The adjustment in Cash Flow Statement simply seems to be an accounting adjustment. For instance, this is what LIC HF reported in its P&L (I’m showing the Notes to the specific item):

A very similar amount has been adjusted in the Cash Flow Statements.

I’m not sure about the accounting implications here, but this looks like a simple case of representation. We know for a fact that for BFSI firms, whatever Net Profit they earn are almost always equal to the actual profits they earned (Except some minor adjustments). I think raising a concern in this area is just trying to look for a needle in a haystack, except there’s no needle.

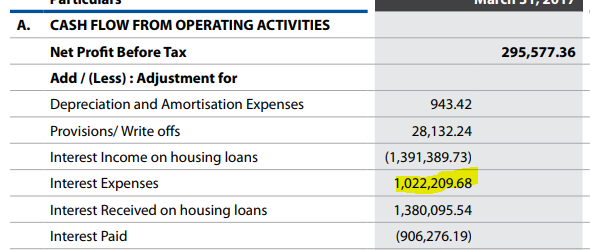

@phreakv6, its just a reclass issue to the best of my knowledge. DHFL makes the adjustment of interest expense and interest actually paid in the working capital changes segment. Whereas Indiabulls and Gruh prefer to first add back interest expense and then show the actual amount paid. While the latter 2 show this more clearly, there is nothing wrong in this presentation I believe.

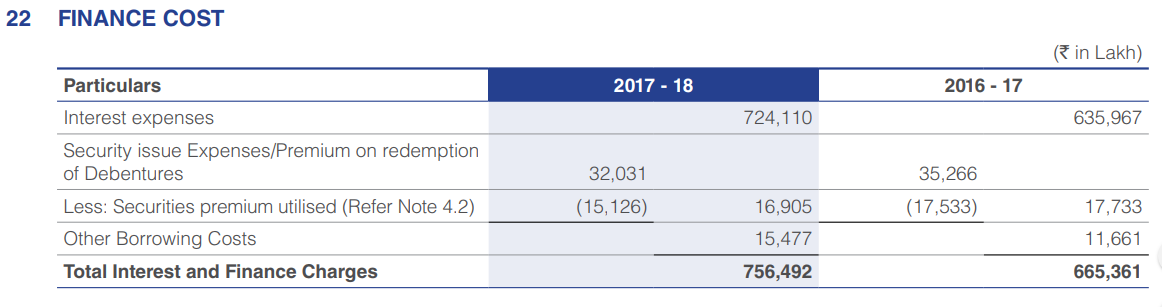

DHFL and PNBH both use indirect method of CFS as per notes. The reason for cost of funds being over the place is because of zero coupon bonds which is something both DHFL and PNBH use and it’s not just limited to DHFL/PNBH. Securities premium reserve can be utilized for paying premium on zero coupon bond.

Zero coupon bond pay no coupon until maturity and hence can be riskier to hold. DSP may have sold zero coupon bonds.

“Cash flows are reported using the indirect method set out in Accounting Standard on ‘Cash Flow Statement’ (AS 3).The cash flows from operating, investing and financing

activities of the Company are segregated based on the available information.”

In the investor presentation, 7 months interest outgo is 2529. On an annualised figure this comes to 4335 intrest outgo.

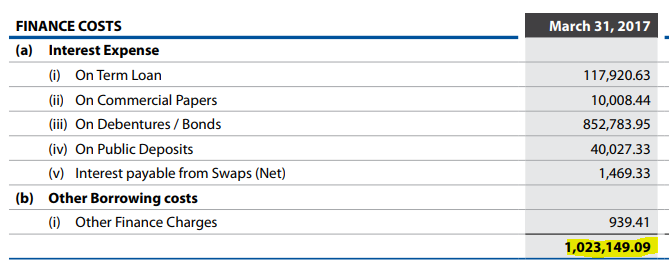

Its not possible to make out actual interest outgo because of adoption of indirect method of CFS.

