@goyal_neelesh Sorry about this naivety, but I dont understand what you mean. Can you please elaborate about promoter’s intention?

Promoters may or may not participate in a buy back. When they do then they themselves also stand to benefit as they are mostly the largest shareholders of a company. When Dhanuka announced the buyback they already declared the promoter’s intention to particpate in the buy back. The screenshot above just shows how many shares they offloaded towards the buyback.

2 Likes

Any industry expert here who can elaborate on this?

1 Like

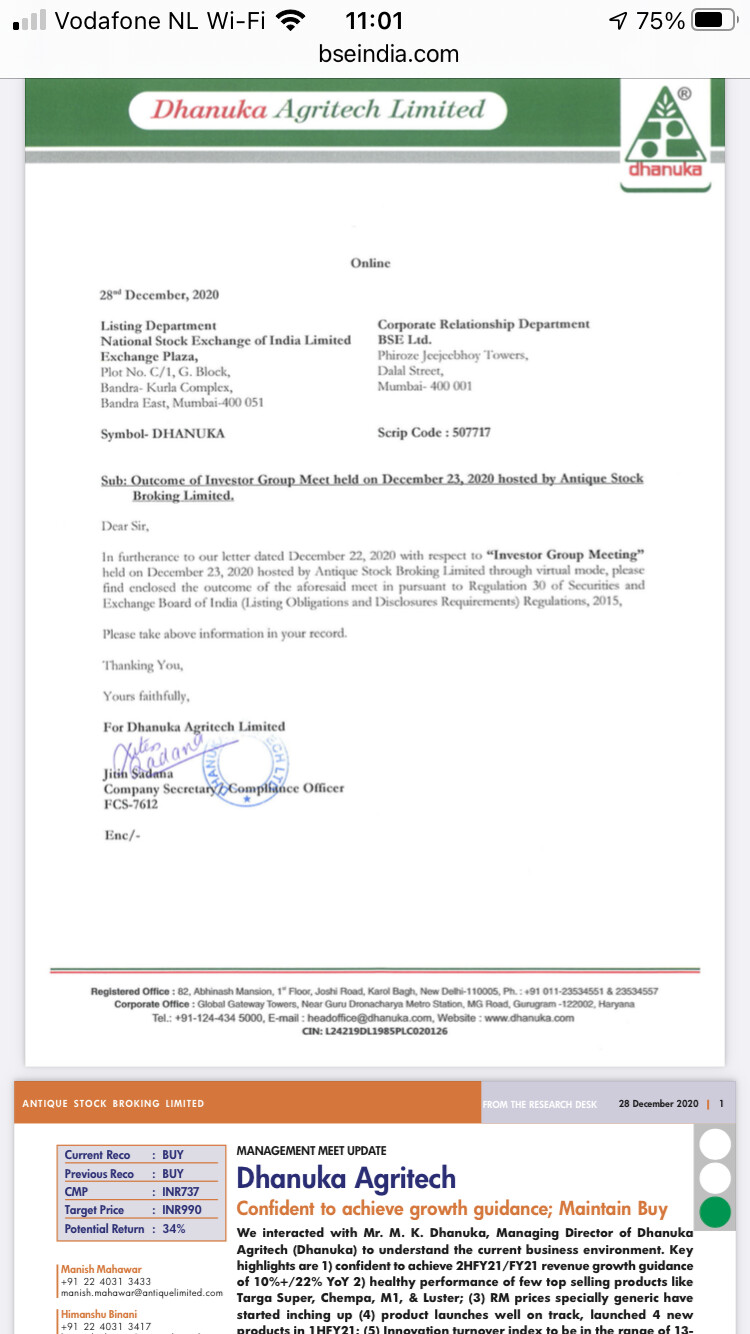

I find it very disappointing that today in the garb of ‘Outcome of the meeting with investor group’ the company shared an analyst report with a high price target with the exchanges. Would they have done it if the analyst assigned a price target lower than the current price? It is not a management’s job to share analyst reports on basis of their discussions.

6 Likes

Hope there is no “non-public” information the broker report

3da021da-4e04-41e5-8883-5c9d6ef6a2e1.pdf (881.3 KB)

Results are on expected lines.

Reported total income of Rs.305.04 crores during the period ended December 31, 2020 as compared to Rs.279.32 crores during the period ended December 31, 2019.

The net profit of Rs.40.04 crores for the period ended December 31, 2020 as against net profit of Rs.27.67 crores for the period ended December 31, 2019

Disc: invested

2 Likes

Promoter holding too has increased from 75 to 75.18…stock has been hovering around same range for past six months…

2 Likes

Stock broken to ATH. Also the results have come today and are quite good.

