Though very tempted to take up a position basis the above excellent note by @phreakv6 - I did not currently invest in the company for the reasons below:-

The massive Capex plan deters me in the mid - short term. It’s definitely a potential game changer in the future, but I would prefer to track the company’s progress over the next few months and try to evaluate if it continues to make sense.

I was not as positive about the end use industries the companies products operate in. I am not as certain about the longetivity in the mining/commodity cycle, so I was just worried I might be looking at an end use industry which might be currently at high utilisation levels

I would’ve preferred the company to expand Capex into TAN rather than deferring it. The chemicals piece is key to the investment here, and even though the Ammonia Capex gives margin expansion in the future, it’s a long term project

That said, the current trailing valuations on current sales and product mix are extremely attractive and I will potentially regret this decision - the share price movement today is already proving me wrong! I was also impressed with the management clarity over the concall.

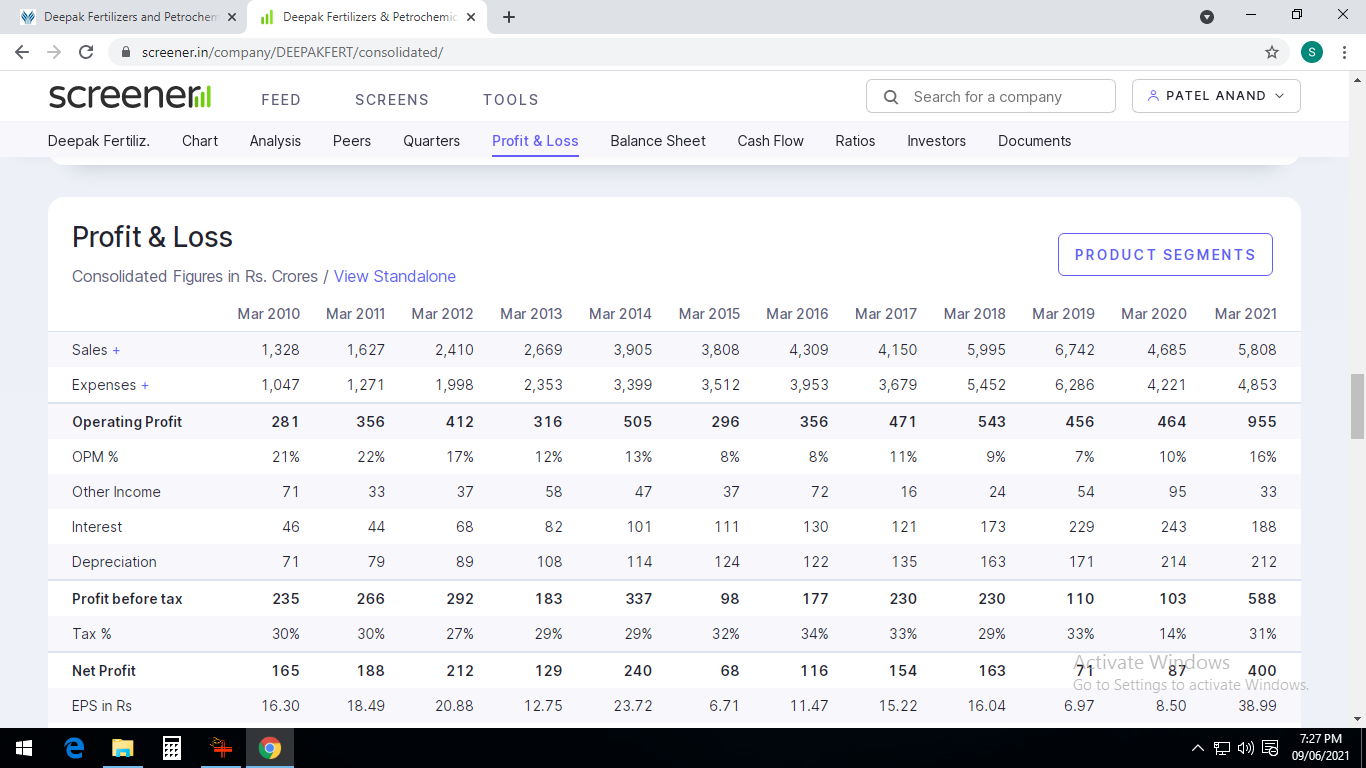

Deepak Fertilizers used to have 20%+ margins in 2010-11 even with small scale of operation

