I find recent Deepak bhai interview had some data related to IPA here:

Regards,

Sathish

I find recent Deepak bhai interview had some data related to IPA here:

Regards,

Sathish

Result is strong in all front,

Result is good given last 10 days of production on march end still they are able to achieve good top line, even though the raw material price went down they are able to manage the top line good. And dasda price realisation reduced compared qoq as mgmt already communicated. Given all these circumstances the top line improved qoq is too good. And ebitda margin of 35% standalone business very good,but this is tend to go down next quarter onwards. And as per mgmt guideline they are able to achieve 15% ebitda margin on phenol segment is great achievement, and they are able to run the phenol segment full year at full capacity without hiccups,is very good achievement.

Bought landbank across all sites around 140 acres will help for next set of CapEx . Eagerly waiting for concal hear from mgmt next set of CapEx.

Regards,

Sathish

Deepak nitrite concal summary:

Debt to Equity is at 0.66 as per screener. Is this okay ? Is there any anyway to find out the company’s debt for the last 3/5 years? I am looking for yoy trend of debt.

Better metric is interest coverage ratio in my opinion. And last 3 years debt level is not good indicator for Deepak nitrite as they were doing large CapEx for 1500cr phenol plant which is done through 1000cr loan. Last year they commissioned the plant we may see reduce debt going forward.

Sathish

The foray into sanitizers, is it not going out of their core area? The FMCG players are the big guys here. They know how to target and get customers to buy their products in B2C.

Is this not ‘deworsification’?

Hi,

Deepak nitrite doing IPA which is raw material for sanitizer and in IPA is derived from acetone ,so it only improve their margin and sanitizer foray is by Deepak fertilizer not Deepak nitrite

Regards

Sathish

Thanks Sathish for the clarification. I just read about the CapEx news which was done in 2019. Also I see interest coverage ratio is at 8, which I feel is better.

IPA prices by chinese suppliers are up 100%. Apt timing to starting IPA production by Deepak Nitrite

IPA for sanitzers is price capped.

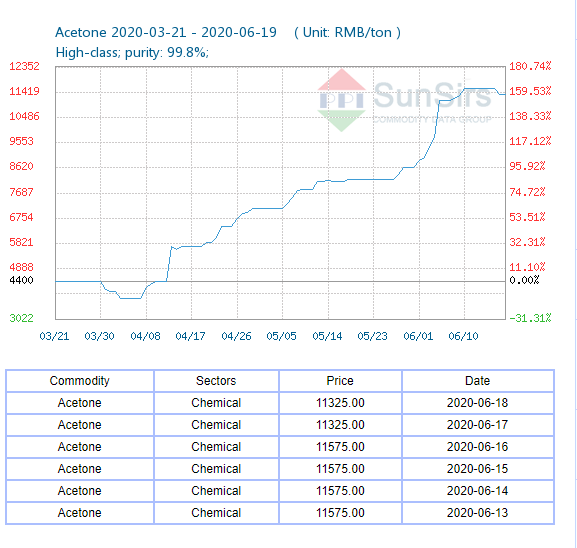

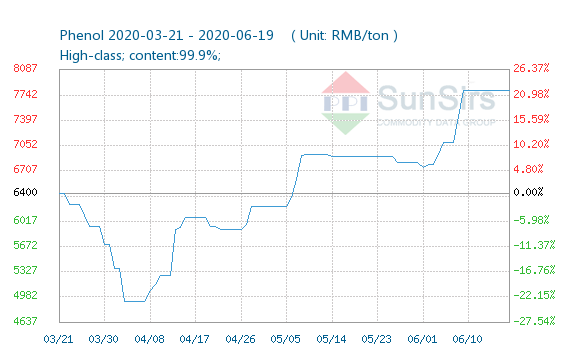

Deepak Nitrite has the largest acetone and phenol plants and their prices have been rocketting

Acetone is up 159%

Phenol 20% up

sources: http://www.sunsirs.com/uk/prodetail-464.html

http://www.sunsirs.com/uk/prodetail-582.html

disclosure: invested tracking quantity

Yes for sanitizer it is capped but for pharma usage it is not capped. And Deepak producing pharma grade IPA additional to industrial grade IPA will see some additional benefits.

