Right 2-3months back bottoming out of spreads did happen. FY2027 should be the time DNL can fire on all cylinders given the amount of capex going live.

Just like the promoter, Market might look to price in the inevitable probability much sooner.

Right 2-3months back bottoming out of spreads did happen. FY2027 should be the time DNL can fire on all cylinders given the amount of capex going live.

Just like the promoter, Market might look to price in the inevitable probability much sooner.

DEEPAK NITRATE; The anti-dumping investigation concerning imports of 4,4-Diamino Stilbene-2,2-Disulphonic Acid (DASDA) from China PR was initiated vide notification dated 27th December 2024.

The applicant has claimed that the subject imports are undercutting and depressing their prices, resulting to financial losses and a negative return on capital employed. Moreover, despite increased production capacity, the applicant’s production and domestic sales have declined. Due to the presence of low-priced imports from China PR, the applicant’s market share has also declined.

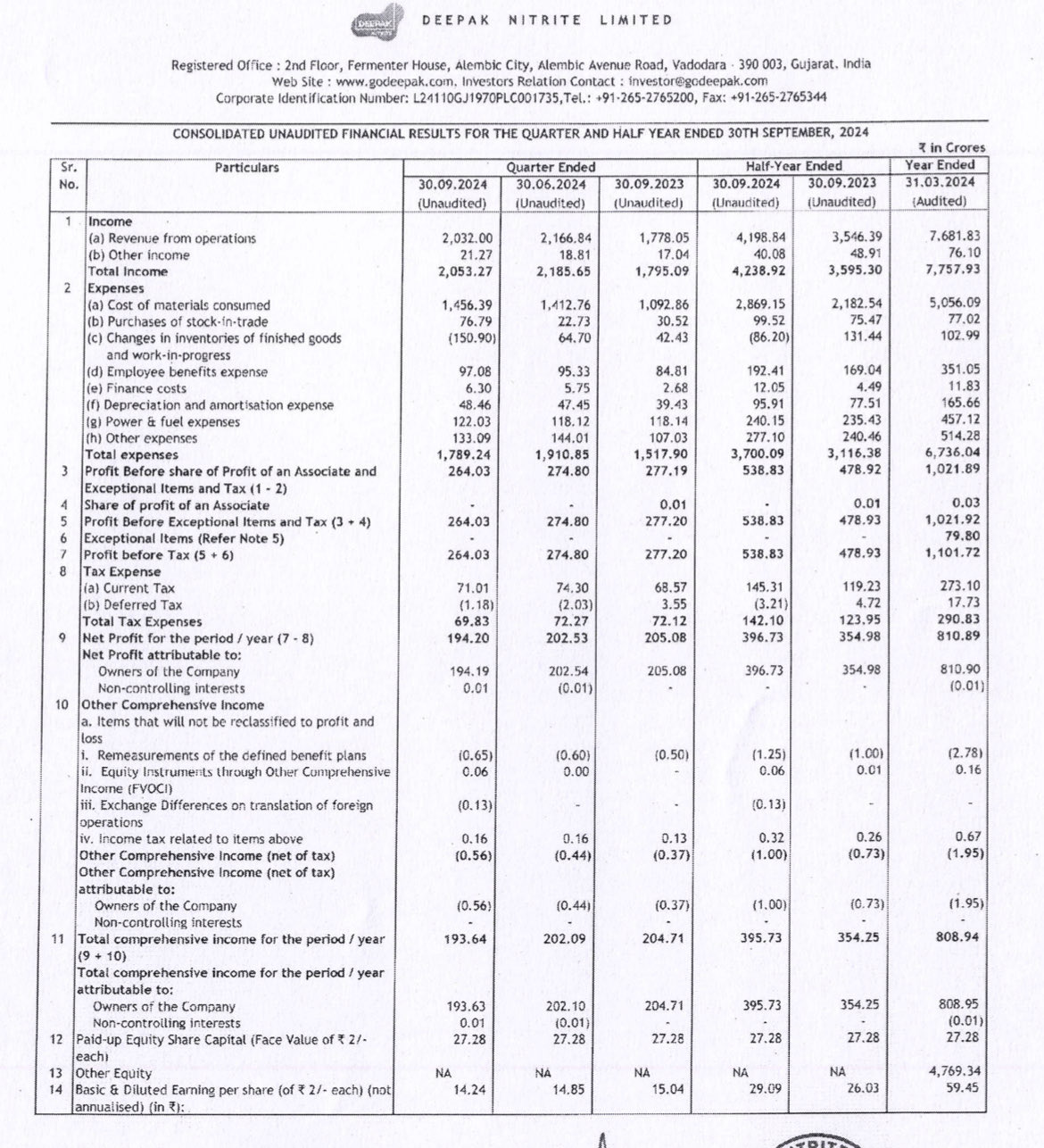

Overall Subdued performance across the board. Looks like, the company is facing multiple headwinds.

