IMO, it would be difficult for the old paint entrants to enjoy the same premium that they used to command. Paint industry is getting hugely crowded and with new players entering the market such as Grasim, Astral, Pidilite, and JK Cement, old entrant’s volume, pricing power, margins would be under pressure and so is their stock price. Just imagine, Grasim eyeing 10,000 crores in next 3 years which is 28% revenues of Asian paints. I would avoid buying these names due to these headwinds. Take informed decisions !!

@sameernics Thanks for reply

I completely align to this. But I’m betting on the volume growth over next 10 years in india, with realestate cycle going up and one more thing for my view, when we paint the house we ask for the brand of paint which is being used by contractor, well this is stuff I see lot happening with Fevicol and everything, this is just my safe bet

Well I believe that eyeing and reaching is two different thing, surely grasim couls achieve this due to it’s reach in dealership and everything because of ultratech but I strongly believe this is not gonna be possible with the dominance which Asian Paints commands.

Yes Paint is Bread and butter for them but

- No. 1 Integrated Home Décor Player

- No. 1 in Decorative Lighting

- No. 2 in Fabric & Furnishing

- No. 1 in Wallcovering & Textures

Although these are segments which does not generate a lot of revenue or profit but they are actively foraying in different domain. Asian paints at P/E of 90-100 is not worth the money but at multiple of 50, there is not a lot fo risk and in this overheated markets (strictly my view), it’s better to find safe pockets.

2 Likes

It’s not the first time AP has faced competitive threat. They have great management who have so far delivered fantastic earning growth and built a strong business. They will find a way to bring back the growth. Give them a couple of years. What they might lose in market share and volumes, they will make up for it through their other initiatives. They have capital, talent, distribution muscles and a strong brand to do that.

Disc- Invested in a few months ago at 2800 level.

1 Like

Hey Dhruv! Sai here, 27. Commenting since it is appreciated ![]()

I think I can totally understand why 65% of your equity is sitting in finance. It is probably a no brainer that financials are the most favourable in terms valuations now, however the markets don’t seem to appreciate it. Also, as we believe the GDP to move up, it is only common sense that we think financials have to do well when the country’s economic performance goes up. The likes of HDFC, Kotak are definitely good buy for long term. LIC infact was a good buy some months ago, considering the valuations in mind comparing the EV ratio to that of HDFC Life and SBI Life.

Though you are betting on the spending capacity improving in terms of Bajaj Finance, SBI Cards which would also obviously happen, it would only be fair if you also looked at the investing potential which would improve in the future. We are seeing in front of our eyes how investing in stocks and MFs have become easier and the numbers will improve in the future. With that in mind, I cannot understand why you chose not to have an AMC business in the financial lot. Even from a valuation perspective, a couple of the businesses are still trading at a decent FY25x PE, though the market leaders have run up. And all these businesses are in fact showing stronger earnings growth and beating the market expectations.

Still have a lot more to discuss and understand, but let’s go ahead with this for now ![]()

Hey Saiguhan,

Thanks for the comments.

I completely align to this view, I entered it around 700 ish and got exited at 1000 ish, I moved that money to HDFC Life, I’m big on insurance as it is my proxy play to indian healthcare sector too.

Absolutely Agree with this one, My father also invest in the market, He has exposure to AMC’s like HDFC AMC with exposure upto 10% of the portfolio. I don’t like to have same stocks in both portfolio’s. Just a safety thing. I have my eyes open to stocks like CDSL, CAMS, BSE and some brokers and wealth management services. I don’t like the current valuation and I believe we are going to have slowdown in them with saturation of new users. I’m also looking for the small term downturn in markets and these companies would be most affected.

More of, I have increased my positions in cash and long term bonds, preparing myself for short term opportunities and looking to extend my positions in Kotak (I have exhausted myself i HDFC Bank positions of over 25% now in HDFC), Bajaj Finance and HDFC Life in Large caps and also increase exposure in small cap banks (small finance banks) and chemical sector.