Spread like D. nitrite possible in Mining and acid part , but fertilizers is regulated by gov

Ammonia is for internal consumption , cost of setting up plant can be recovered in 6-7 years

They are delinking from ammonia price fluctuations but linking to LNG prices after NH3 plant completion. LNG is somewhat more stable, but not risk free

This is where the management made a reference to specializing within the fertilizer space. In the Chemicals space, the company is offering TAN, LDAN and AN Melt which are specialty chemicals and also Nitric Acid in various concentrations (Turns out even diluting Nitric acid is a value-add at industrial scale due to its toxicity). They have also reduced trading in commodity fertilizers like DAP. (These are elsewhere in the transcript)

4. Economics of Ammonia

Looks like the company doesn’t have to sell any Ammonia from the new plant when it comes online as their need is about 0.5 million tonnes (same as capacity, so 100% utilization from the beginning). So this is going to be a complete backward-integration project with zero sales risk. To put it in perspective India currently imports 2.5 million tonnes of Anhydrous Ammonia in a year.

Going by the above, we can assume topline will not grow but there will be very good margin expansion even when Ammonia prices stay close to long-term average. They will be able to price TAN, CNA higher when Ammonia prices go up and have even higher margins. So EBITDA expansion could be about 600 Cr as a base case. The Operating Margins could be north of 40%, even approaching 50% as the best case if my calculations are right. The volatility in margins will also probably reduce as LNG prices are relatively more stable than ammonia