THe growth is more than 50% as compared to last year. If they can maintain even half of this growth, then the stock should do well

Nikhil

2 Likes

Conference call takeaways

Dahej capex plans. The management is looking to invest Rs3 bn in Dahej facility over FY2022-24. This investment will be first on setting up active ingredients (AIs) for pyrethroid family of insecticides. Post that, the management will also put new capacities for generic herbicide products. Dhanuka would use nearly 50% of the capacities for internal consumption while rest of the capacities would be used for selling to third parties.

The management is also exploring opportunities with Japanese players for setting up contract manufacturing in this facility. However, this would only be possible after Dhanuka builds up the Dahej facility and clients are able to inspect the compliance standards of the facility. The management expects phase 1 of the facility to be completed by FY2022-end and generate Rs2 bn in revenues in FY2023. By 2026, the management expects this facility to be fully utilized and generate revenues of Rs3.5 bn on an investment of Rs3 bn (implies 1.2X asset turn) and 12-15% EBITDA margins. Dhanuka will invest Rs800-900 mn in FY2021, Rs1,300 mn in FY2022 and Rs800 mn on Dahej project in FY2023. FY2022 guidance.

The management remains optimistic to drive early double-digit revenue growth despite stiff FY2021 base which registered 24% revenue growth. 1QFY22 is likely to register a decline in sales growth given a stiff base. 1QFY21 had benefited from postponement of demand from 4QFY20 and advancement of demand from 2QFY21. FY2021 growth was largely led by volumes with pricing growth of only 1%.

The management expects FY2022 growth to be also driven by volumes. Expectations of better acreages on pulses/oilseeds which have higher revenue salience for Dhanuka drive the management optimism. Better ground water levels, higher commodity prices and better cash levels from relatively better FY2020 and FY2021 agri years should support better industry growth rates.

In-licensing share. Dhanuka drives 40% of revenue share from in-licensed products. This has gone up by 200-300 bps over past few years. The management expects this to marginally improve over the next 1-2 years. It is launching two 9(3) molecules this year and another two 9(3) molecules next year.

6 Likes

1 Like

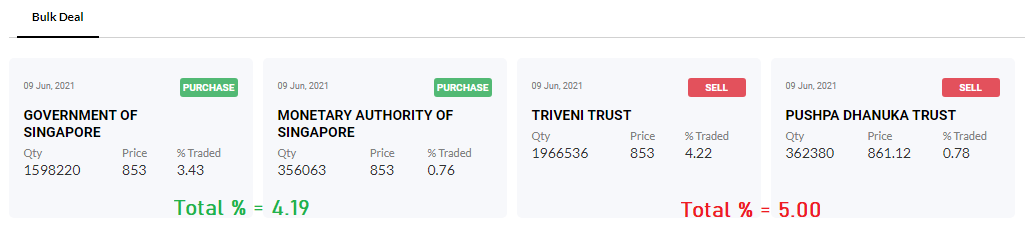

Promoters sold 5% stake. Dont Know the reason D4935897_6DAA_4E45_8601_129F65D8E2BC_171329.pdf (1.5 MB)

Pls check this recent management interaction in CNBC. Discussion made regarding stake sale also.

Hope it helps

2 Likes

1 Like

Dhanuka Agri Q1 concall, latest management interview highlights -

Revenues- 369 vs 392 cr

Gross Margins @ 32.8 vs 32.7 pc

EBITDA- 44 vs 51 cr, margins @ 11.8 vs 13.1 pc

PAT- 33 vs 49 cr

Q2 is their biggest Qtr

Q1 was affected by delayed monsoon till Mid June

Demand scenario and product off take in July was good

Aug again was subdued due deficient rains but first 10 days of Sep have been buoyant (source: latest management interview on 13 Sep)

New products launched -

Implode - Maize herbicide

Mesotrax - Maize, Sugarcane herbicide

Defend - Rice Insecticide

To start commercial production from Dahej plant (company is making Technicals or AIs here) in Q2

Initially going to produce - Lamba Cyhalothrin and Bifenthin (both - pyrethroid class insecticides)

Revenue Mix in Q1-

Insecticides-27 pc

Fungicides-10 pc

Herbicides-54 pc

Others-9 pc

Herbicides have structural tailwinds as the cost of manual labour is increasing

Company guiding for 150-200 bps improvement in EBITDA margins for entire FY 24 with double digit topline growth

Besides the new Dahej Plant (for Technicals), company largely makes formulations only

Have a distribution network of 41 warehouses, 6500 distributors, 80000 retailers

Sells to aprox 1 cr farmers

Has international collaboration with 10 global MNCs to source products, technology