So lot’s of action ahead! Looking ahead for further discussions. Would love to listen about your observation on different sector!

Okay, I am curious. What led you to this move? Don’t you think LIC at 1000 was a hold? I mean, it isn’t bad that you booked north of 40% returns but I think LIC may have more value than HDFCLife at this point, or let’s say the upside is more for LIC in the medium term. Ofcourse, from a decadal perspective HDFCLife can give more returns.

Yeah this makes sense! Current valuations are bit stretched. Let’s see if some kind of downturn occurs.

Regarding other sectors, I normally stay away from sectors which I don’t understand well. For example, chemical sector. I am mostly value driven and I prefer simple boring investment ideas. One of the best examples sitting in my portfolio right now is Sun TV.

Frankly speaking I stay away from PSU. That is my rule and I pretty much stay out of this bull market. Th e major issues is, these company are for public good not for money making. I believed that LIC was at dirt cheap valuation at 700 that’s the reason I entered. There is overhang of OFS, for government to comply with 75% holding rule of SEBI. I may be wrong but post election we could see huge de-rating of these companies. Just my view.

Completely align, expecting solid 15-18% CAGR from HDFCLife and that’s the reason to make the shift .

Yes I try to stay away of what I do not know, but some speciality chemicals are showing good future prospects with solid balance sheets. Yes the sector is in extreme issues due to china’s dumping and sales are low but with growth in India’s GDP I believe the internal consumption would pick up and this would be huge proxy play for me. So I have started reading and learning about this sector.

More of there are bunch of micro caps and nano caps with huge potential, the only thing is to buy a good company. Still I had not find any story which I would love to make huge position wrt to my portfolio. But still looking

I have never invested in media company and not aware of this stock. Would love to read more about that and what other stories/stocks do you hold in your PF. I would post my updated PF in the thread soon!

Looking forward to hear back!

Rather 75% shareholding Cap will work in favour of LIC. Still 20% Further public issues are going to come…that will make its price soar to much higher levels from here. Why you think, this 75% condition will drag down the price?

Thanks for the interesting comments.

I understand the view on PSUs, however I think if value lies there, it commands respect, any sector for that matter. For example, PSUs 2-3 years ago or LIC at 600 levels, SBI in 2016 etc. Coal India at 10% div. yields in my opinion was a solid buy. But yes, if you have a framework or rules, you should abide by them.

Yes I am aware. But I think any Govt is smart enough to go OFS only if they believe it has reached the value it is deserved to be sold. Initally the IPO was pegged at 12-15L Cr INR, meaning nearly double the current levels. There could be a chance the govt might not start trimming their stake until LIC moves somewhere closer to there. Also, we have the 10 year exception to promotor stake. So let’s see. Yeah, LIC will lose its market share to HDFC Life, SBI Life etc but the question is despite of that can they keep showing earnings growth and if yes, the market should atleast decently value LIC’s EV ratio if not that of HDFCLife and SBILife.

Understood. My problem is, I have to learn about how these companies go on about their business and how they can grow their earnings. One of the best examples I have is Gulf Oil. For me, it is a decent buy at the moment, but March last year was a very good buy and in fact, I have been following them for a while now. at 9xPE, it was a great buy. They are exploring new areas, especially with the EV oil and when EV becomes a play in India, both castrol and Gulf oil will have a role to play. Another good aspect was that both these companies hadn’t performed in terms of stock performance. I just did not have it in me to follow my instincts.

True. In any market, there are always opportunities. We just have to be lucky I believe. I think of one or even two of the rice export players is undergoing some sort of consolidation for a while now. I actually was invested in LT Foods since Oct 2020 and sold it last year to enter KRBL. Seems like a mistake, but I am in it for the next few years, It has done nothing in my portfolio for a while. I am keen, let’s see what happens.