Just thinking what is left for Deepak Nitrite after huge base effect of DASDA tailwind, and from where next incremental 2000cr revenue bump up will come to achieve Deepak bhai vision of achieving 1billion dollar revenue by 2022-2023.

Regards,

Sathish

https://myinvestmentdiary.com/quarterly-result-analysis/deepak-nitrite-ltd-q4fy20-analysis/ gud analysis

Edelweiss report on Chemicals sector: Q4 analysis, trends, covid impact, deeper analysis of 6 companies inclusive of Deepak Nitrite

Full Report

Deepak nitrite was close to this explosion 8 km. Not sure if the company is running or closed due to local tensions.

On 26 May, Shri Mautik Mehta elevated as Executive Director ft CEO of the Company with effect from 1st June, 2020.

He is of age 37 Year, having 12 yr of experience, son of Shri D. C. Mehta, Chairman and Managing Director and nephew of Shri A. C. Mehta, NonExecutive Director.

Isn’t he is too young to be CEO of the company.

Deepak Nitrite- Transformation into Specialty Player underway…

Written by- Amit Babbar (July 9 2020)

Putting basic chemistry in place and then building specialty blocks on top…this has transformed Aarti Industries from Benzene manufacturer to Specialty player supplying lucrative Benzene (and later Toluene) derivatives. PAT margins improved from 6% in 2014 to 13% in FY20- resulting in PE re-rating from 5x to 30x… Deepak Nitrite could follow a similar trajectory.

Chemicals manufacturer since 5 decades, Deepak Nitrite has history of ramping up market shares across chemistries- having dominant market share in most of its key products.

Started getting into Phenol few years back- commissioned a massive 1400 cr plant with textbook style execution.

Now sitting on an absolute goldmine as Phenol considered building block for vast number of high potential derivative products.

Company literally can pick and choose from a vast array of equally remunerative products, each with massive import substitution opportunity in India.

Opportunities include setting a polycarbonates (Bisphenol) capacity in India. Despite sizeable domestic demand, there is no domestic production of polycarbonates. These also include high margin Phenolic resins manufacturing opportunity- something no Indian manufacturer can produce at the moment.

Other big lucrative opportunities include use in agriculture and pharmaceuticals.

2 of the biggest drugs in India- Paracetamol and Aspirin- have Phenol as base material, and almost fully imported in India. Paracetamol is made by treating Phenol with Sodium Nitrate (leading to 4 Amino Phenol or PAP, the API) and Acetic Anhydride. Aspirin can be made by reacting Phenol with Salicylic Acid and Acetic Anhydride. Given the strong chemistry skills of Deepak Nitrite these should not be tough to master.

Strong chance most of the existing Phenol could get used entirely in high value derivatives itself- that would complete transition from a bulk commodity producer to a specialty chemicals producer.

Company already handpicked its first opportunity- announced capex on Isopropyl Alcohol (IPA), comes from Acetone- a co product in Phenol production facing strong tailwinds as Pharma localisation picks up. This is expected to hit peak utilisation levels in record time !

With these kind of opportunities it is baffling stock trades at a 10x (trailing) PE multiple !

Even the base product (Phenol) has zero competition as the only 2 other competitors are almost out of the market now ! New players cannot compete as tricky chemistry to master that most definitely requires outside technology- multiple players have tried in past and failed- a prominent player in west India tried with own r&d and failed miserably.

Interestingly even at this point financials for Deepak Nitrite are in much better shape than Aarti’s- with better margins and return profile and strong cash generation- almost 700 cr a year. While improved performance in DASDA segment can be argued, even on normalised basis a 1/3rd valuation difference is simply not justified.

Company recently bought a 127 acre new land for expansion, 2x the land bought earlier for Phenol- potential products’ market is so big just 1-2 product lines can potentially fill the entire 127 acres !