Is there a source for split in Rev mix between the different sources over the last few quarters?

One of the fallen small cap Angels, Deep Nitrite has best-in-class management and needs the business cycle to turn. Their stock is down due to huge fall in operating margin %.

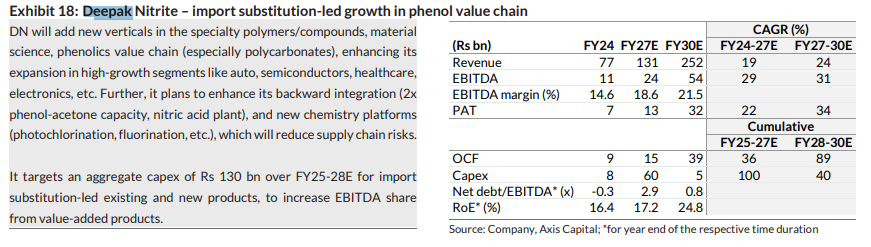

They are focusing on increasing margins by backward integration and import substitution of phenol and acetone, and ramping capex on nitric acid, photochlorination and hydrogenation.

Triggers for Deepak Nitrite could be import substitution via electronics chemical manufacturing in India and the business cycle turning

Every stock is good at the right price. Currently this is richly valued at 45 P/E

There are few managements, i would like to follow because of their experience, honesty and capabilities. This is one of them. More 10-15% of correction and a value would start emerging. Personally, very bullish on few specialty chemicals.

Disclaimer: Not invested. Tracking very closely.

Deepak Nitrite | Q3 Concall

a. Normalization expected between Q1 & Q2 FY26

b. Q4 improvement to be fully realized in Q1FY26

c. Raw material costs seen normalizing in Q4

d. Q4 to be meaningfully better than Q3

Promoter buying in Deepak Nitrite

Smt. Ila D Mehta bought 30.7k shares at 1898.8/sh, earlier she acquired 1.46L shares at 2504/sh ![![]() ] Averaging the position by 50% , need to track

] Averaging the position by 50% , need to track

Deepak Nitrite Limited

Smt. Ila D. Mehta (Promoter Group) bought ~27.1k shares, value Rs. 5.146 cr (Rs. 1898.76 / share) through Market Purchase again