Ah Sun TV is simply because of 2 things. 1st thing is a mix of reasons such as low PE compared to median 10-yr and historic levels, SUN is one of the most watched channels in the country and they have a huge portfolio. They don’t care about corporate governance by the looks of it but they are a very solid promoter. I don’t see any reason for them to sabotage the business. I am also biased since I am from the region.

2nd thing is they own SRH. I think IPL is the fastest growing brand in India and definitely the world has started to turn towards cricket and it can only become bigger in the next decade. Hoping they will win atleast 1 IPL in the next 5 years. The team looks good and they are performing better than expected this season. So let’s wait and watch.

I will also post my updated PF soon, I am also not sure if I should really post it. Not because of negativity or bad comments, some positive comments can also make me biased. I am hoping not to follow the crowd. I like to stay away.

Yes I missed that!

Yes, but you can take me as HDFC fan! My family for last 25 years are banking with them and I believe that HNI clients would take them for insurance as trust is really important and, “LIC IS ALWAYS TRYING TO EARN”, they are not friendly policies for consumers and I don’t like that, may be better for business but noone iin genz is going to so those rubbish ulips or insurances with them they would move to HDFC or ICICI or SBI. This is my super long portfolio stock and I’m extremely biased on this which I should not be.

Yes this makes sense but for me I’m into speciality chemicals, I am not able to find them for dirt cheap valuations but current valuation has started giving me comfort. I pretty much stay away from hot sectors like EV, Solar or renewables for now, the valuations are extremely stretched. I don’t know about gulf. Not tracking that.

I did not knew this, I would love to own stock of some IPL teams for sure. I would definitely go and research about this one. Recent addition of Gujarat and Lucknow was around a billion dollars if I’m not wrong so team like SRH must have value of 10K CR. I’m check it out and would like to discuss more further.

Understood, completely make sense !!

Thanks for the response and feedback Dhruv! Yes, I do get the idea behind favoring HDFC. It has created wealth for a lot of people in the past.

And yes, regarding the IPL, it is a long ask. Let’s see how it turns into favouring the business or if SUNTv can unlock some kind of value in the future. But I am invested cauz I think the downside is quite low. It has to take a disaster like Covid or some other event to bring it down and in that case, there would be lot of other opportunities to move to.

Current Update of the Portfolio

With the current market pullback, I’m reinvesting in my holdings and this time I’m making sure not to repeat the mistakes I previously made.

Overall Division

- Real Estate (Residential)- India: 17.70% (In next 3 years exposure would be around 30-35%)

- Stock Investment - India: 26.55%

- Cash FDs - India: 1.77% (AU Bank 8% + Lien for IPO)

- Liquid Cash (savings + emergency) - India: 15.93% (Ready for deploying the money)

- Stock Investment - USA: 5.31% (HDFC ADR, Alphabet, Snowflake and TD)

- Retirement Investment - USA/CA: 26.55% (US Index + Bank Share(ESOP))

- Friend Help (no Interest): 6.19% (want to ask back but don’t know how could I, I think should consider as NPA)