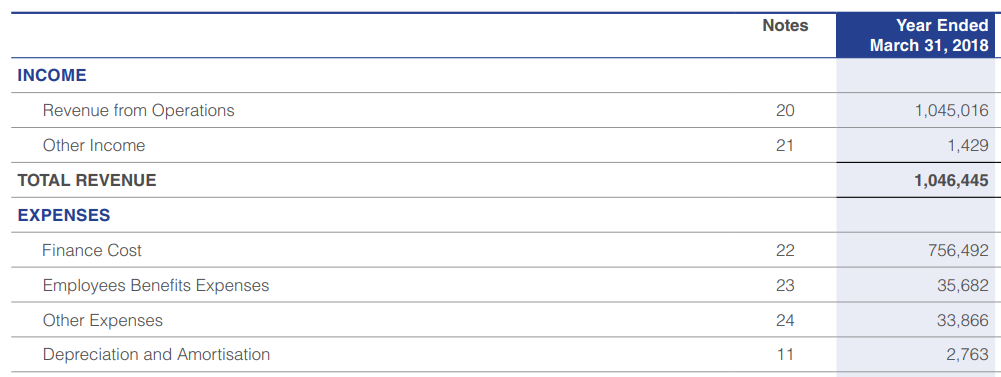

Finance costs were 7564 Crores as per FY 2017-18 and Total debt was 94,244 crores as on March 31,18

This works out to be 4.5% cash outgo on borrowings. On an unrelated note auditor of DHFL is Deloitte. For some people it matters and for some it doesn’t.

my understanding is that it interest is your cost of goods then it’s an operational expense and not a finance expense on cash flow

I don’t know why the others like Gruh and indiabulls show it differently

Like like if you were to buy a car, it’s a fixed asset but if you were to buy it as a car agent then it’s current asset/inventory

A good article highlighting that When you are hit with something unexpected and extreme - you tend to forget previously learned behaviors. Pertinent to the current ongoing posts.

On a more relevant note - as I understand DHFL has an average roe of 13-14%. The long term goi bond yields are hovering around 8.3% or thereabouts and there is a rising interest rate scenario. Under these conditions , dhfl equity should be a prime candidate to be priced at somewhere around book value regardless of what happened. The natural gravitational laws of valuation are a reality for good, great or mediocre businesses.

I guess the question is, is the CP at 12% for DHFL a sustainable level? It is AAA rated after all. How can we be confident what the borrowing rate of the company will be after 1 month?

11% yeild was in secondary market which is typically illiquid and on which company has no control. Even tax-free bonds from NHAI are available in 7.5% region (effectively a pre tax yeild of 10% ! (From near sovereign institution). These are exceptional times due to acute fear in financial market and as benjamin graham says in intelligent investor, buy when there is acute fear in the street. Good prices and good news don’t come together .

Hi Sarangg,

Could you please elaborate how you arrived at the conclusion of fair value of DHFL is ~1-1.2x based on CP interest rate and ROE. What is the relation between the two?

This is not the right way to compare - first of all for shareholders the relevant number is how the company has increased book value per share over the last many years. Now I haven’t done the analysis by myself - but the ratestar.in numbers show that book value per share has been compounded at 20.5% for DHFL over the last 11 years → this is the relevant number for the investor, not some perfunctory glance on the RoE’s. Interestingly, the first page of all annual reports of Berkshire Hathaway - compares the growth in book value per share over the last 40-50 years and Warren Buffett calls this as the prime factor to gauge his performance over the long term.

So if I take the number of ~8% GoI yields long term - a person holding 100 Rs of book value of DHFL stock 11 years back would now have Rs 780 book value of DHFL stock now (worth atleast 780 rs as per your analysis or 1560 rs till the last week by the all knowing market) while the person holding 8% GoI stock worth 100 rs of book value would have 233 Rs worth of book value GoI stock (worth 233 rs only) - a difference of 3.3 times in just 11 years or a difference of 6.6 times in 11 years minus one last week.

Given this vast difference in past long term performance - should someone today value 100 Rs book value of GoI bonds and 100 Rs book value of DHFL stock at the same multiple of 1 !![One should but only if one believes that the management has been successful in fudging the real economic numbers for the last 11 years atleast and truth has been evergreened. Not impossible but less likely.]

[I have not yet gotten into the tax advantages of holding a stock over 11 years vs holding debt which will further magnify the difference. Another big difference not captured here is most debt is anyways not zero-coupon unlike a stock where most earnings are withheld for growth and saved from income tax or DDT.]

Disclosure - Not invested, invested and exited several times in the past.

