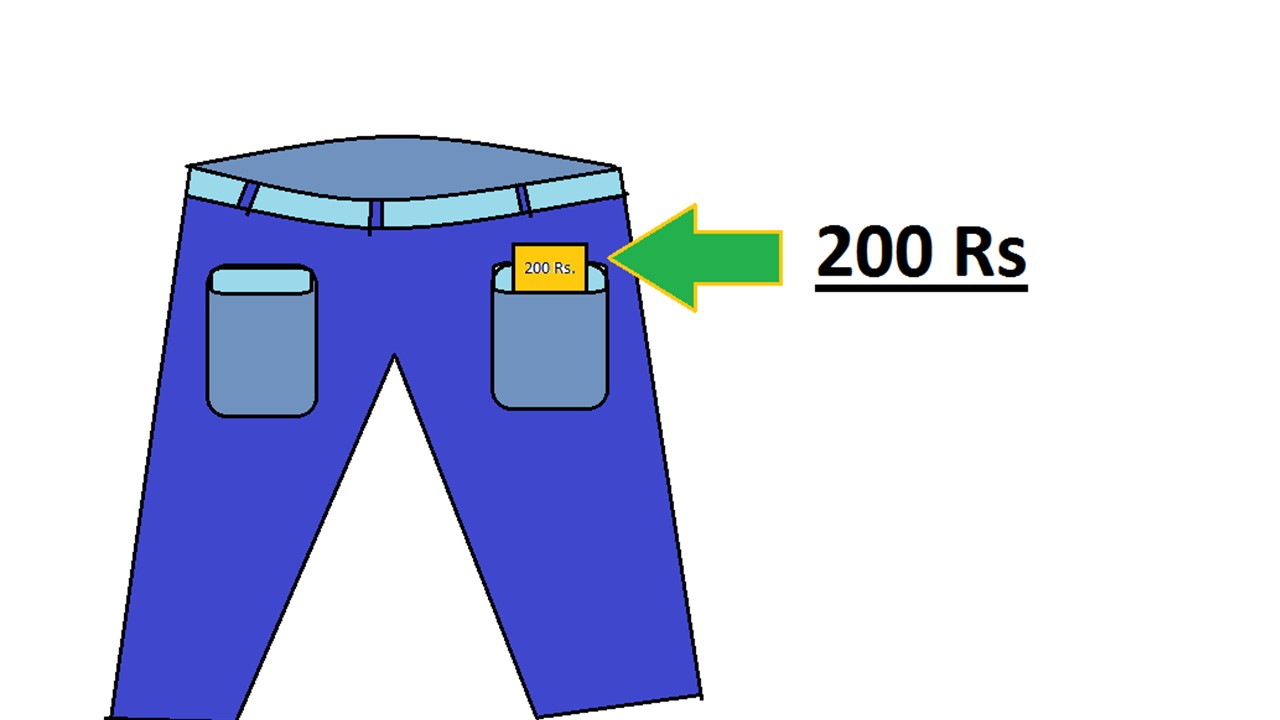

Rupees 200 in a pant, that is on sale for Rupees 200.

Here once you purchase the pant, 200 rupees is all yours, meaning you get back what you paid for.

So the pant becomes free of cost for you.

Risk factor:

Disclosure: I current hold few shares which I had purchased for tracking purpose, No recent investment is made on the above logic of market cap trading less than its liquid assets.

Would like your views and opinion on this Opportunity.

Not much activity on TV 18 broadcast.

Views invited on the Reliance group company with reducing debt & improving top bottomline & ROCE ever since RIL took over the co from Raghav Behl. RIL OWNS 60% with FIIS owning 14% & RJ another 1.5%

Launch of Sports 18 WITH FIFA world 22 rights already in bag . What if they bag IPL rights as well?

What will be effect on tv18 of the murdoch and uday shankar deal ? What will be the end shareholding of TV18 in Viacom18 ? Anybody analyzed the situation.

So far the company is not disclosed what percentage stake will be given for Rs.13,500 crs investment by Murdoch & co. i could not able to understand why the markets reacts so negatively about his news.

There is a note by spark capital saying after the investment from Murdoch & Shankar deal TV18 will hold only 18% of Viacom18. I don’t know how spark got to this number.

Actually in social media, there is a rumour that stake of TV18 will reduce significantly in Viacom18 after this deal and that will affect its profitability. Further some say that if they win IPL rights, which may cost them 33,000 cr base price + 50% premium, then it will also affect the revenue of tv18.

Clarity shud be awaited. Mr. Ambani is known for value accretive deals.

agreed but this is a good example of poor corporate governance in a listed company, that too Ambani`s as they are famous for this. I am not expecting clarification from company unless stock exchanges ask questions on volume surge or shareholders raises alarm.

the reduction in stake is pretty much a given considering primary infusion of capital, isn’t it ? The value of TV18’s stake in Viacom18 after the infusion shouldn’t decrease but in the short term, their share of the profits will take a hit as the new capital won’t start generating profits right away…I guess that’s why the stock has taken a beating…in the long term, the revenue should increase in a way that ROEs are at least as much as they were before investment by Bodhi Tree…that would have been the intent of Murdoch anyway…

TV18 Results out:

Revenues decreased from 1512 cr to 1295 cr QoQ while PAT decreased from 220 cr to 60 cr QoQ.

Profitability was impacted due to

25% increase in operating expenses

Decline in Subscription Revenue

Colours Rishtey went off DD FreeDish

Flat Advertisement Revenues

Decline in news business despite state elections.

Overall, I personally don’t see the company recovering from this anytime soon.

Ps. Not investment advice.

Anyone still tracking this. What is future of combined entity with Network18 and TV18 merging?

How about current valuations?