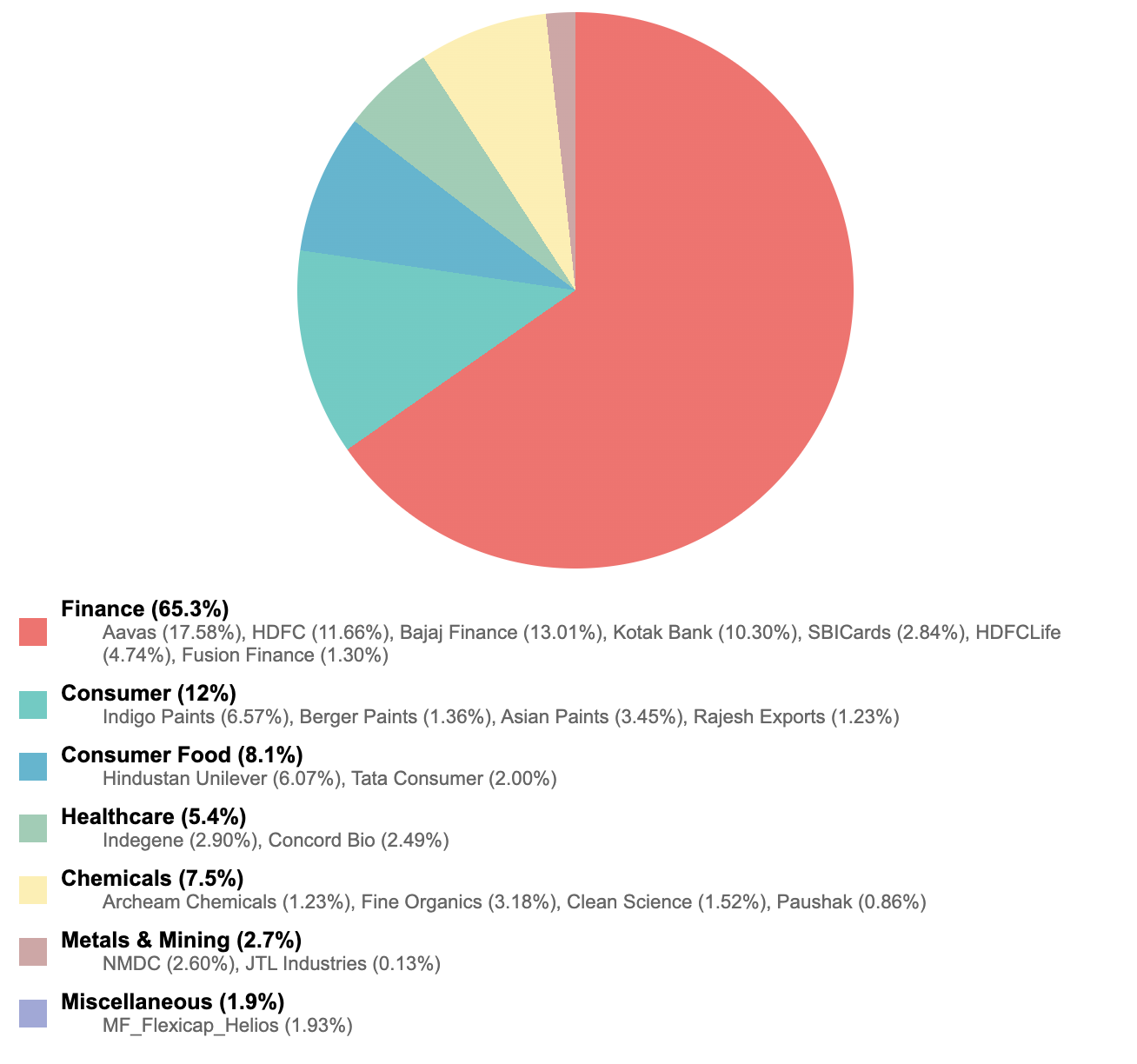

Complete Portfolio Insights (long only) (XIRR: 17.92%, ROI:10%)

Check this out

- Finance - 65.3%

- Aavas: 17.58% (XIRR: 6.24%)

- HDFC: 11.66% (XIRR: 12.48%)

- Bajaj Finance + Kotak Bank: 13.01% + 10.30% = 23.31% (XIRR: Bajaj Finance: 6.89%, Kotak Bank: -1.41%)

- SBICards + HDFCLife: 2.84% + 4.74% = 7.58% (XIRR: SBICards: -10.70%, HDFCLife: 21.39%)

- Fusion Finance: 1.30% (XIRR: -82.24%)

- Consumer - 12%

- Indigo Paints + Berger Paints + Asian Paints: 6.57% + 1.36% + 3.45% = 11.38% (XIRR: Indigo Paints: 34.19%, Berger Paints: 5.69%, Asian Paints: -6.92%)

- Rajesh Exports: 1.23% (XIRR: -45.83%)

- Consumer Food - 8.1%

- Hindustan Unilever: 6.07% (XIRR: 7.29%)