PS - the premise of my post rests upon the accuracy of the data used which I haven’t verified from primary source

Yes, the growth in book value is the relevant metric. However, it cannot exceed the ROE unless there is consistent equity dilution as is the case with financial institutions.

HFC’s have had a great run in the past due to a benign interest rate scenario coupled with rising home prices in an unregulated real estate sector which was quick to increase inventory.

The position has now reversed. We now have a rising interest rate scenario, pricing pressure on developers, tough real estate regulations and developers who are now more concerned with collections rather than volume.

Under these circumstances, margins for housing finance cos are going to be curtailed and they will also find it difficult to raise finance. Exacerbating this situation is the entry of many other players in this space.

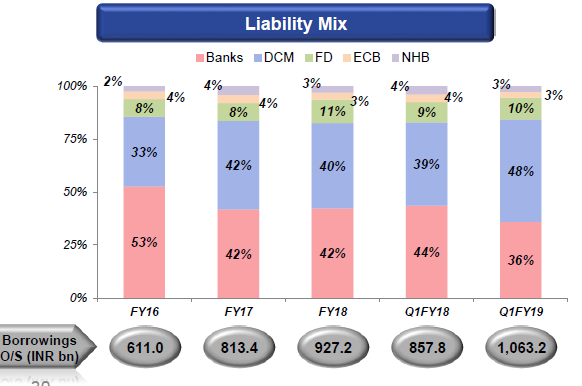

I think 60% of the borrowing mix of DHFL is from banks. Clearly, Interest rates are going to put further pressure here.

Under these circumstances, the typical ROE of a HFC going forward should be much lesser than what has been in the past. 13% - 15% should be a good guess going forward.

The long term government bond yield is a risk free investment and an investment in the equity of an HFC i should assume carries with it significantly more risk and it stands to reason that a greater margin of safety should be demanded if one is certain about the long term earnings potential of the said HFC.

Net Net in my view and given the changed market scenario, the average ROE of HFCs will contract to 15% going forward and maybe DHFLs will contract even further to settle at 13% or so.

1.5 times book value should be a fair valuation for DHFL in my view and ofc you would also want a deep MOS on that given that the sector may not be as attractive going forward like it was in the past.

For my understanding can you please explain how do we know we are in rising interest rate scenario. Because the interest rates increased in last 1 year does it mean it will continue in future also. Can’t interest rate be dropped if inflation decreases?

I am not trying to contradict you. Just want to learn about interest rate cycle.

Does anyone have a any pointers as how did HFC’s performed when at the peak interest rate cycle…If i am not wrong maybe 2011-12 period where rates are high…so will the HFC continue to under perform in the near term?

Percentage bank borrowing as per Aug 2018 investor ppt is 36% and declining

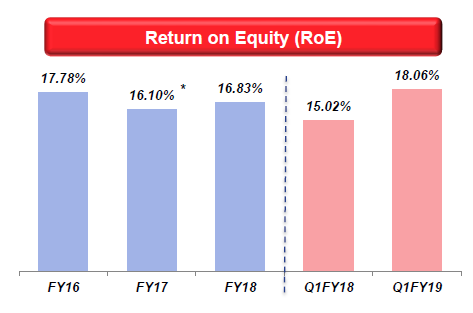

Also, I think the RoE of DHFL is slightly better than what has been stated in these posts, around 17% in FY18 as per Aug PPT

The concern about possibility margin contraction in a rising interest rate scenario is valid, and in fact this very concern was raised by one VP member in the analyst conference call last week. While management assured that the margins will be by and large protected, we have wait and see I guess. Looking back, in 2011 when there was steep rise in rates, company did fairly well if I am not mistaken.

Based on information available in public domain, I personally feel that DHFL has been unfairly punished, and the stock is currently available cheap.

DHFL has 99.70% of its loans on a floating rate basis. So margins will stay intact. If at all RBI increases rates a lot, it’s the revenues which will get affected, not the margins (Which is fine, by the way. It’s business as usual).

In April 2012 , the net worth was around 2000 crores and company was trading at price of 120-130 (4100 crores market cap) , i.e. two times the book values , today its trading on book value. Seems V cheap if we compare from 2011-12 when interest rates were high. I don’t track this company and started looking at this since last week. Even if interest rates goes up consecutively , what is the worst case scenario ? How low it can trade to price to book value ? I can see margin of safety but not getting courage ( already burnt hands in PCJ few months back).