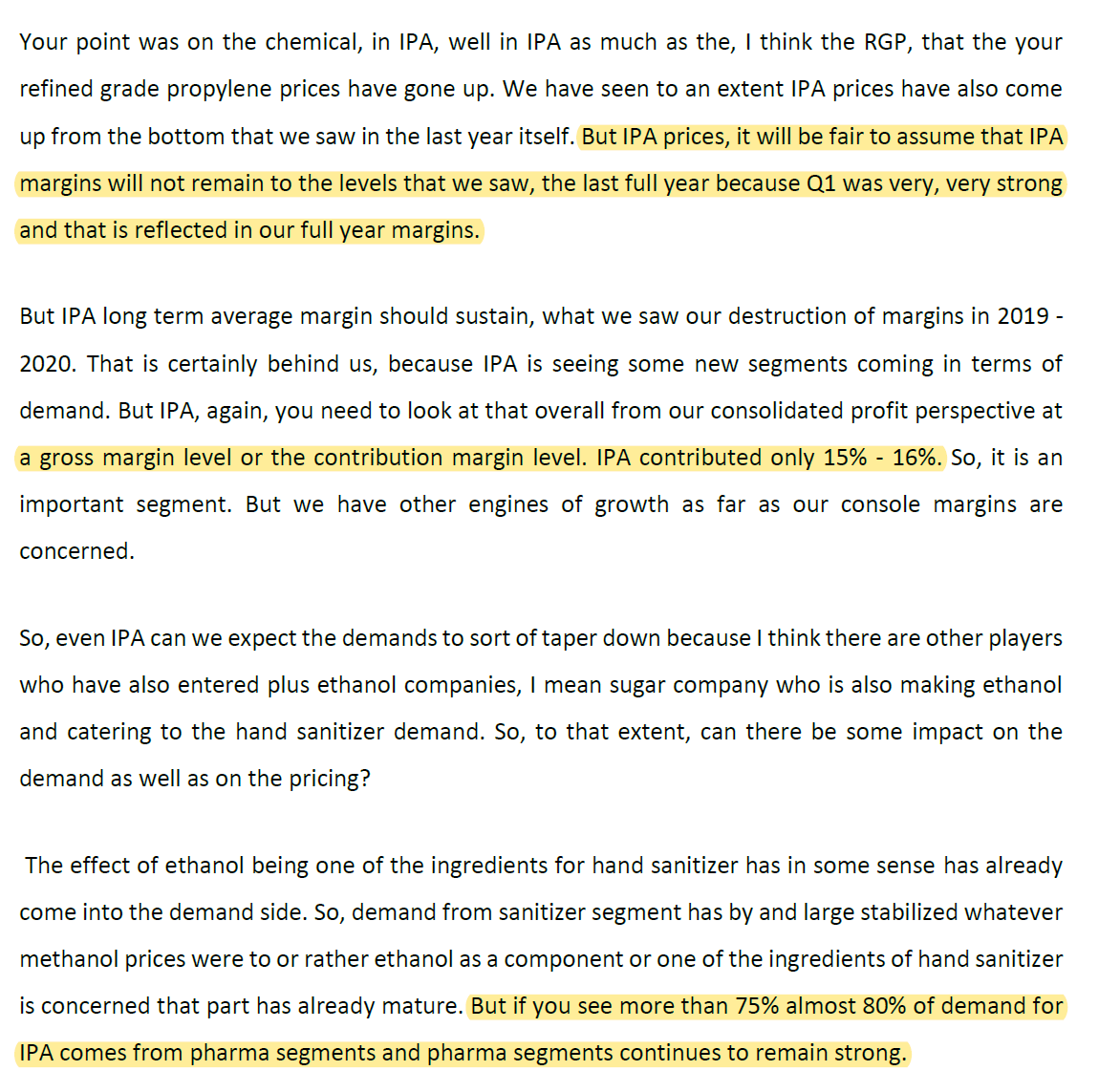

As I had earlier calculated (150 Cr/950 Cr was my estimate in my previous post), the management’s number as well is close to 15% for IPA contribution to Operating Profits. Though hand sanitizer contribution will reduce, 75-80% of demand comes from pharma space and will sustain. Margins will reduce compared to FY21 though. My guess is that this reduction could be to the tune of about 50 Cr and IPA could still contribute 100 Cr to profits from 150 Cr in FY21.

They had designed their plant with gas as a fuel in mind and suddenly gas supply was discontinued and that impacted them dramatically from 2014/15 …

Then at the same time their large amount of fertiliser subsidy was held back leading to huge working capital overhang and cost . Inspite of court ruling in Deepak Fertiliser favour the issue was not resolved for long time

Then they got into dirty fight over Mallya’s fertiliser plant in 2016/17 … finally Zurari took over that plant …

Now all that is behind … and now management is fully focussed on their operation …

Key to note up to 2007 Deepak fertiliser was far ahead among all chemical companies , but because of lot of diversions it fell behind in 2010- 2018 period ,

Thanks for the wonderful analysis. I have one question.

Amount spent on Ammonia capex is 4000cr. The amount of money needs to be spent to import 0.5 million tonnes of ammonia is approx. 1800 cr. Is not the asset turn is bit low ? Is there any thing I am missing here?

Interesting discussion. Few points which I could think of:

Is there any other source to validate this. Because they have been offering these since 3 years. If that’s the case, why hasn’t the shift from commodity to specialty happened in last 3 years or why hasn’t the company spoken about it so far.

These points were made in Q4 call. While it says there is a shift in nitric acid business – China to India. One would have expected it to be a more seamless & secular trend. But if we compare quarter wise margins – there is volatility in margins – a drop in Q2. Which is a little uncommon for specialty chemicals, IMO.

Comparison with DN on margins improvement trajectory–

For Deepak Nitrite –margin improvement largely came from fine & speciality chemicals division. They were manufacturing products which are not price sensitive. Products which were customized as per client’s needs. DN - more diversified player even in FY 18-19.

In case of Deepak fertilizers, I think the demand in chemicals this year is linked to strong demand in end user industries (pharma, agrochem; for LDAN – cement, steel, etc). Should track how it pans out in the coming quarters. Not sure if it would be appropriate to compare the margin trajectory with Deepak Nitrite, at this juncture

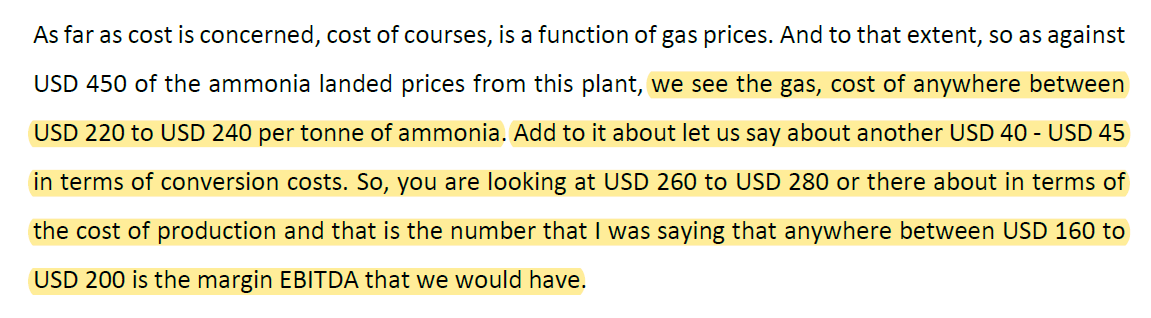

As per the details provided in the con call

Average price of ammonia $380 to 390 (avg 385)