- Tata Consumer: 2.00% (XIRR: 11.70%)

- Healthcare - 5.4%

- Indegene + Concord Bio: 2.90% + 2.49% = 5.39% (XIRR: Indegene: 0%, Concord Bio: 110.94%)

- Chemicals - 7.5%

- Archeam Chemicals, Fine Organics, Clean Science, Paushak: 1.23% + 3.18% + 1.52% + 0.86% = 6.79% (XIRR: Archeam Chemicals: -6.10%, Fine Organics: 12.39%, Clean Science: 10.46%, Paushak: 18.02%)

- Metals & Mining - 2.7%

- NMDC: 2.60% (XIRR: 40.11%)

- JTL Industries: 0.13% (XIRR: 14.26%)

- Miscellaneous - 1.9%

- MF_Flexicap_Helios: 1.93% (XIRR: 41.26%)

I’m bullish on India Finance, yet a low yield on XIRR and largely due to under performance of largecap banks and NBFC. I misread the microfinance and personal lending and invested in Fusion Finance on the top of cycle, now showing NPA’s, yet the exposure is minimal but would love some thoughts on that. Additionally have some exposure in Rajesh exports, I’m planning to leave both of them as it is, not cutting losses but not averaging.

I feel I have high exposure to largecap and that is my style, but am open to some smallcap and microcap suggestions for long term.

It is still a financial heavy portfolio within equity. Not sure why are so much inclined to investing into this sector leaving out tailwind sectors. It is time to slowly deploying the cash into these tailwind sectors as the market is playing out exactly what I said on March 13.

Also you can look at having some exposure to long tenure bonds for portfolio stability and steady stream of income. IMO the current yields are expected to further drop post RBI rate cut action.

Take informed decisions.

It’s true; my portfolio does have a heavy concentration in financials, and I agree that diversifying into tailwind sectors could add resilience. I’ve mainly focused on finance due to a strong personal conviction about long-term growth in this space, though it hasn’t always panned out in terms of XIRR, especially with large-cap banks and NBFCs underperforming.

Deploying cash into other promising sectors is a solid call—I’ll evaluate those options, particularly ones with growth potential amid current economic conditions. Your point on long-term bonds for stability and income is also spot on, especially with RBI’s expected rate cuts. I’ll definitely take a closer look at this to bring in steadiness to balance my high-equity exposure.

Thanks for your insights—making informed decisions is the priority here, and your guidance helps set that direction!

1 Like

Update in the Portfolio

I have made significant update to improve diversity of my portfolio. I have started deploying more in US Markets as I felt in Indian markets I did not had valuation comfort and my stock picking in Indian market is not so good. I pretty much buy the large caps but gave absurd valuation at the time of buying.

Current Portfolio

- Retirement Investment (USA/CA): 27.59% (Majorly US ETF - S&p 500)

- Stock Investment – India: 15.78% (Aavas Finance, Indigo Paints, HDFC, Kotak, Olatech, HUl, Asian and other companies)

- Real Estate (Residential) – India: 14.79% (Paid 50% of the Home, mostly going to exit the investment)

- Canada TFSA: 13.12% (Google, UNH, ASML, Amazon)

- Liquid Cash (Savings + Emergency): 12.33% (USD Hi Yield Savings Account) - (Expecting some expenses)

- Canada RRSP: 11.51% (UNH, Google)

- FSHA: 1.44% (Novo Nordisk - Just started Investing)

- Friend Help (No Interest): 3.45% - (Not going to get back for sure now)

Now due to surge in US portfolio Blended XIRR of the managed Net worth is +35.84% and absolute return is 23.32%, can not include Retirement Investment (USA/CA) in calculations but that is around 19% XIRR.