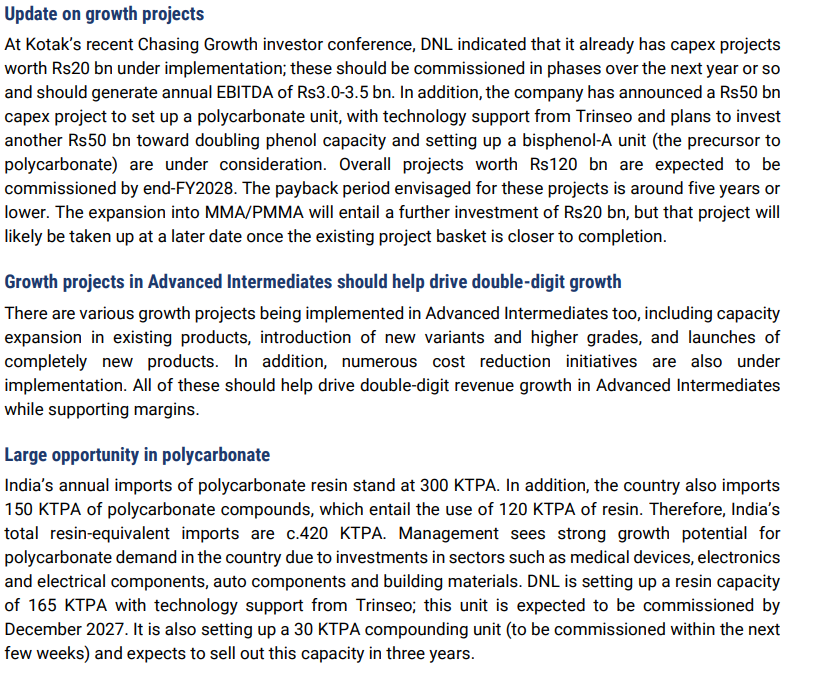

Polycarbonate is produced using phenolics as feedstock

Trinseo is a global materials company specializing in plastics, latex binders, and synthetic rubber. It was originally part of Dow Chemical and later became an independent company. Trinseo provides advanced polymer solutions to industries like automotive, electronics, consumer goods, and construction.

Since BPA is the essential raw material for polycarbonate production, setting up a BPA unit allows for better integration, cost efficiency, and supply chain control in polycarbonate manufacturing.

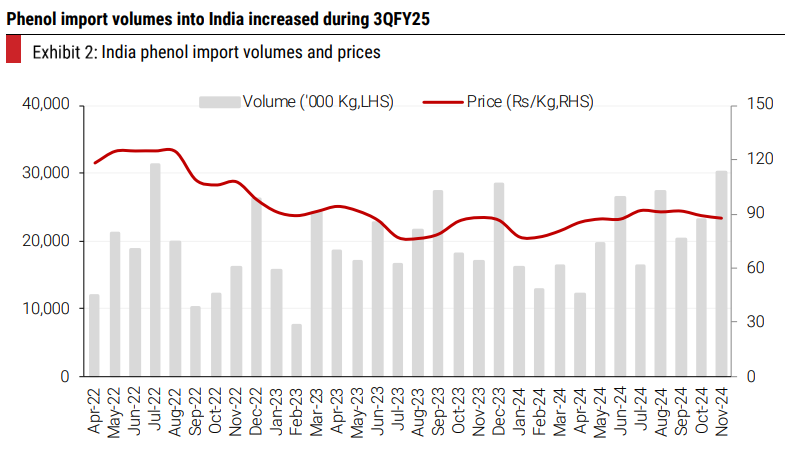

Phenol spreads in India have fallen sharply

Bisphenol-A unit worries me . It is a known endocrine disruptor and EU has banned its use in food packaging. FDA also has some safeguards . Dont know what is to gain from setting up a unit for this since it will be banned across the world by the time they receive payback

Rationale for setting up BPA plant.

Deepak Nitirite

FY27 is inflection year here, Full commissioning of PC Resin + BPA + IPA, Captive nitric acid integration improving cost base. Market is not yet pricing in FY27 optionalities fully

(Segment Wise Scenario)

Phenolics - 16% estimated margins

New Downstream Products (BPA, Polycarbonate Resins) will elevate blended EBITDA margin by FY27–28.

New: Bisphenol-A (BPA) – Higher-margin downstream play (20-25% margins)

New: Polycarbonate Resin – Compounding, import substitution (25-30% margins)

New Specialty Chemicals – Friedel-Craft, fluorination, personal care (18-25% margins )

FY27 ranges

Rev : 11k to 13k Cr

Ebitda Margins : 16-18.5%

PAT could be 1000Cr + if they stretch it could be 1300 Cr too.

Toulene Chain (Adv Intermediates) ::: Crude Oil → Toluene → Nitro Toluene → DASDA / OBA / Toluidines

Toluene is nitrated using nitric acid (which is why backward integration into nitric acid matters).

Benzene Chain ( Phenol, BPA, PC Resins) ::: Crude → Benzene → Cumene → Phenol + Acetone → BPA → Polycarbonate

Deepak is backward integrating all the way from Phenol → BPA → PC Resin, to capture margin and reduce volatility.

Propylene Chain (IPA & Acetone) ::: Crude → Propylene → IPA (Isopropyl Alcohol)

Deepak is India’s largest IPA player - End indus : Pharma, cleaning agents, sanitisers and solvents.

Forward Integration to PC/BPA : Adds value and cushions commodity volatility

Backward Integration into Nitric Acid : Secures nitration capacity for toluene products

Compounding Facility : Accesses sticky, higher-margin niche customers

If after 5 years and spending 5000cr on CAPEX the best the company achieves is the same PAT it achieved in FY22, then the stock is completely overvalued forget undervalued.