Some thoughts on Deepak Nitrite. No recommendation to buy or sell. Don’t hold any position.

Early years- unviable business

• Founded in 1970 as a chemical trading company it gradually started manufacturing chemicals such as Sodium Nitrite and inorganic salts. As of 1997 (first AR available), it made a loss of 2.1cr, had equity of 43cr and around 80cr in debt.

• The early years from 1997- 2008 were a struggle. PAT fluctuated between 5cr-10cr, debt to equity ratio was more than 1 and ROE was in single digits they could have created more value by simply putting their money in an FD. The key reasons were volatile RM prices which they could not pass on, severe competition from China which had large scale plants and government support and generally weak demand in the Indian economy. Even the bull market years of 2003-2007 saw patchy profits due to pricing pressure.

• Conclusion- their business model of small-scale commodity chemical manufacturing was destroying capital and simply not viable in a world where India had liberalized and was freely allowing imports. The only reason they soldiered on was likely because it was a family business.

China reduces capacity- windfall gains

• Suddenly in 2009 the company reported a 6X increase in profits! The reason was China’s closure of plants to combat pollution. This clearly shows the impact of Chinese competition on their profitability, not even the global financial crisis could dent this.

• From 2010 onward the company became more confident and started increasing capex which grew from 166 cr in 2010 to 560 cr in 2017. New products such as OBA ( optical brightening agent) were introduced. While profitability did improve in these years to reach around 55-80cr the ROE was still poor at low teen levels.

Conclusion- Patience pays! China’s capacity reduction gave a new lease of life to Deepak.

Products and return ratios

The company has 3 main segments (other than the newly incorporated Phenolics subsidiary)

• Basic chemicals- they contribute around 50% of revenues and include commodity chemicals like Sodium Nitrite (around 15% of sales) and petrochemicals such as ortho and nitro toluene and fuel additives. The margins on these chemicals are crude oil driven which the company has no control over. Unlike Aarti Industries it does not control its EBITDA per ton. Its market share in many of these chemicals is already above 70-80% signifying saturation.

• Fine and specialty chemicals- this includes chemicals mainly used in dyestuffs and agro chemicals such as Xylidines and oximes. They are also petrochemicals (derivatives of aromatics such as Xylene) with prices dependent on crude oil dynamics. The market size for such chemicals is not much.

• Performance products- includes vertically integrated operations from toluene---- PNT------ DASDA----- OBA (optical brightening agent). OBA the main product is used as a brightening agent in textiles and paper. Deepak already claims a 75% share of this product hence further gains can only come from price increases and general market growth. China based Tsaker chemicals the largest global producer of DASDA and OBA is training its sights on the Indian market after having won an anti-dumping suit in early 2019.

• The overall ROEs of commodity chemical companies like Deepak are in the 10-15% range owing to low FA turnover (2.5X-3X) and relatively low margins of 10-15%. A few quarters or years of supply driven gains can optically increase ROEs but this needs to be set off against losses which will surely follow the wind fall years.

• Deepak’s ROEs even after 2009 driven by Chinese supply cuts have been in 10-12% range due to continuous high capex (more than tripled from fy 12-fy 17). FY 19 and FY 20 ROEs may be higher due to attractive spreads in phenol but this cannot be extrapolated.

Conclusion- Deepak’s product portfolio is rather unexciting and mostly maxed out in terms of volume growth given high market shares. Recent profit figures have been due to China driven price increases which cannot continue for ever. The diversity of products is also low with most of them dependent on crude oil pricing. The 60/40 domestic and export split shows good geographical diversification. Valuations need to consider low medium-term ROEs of the business despite a couple of windfall years.

Phenol business

• Deepak made a bold move in 2017 to set up a huge 1600cr phenol plant. This was triple the size of their 500cr+ net block at that time! The plant was set up as per schedule and has contributed strongly to its fy 19 numbers driving up its valuations.

• To understand how to value this, it is important to delve a bit deeper into the Phenol business to understand its economics.

• To start with, Phenol is a classic commodity chemical with huge capital commitments and extremely competitive market driven pricing with periods of over and under supply.

• Phenol is manufactured from Benzene and Propene, both of which are produced in large petrochemical crackers. So, the obvious question is why someone like Reliance has not set up a phenol plant? This is how it has been done elsewhere with PTT phenol in Thailand, Mitsui phenol (direct link with Shell in Jurong Island) in Singapore, Sinopec Phenol in China and Shell Phenol in Europe.