Now let’s look into top holding across portfolio in pure equity. (No retirement and No RE)

- UNH sits at 20.6% of all the investments

- GOOGL sits at 15.7% of all the investments

- CASH - USD sits at 20% of all the investments

- ASML sits at 3.2% of all the investments

- AMAZON sits at 2.2% of all the investments (Increasing Position)

- Novo Nordisk sits at 2.5% of all the investments (Aggressively Increasing Position)

- Aavas Financiers Ltd sits at 5.8%

- Indigo paints sits at 3.8%

- Hdfc Bank + Kotak Mahindra Bank sits at 7%

- Olatech Solution sits at 1.7%

- Hul - 1.6%

- Asian Paints - 1.4%

- HDFC Life - 1.2%

- SG Finserv - 1.3%

- Muthoot Microfin + Fussion MicroFin - 2%

- Sub 1% - Indegene, Fine Organics, NMDC, Archeam, Concord, SG Mart, Berger Painst, Paushak, Clean Science, Rajesh Exports

So the Indian Portfolio is not performing well. But the USA stocks are through the roof. Googl is over 100% XIRR and UNH is over 150% XIRR which is lifting whole portfolio but I expect Indian stocks to do good in next 2 years, the one which I have NBFC and Finance Companies.

I’m also open for more sectors such as manufactoring or Pharma. keeping my eyes on shaily engineering plastics ltd, ran up a lot but with GLP-1 I think they could do wonders.

Would love some constructive feedback!

Most of my portfolio is stable, I have started booking profits in some pockets but more or less indian stock portfolio is still lacking and in pain. I might completely exit my indian positions soon.

Current Portfolio

-

USA / Core Investments: 54.76%

(Majorly US ETFs – S&P 500 and US equities) -

Stock Investment – India: 16.74%

(Aavas Finance, Indigo Paints, HDFC, Olatech, and other companies)

(Exited Kotak Bank, HUL, Asian Paints, and Berger Paints) -

Canada RRSP: 9.91%

(UNH, Adobe), Also hold options on UNH and ADOBE, LEAPS 2028 -

Canada TFSA: 6.38%

(UNH, Amazon) -

Cash / Liquid (Savings + Emergency): 9.22%

(USD High Yield Savings Account, Dry powder for deployment) -

FHSA: 2.70%

(Novo Nordisk – just started investing)India Mutual Funds: 0.29%

Friend Help (No Interest): Already written off – not included in portfolio allocation

Now due to surge in US portfolio Blended XIRR of the managed Net worth is +35.84% and absolute return is 23.32%, can not include Retirement Investment (USA/CA) in calculations but that is around 19% XIRR.

Now let’s look into top holding across portfolio in pure equity. (No retirement and No RE)

-

UNH sits at 22.5% of all the investments (Excluding LEAPS)

-

CASH - USD sits at 27.5% of all the investment

-

AMAZON sits at 2.2% of all the investments

-

Novo Nordisk sits at 10% of all the investments

-

ADOBE sits at 2.9% of all Investments (Will increase allocation to 5%)

-

CSU sits at 5% of all Investments (Will increase allocation to 10%)

-

Aavas Financiers Ltd sits at 8%

-

Indigo paints sits at 5%

-

Olatech Solution sits at 1.7%

-

SG Finserv - 1.3%

-

Muthoot Microfin + Fussion MicroFin - 2%

-

Sub 1% - Indegene, Fine Organics, NMDC, Archeam, Concord, SG Mart, Berger Painst, Paushak, Clean Science, Rajesh Exports

So the Indian Portfolio is not performing well. I booked 100% gains in GOOGL as it is now 2.5 PEG and Expensive for me to hold. UNH and NOVO had ran a lot but due to latest results they are back at my average buying price

I have started some positions in SaaS after the brutal fall in the markets. CSU and ADOBE is my choice. I expect them to reach back to 52 W Highs in next 1/2 years. I brought the stocks and for the first time I have started using options to gain exposure. For both the stock (UNH and ADOBE) I have brought call option for January 2028 with strike of 310. I expect the UNH over 450 and ADOBE over 500 by that time.

Would love some constructive feedback!