Yes indeed.

What was your reason to sell?

1 Like

The hypothesis was to invest for re-rating due to sheer undervaluation and improving fundamentals. As it played out in very short time, giving me far more than my own expectation and with this 1) initial hypothesis no longer applicable 2) unfavorable RR and 3) better alternatives, I shifted my capital elsewhere.

It’s just that in this counter my entry/exit worked to perfection. There are at least 2 examples where in I’ve lost 100x or so in profit and still counting due to premature exits. But the lessons learned stays and reflections like this on the past helps.

Hope this helps.

6 Likes

2 Likes

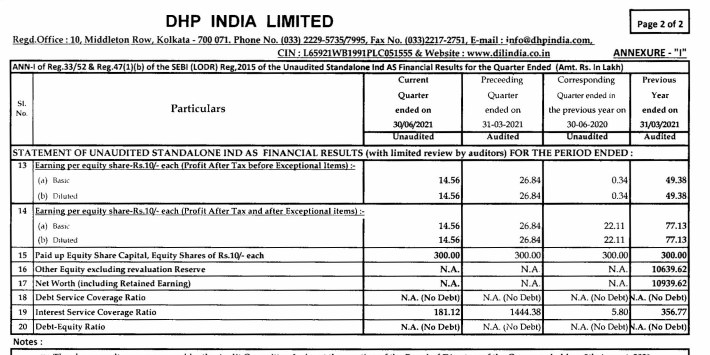

4 cr operating profit is a good achievement considering the prevailing environment in Q1.

8 cr MF gain is a seasonal gift which will not be sustainable in coming quarters.

12% fall in price today is a needless knee jerk. Can be a good point for accumulation. Must scale back to 750+ levels in August if market remains stable.

3 Likes

I think the expectations were bit high with huge Q4 (despite poor cash flows) & the raw inventory built up indicated big Q1 as well. But from the notes, it seems the lock down affected them severely. Lack of communication from management always keeps the investors on edge (mini correction in mid & small cap indices adding fuel to fire). Opting for physical format AGM indicates management’s lack of interest in providing investors proper avenue to interact with them. Since, nodody clearly knows the management thinking on putting cash to any good use, not many would like/dare to take that into valuation consideration.

Discl: Invested (still a novice investor; plz don’t take sell or buy decision based on my writeup)

2 Likes

The latest annual report mentions company is undergoing capacity expansion: https://www.bseindia.com/bseplus/AnnualReport/531306/68591531306.pdf

C.FOREIGN EXCHANGE EARNINGS AND OUTGO :

(a) Activity relating to export, initiatives taken to increase exports; development of .new

export markets for products; and export plans :

The net exports of the Company has been increased from Rs. 4785.49 lacs to Rs. 6199.42 lacs

during the year. The Company is expanding its production capacity to emerge as a leading exporter

of our product. The Company is ISO 900 I : 2008 certified.

How much is this expansion and what is the estimated completion time?

You can see same statement in its past annual reports. This may be a reference to a gradual increase in production capacity over years as is evident from a gradual increase in its turnover over.

However they have not spent heavily on capex for many years, but invested all their profits in Mutual Funds which on the hindsight seems to have rewarded the company well crossing over 100 cr.

With a PE of less than 9 and over 50% of market cap in cash, the valuations are dirt cheap. Tomorrow’s results can trigger the spark for a much needed rerating. Fingers crossed!

5 Likes

dhp_quarterly.pdf (4.0 MB)

Good sales numbers in this quarter. MF investments also doing well. Increase in cost of cost materials, may be due to higher commodity prices.

Stellar results. It’s a valvonic eruption that is looking to be unfolding here that can take the stock to levels no one would have imagined.

Apart from 11 cr operating profits and 3.9 cr mutual fund gains, a major silver lining is 7 cr capex spend in this quarter which is 3/4th of its net book value of Mar.

If there is a trigger for its long overdue rerating, it will be today’s results.

Disc: Invested for more than a decade!

5 Likes

what is impact of this will this can happen in bse as well ?

Most companies have already delisted from all the exchanges other than BSE & NSE. There will be no impact on current BSE listing.

1 Like

Hi Lakshmi Narasimhan,

Congrats for being invested for 10 yrs in DHP & making great gains on your investment. I have invested in DHP last year, which constitutes about 5% of my PF. Despite the concerns of cash accumulation & lack of communication, the valuations & Dr. Vijay Malik’s presence as a shareholder made me pull the trigger. Can you share your opinion on the cash accumulation part? Why is the management accumulating cash like crazy? If you have attended last AGM , can you share what transpired there briefly? Thanks in advance.

2 Likes

Hi Srikan, this was a stock I entered in 2006 to be precise after some bit of my own study those days and been gradually adding seeing their results every quarter. I never regretted my decision to stay invested although the stock remained outright laggard until a break out in 2014.

The management team from my view point remained extremely honest and working on their strengths and generally risk averse. They have gained extremely good traction with their customer base across globe which would not have been possible without meeting tough quality and delivery standards.

Maintaining 20 to 30% operating margins over the years despite heavy fluctuations in their input cost for copper and brass are a test of their competitive edge with their customer base.