Has set up a new R&D centre in Haryana for faster development of products

Did a buyback of 85 cr LY and distributed Rs 2/share as dividend

Has introduced 06 new biologic formulation in India in Q1

Intend to export technicals from Dahej plant after meeting the captive demand

Indian agrochemical can potentially be a great growth story going forward (India has already overtaken US, Europe in Exports. Is only behind China now)

Inventory at Q1 end - 395 cr. Working capital days - 152

Channel inventory eased out in July after a build up in June

Rising agri commodity prices in Q2 is another positive for the Industry

Expect 50 cr revenues from the new Dahej facility in FY 24. The double digit topline growth guidance does not include this

Q1’s volume de-growth was 3.5 pc

The product off take in July was robust

Expect Dahej plant’s revenues to go upto 100 cr by end of FY 25

Prices of Chinese technicals seeing a gradual rise in Q2 ( company procures from both China and India )

Disc : have a tracking position

Latest update by Dhanuka Management in recent interview:

Negatives :

-India has witnessed a lowest rainfall in Aug’23 and hence the demand for products was very weak vs Jul’23.

-Management has said that topline will be 10% less than the projected targets.

Positives :

-Management has said that the company may report lower double digit growth (10-12%) in topline on y-o-y basis; although dry season reported in Aug’23 (Management expectation was higher double digit growth i.e. 16-18%)

-High cost inventory is fully absorbed and now the company is procuring raw material at lower prices. Also, company has increased prices of products in Aug and will continue till Sep’23

-

Improvement in gross margin and operating margins by 200 bps and 100 bps respectively.

-

New CAPEX plant at Dahej will generate Rs 50 cr in current year and 100cr next year. They are looking for a tie up with Japanese companies for production of technical molecules which will be announced before Mar’24.

1 Like

any take on dhanuka after latest result?

Fixed asset base has almost doubled. good latest quarterly result.

Dhanuka Agritech Q2 concall highlights -

Sales - 618 vs 543 cr

Gross Margins @ 40.3 vs 34.1 pc - Huge Jump !!!

EBITDA - 142 vs 98 cr, Margins @ 22.9 vs 18 pc !!!

PAT - 102 vs 73 cr

Guidance for FY 24 - double digit revenue growth over 1700 cr ( last Yr’s revenues ), EBITDA margins for full FY at around 17 pc

Company seeing excellent demand for its new product - DECIDE (insecticide) introduced LY. Fuelled by a few more insecticide introductions, growth in Q2 was robust

Launched 02 new innovative products in Q2 -

TIZOM - Herbicide for sugarcane crop - in collaboration with Nissan Chemicals Japan

SEMACIA - broad spectrum insecticide having excellent efficacy over a range of crops

Product wise sales break up for Q2 -

Insecticides - 44 pc

Fungicides - 18 pc

Herbicides - 25 pc

Others - 13 pc

Geography wise sales break up for Q2 -

North - 24 pc

South - 31 pc

East - 11 pc

West - 34 pc

Company’s unique strengths -

Asset light model with minimal investments in Fixed assets

40 warehouses, 7000 distributors, 80000 retailers covering over 1 cr + farmers

90+ products across agrochemicals and plant growth regulators

Tech Tie-ups with leading global companies from US, Japan, EU

Robust pipeline - focus on launching margin accretive 9(3) products. To launch 8 new products in next 2 yrs

Volume growth in H1, Q2 @ 10 and 20 pc respectively

Gross margin expansion in Q2 happened because of 2 factors - better product mix, phasing out of high cost inventory

Insecticide - DECIDE did very well in Q2. It’s a versatile insecticide. It’s a 9(3) registration product used across a variety of vegetable crops ( like chillies, brinjal, tomatoes, okra etc ) against the sucking pests. Hence its Mkt potential is also big

Dahej Technicals plant got commissioned in Q2. Nil revenues in Q2. Should contribute from Q3 onwards

DEFEND - a paddy crop herbicide should do well in H2

Plus there is upcoming Chilli season in South India - which is again a good opportunity

SEMACIA, TIZOM also have good sales potential in H2

In talks / discussions with a number of international partners for CDMO business. Things should materialise sometime in future

For DECIDE and TIZOM - Dhanuka is the exclusive local partner of the innovator

New products / Innovative products - introduced by the company in last 3 yrs are doing exceedingly well. Plus the margins in these products are also better

Capacity at the company’s three formulations plant is not a constraint. Company can almost double its revenues from the existing capacities

Disc: hold a tracking position, biased, not SEBI registered

4 Likes