• A key advantage the refineries have is availability of feedstock, while Benzene can usually be procured, Propene has always been in scarce supply due to it being used for higher value chemicals like polypropylene. For example, Mitsui Chemical in Singapore has stopped Phenol production several times due to non-availability of Propene.

• The other important thing to understand is that the technology for phenol is freely available. In Fact, Deepak used KBR for technology and Thyssen Krupp as EPC contractor to set up its plant. The only thing it bought to the table was cash (and courage to take such a risk).

• Success in running any large-scale commodity chemical plant is fully based on cost and operational efficiency. Deepak has no experience in running such a plant where it has to now compete with vertically integrated incumbents who have been running such plants for the past 50 years.

• More importantly, it has a strong disadvantage in RM procurement. How will it then compete once the market balance is restored?

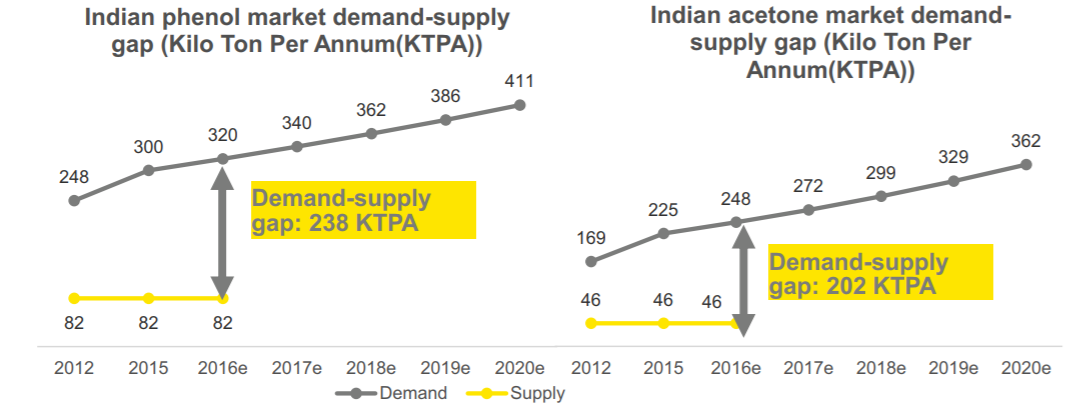

• Supply demand- phenol was in an overcapacity situation from 2012-2017 with at times negative spreads over benzene+ propene. Delay of new plants led to a favorable market which continues today. However, things can change anytime. China is now mostly self-sufficient in Phenol so the two major capacities in SE Asia, PTT Phenol’s 310k tons and Mitsui Singapore’s 200k tons have their eyes set on India.

• Anti dumping- this is no panacea and not easy to impose. Deepak recently lost an antidumping case against Tsaker chemical in China for DASDA. Such duties will only be imposed once Deepak gets into losses which is too late for investors.

Conclusion- prima facie, the entry into Phenol looks like a bold and opportunistic gamble by Deepak purely based on current supply-demand situation. The long-term characteristics of the business would be similar to any commodity chemical business. Big negative is that Deepak has no edge in running such a plant nor any RM procurement edge.

Valuations

• The most important thing to remember when valuing commodity businesses is that any given year of profits only tells you where they are in the commodity cycle, not how much they will make in future years.

• At this point both its phenol profits and DASDA profits (acknowledged in 4qfy19 call) are abnormal. Profits in other chemicals too have been turbocharged by China closures. Thus, PE multiple based valuations would be misleading.

• Another approach could be to look at book value. With its entry into Phenol, Deepak is now clearly a full-fledged commodity chemical company that sells on the spot market. A private buyer if at all interested in such a company would not much pay more than book given its lack of patented products or long-term customer relationships. Deepak currently at around 4000cr market cap trades at 4X its book value of around 1000cr. Clearly on the expensive side.

• Should one pay up for a high probability bright future; is Deepak a rising star? My sense is that while Deepak on balance is a well-run company which has survived decades as a small-scale business in India, it is now charting into unknown territory by venturing into running a large-scale commodity chemical plant with no clear edge. Given this situation, the risk-reward of paying up is weak.

• The sell side has been aggressively extrapolating its current profits into the future with no regard for risks (despite lessons from Avanti, Rain Ind. and Graphite), this is fine for riding the momentum and indeed the prices may well sustain for longer but serious positions cannot be taken at such prices.

• Best to buy such companies when things go wrong and the market forgets about intrinsic strength of the company.