Coming to the company’s decision to park surplus funds in Mutual Funds, I was not liking it either initially. But when you look back, a four fold growth in business in less than 10 years without any significant capex and maintaining zero debt is a proof that company has a moat when it comes to delivering quality products and maintaining high customer satisfaction.

As a rough calculation, net profits generated from 2015 to 2021 are ~ 70 Cr growing nearly 4 fold.

Current market value of their mutual funds investments alone must be over 100 Cr which is more than the profits generated from the business.

Management left cash in the hands of safe fund managers to do what they are good at in managing their cash, while they concentrated in consolidating and growing their core business.

In Q2-FY22, after a long time we are witnessing an aggressive capex spend from the company entirely funded from internal cash pool. There can be more such spends going forward as well which will only translate to far better results.

Having 100 Cr cash in the hands of a very honest and efficient management team controlling a business that has a great potential for growth in future, I am not really worried as an investor as the broader market continue to remains bullish in the long run.

At today’s market valuation of 212 cr, and ~ 8 PE, 100 Cr cash is a bonus. Either they reinvest this in their business, or distribute as dividend or let it grow in mutual funds, its a win-win situation.

Having said, I constantly re-asses these conditions with every quarter result published and I have not had any discomfort yet on their performance in comparison with the broader market.

Floating stock in the market can be just around 5 lacs and with constantly good delivery volumes, chances of the price being manipulated are extremely less.

Growth potential in the stock far outweighs the liquidity risk and hence any moderate exposure can be rewarding in the long run.

30 Likes

Thanks for sharing your views.

I am also invested in the business since 2013. My concern is : with almost 100 cr in MF. What is the probable utilisation in future. Is it coming to shareholders or is the company employing it somewhere more useful.

Are we seeing another ITC (just a thought), where business generates excess cash & management doesnt know what to do with it.

Though is a happy problem (situation) to have.

Disc : Invested for long term.

1 Like

This company is little over 2 decades old at best and have a long way to go before we draw parallels with behemoths like ITC.

Cash cannot be the only resource a company of this type will need for an all out expansion. From their past track records, I can see the management is taking the right steps in building their customer base, developing their manpower, improving product qualities and maintaining production machineries for a sustainable growth in an industry that is still fairly at a nascent stage in India.

The company’s annual reports are as much an exhibit of managements integrity in handling surplus cash, as much as their robust performance has been over the years. I don’t assume they will start spending them all for the benefit of promoters or employees, although they have all means to do so.

I am glad to see 7 cr capex spending in this quarter which is still a fraction of their cash reserve. These baby steps are strong indicators of more pervasive growth that will be more sustainable for years to come.

5 Likes

Really appreciate your views @Lakshmi_Narasimhan_B

I have a couple of questions which I am hoping you can answer.

On the subject of the Mutual Fund investments — even assuming the act of investing in Mutual Funds itself is alright — what’s your opinion on the fact that they’re not going the Direct route and instead incurring Transaction / Brokerage charges?

A while ago, someone had calculated the savings should they shift to Direct plans and I believe it was about Rs. 60 Lakhs.

Maybe a trivial amount, but when you consider the drag of Transaction costs over several years (Assuming they continue investing in Mutual Funds), surely it’s much more beneficial to go Direct.

Was this ever discussed with the management in any of the Annual General Meetings?

This also brings me to my second question. DHP India’s Annual Report feels like a template at times and the AGMs are always physical (Even when COVID19 was widespread, they chose not to conduct it online). Was there ever a suggestion to have other forms of Shareholder communication — Concalls, Investor Presentations and so on?

4 Likes

I spoke to the CFO a few months ago. The fund investments are carried out by the MD himself. They have taken the feedback and will incorporate in the fresh investments. I hope this clarifies.

5 Likes

Hi @dineshssairam, you do have a point on saving brokerage cost through Direct plans. The other boarder’s response might have answered it though.

As regards conducting virtual AGMs, Con-calls, Investor presentations, I feel given the highly concentrated shareholding and with its micro cap tag, the management might have chosen to maintain a low profile and let their results do the talking. Yes, the annual report seems more like a template, but the numbers are numbers at the end and we have to admit they have done their job well.

I have not felt the need to attend any of their AGMs till date, but never missed to write to express my gratitude and wishes to the team every time they came out with good numbers.

As and when their shareholder base widens, we can expect to see these modes of communication taken up seriously.

Of late, I am getting more anxious about their increasing exposure in Mutual Funds which can crack down anytime without their notice. Its high time the company diversify their investments and move a good part of their cash to safe haven assets like bullions/ETFs and debt funds.

I personally like gold and silver at the current prices and given a 30 year record inflation in US, its just a matter of time prices for these metals to hit the roof.

7 Likes

Holding company selling shares continuously in the open market.

Not sure if it could be a red flag. Till now only about 1% diluted, however this can increase further.(Updated the figure due to more selling by the promoters)

This is very disturbing indeed. Nearly 1% offloaded since June this year. Looks like a desperate sale before Q3 end. Stock been consolidating for a quite sometime despite posting good results.

Chances of price recovery before results seems unlikely. If Dec results are not encouraging, price can be hammered deep down.

3 Likes