Logistics cost $80 to 90

Total landing cost $450 to 470 (avg 460)

Cost of gas for manufacturing $220 to 240

Other conversion costs $40 to 45

Total cost $260 to 280

EBITDA benefit including adv of logistics cost 160 to 200 (avg 180)

EBITDA benefit excluding logistics coat 80 to 120 ( avg 100)

Total capacity of the plant 510KTPA

Cost benefit including logistics (Revenue+Logistics) = 510 x 460 = 235 million $ = 1650cr

Cost benefit excluding logistics (Revenue) = 510 x 385 = 196 million $ = 1375cr

EBITDA benefit including adv of logistics cost = 510 x 180 = 92 million $ = 645cr

EBITDA benefit excluding adv of logistics cost = 510 x 100 = 51 million $ = 360cr

Now what is the total ammonia project cost? I think 4000cr is too high.

lets consider 3000cr (i will updated calculation later with actual cost ) and I am not considering working capital requirement as plant is mostly for captive use.

Asset turn = 0.55x (0.46x)

Total Pre tax ROCE = 645 / 3000cr = 21.5% (360/3000=12%)

So the conclusion is this project can generate 12% return if all ammonia sold to others. (substantial working capital will drag this number to further down) and 21% if used for captive consumption

Imagine you are buyer of a chemical . Its cost is <10% of your total product cost ,

You have two supplier one is domestic and one is in China or South east Asia. Both offer same rate what will you do …

In most chemicals this is the story …

If domestic supplier builds capacity which is > 60% of domestic demand … He will slowly gets unfair adv over competition because of qualitative factors - esp customs delay issues , import duty uncertainty , currency issues and payment terms .

Is this a speciality chemical story …

Well I believe all B2B chemicals are basically commodities , there was sector tailwind in last 10 years like it happened in early 1990s … but as in past slowly all these chemical companies will get into each other business and competition will increase … and people will realise there is no major rocket science ( esp w/o major R&D expenditure and long duration patents ).

This has happened in past and will happen in future …

Discl : Coming to Deepak fertiliser … I have been in and out of this stock several times in past 5/6 years … My average price is Rs 91 and I am partially booking profits now near Rs 400 and 100% exit price as per my model is 780 …

While going through the Annual report for FY19-20, there is some warrants issued to one of the promoter entity by the company and it seems the promoter group asked for the extension for warrant closure which again they defaulted. Can someone help me in understanding the entire flow as to what has happened and why company again is looking for fresh fund inflows.

As per latest ICRA report there had been a substantial cost overrun in CAPEX from Rs 2920 Cr to Rs 4350 Cr i.e almost Rs 1430 Cr or 50% of the initial project cost.

Additionally, the group is planning to implement TAN project in near future, whose earlier budgeted project cost has increased owing to increase in costs of project utilities and other reasons.

“Besides, ICRA notes that there has been a time overrun (from Q4FY2022 to Q1FY2024) in the Ammonia project due to Covid19 pandemic-related challenges and land acquisition and land conversion issues. It also faced cost overrun (from Rs 2,920

crore to Rs 4,350 crore) owing to increase in land acquisition costs, EPC cost, addition of certain project components,

increase in foreign exchange component, increase in cost towards storage and preservation of equipment and interest

during construction (IDC). Due to unavailability of land in MIDC, the company had to purchase an agricultural land nearby,

and convert it into industrial land, which led to the delay and increase in overall costs. Additionally, the group is planning to

implement TAN project in near future, whose earlier budgeted project cost has increased owing to increase in costs of

project utilities and other reasons. The timely execution of the ammonia and TAN projects as well as ramp up of operations

within the revised timeline and cost budget would remain a key sensitivity. Going forward, the liquidity is expected to remain

strong on the back of high anticipated cash accruals, large unutilised fund based limits, limited debt repayments and

anticipated equity fusion from multilateral institution and from monetisation of assets.”

It’s under long term ASM now and circuit limit is 5%. So, traders aren’t interested. Only long term investors are interested right now. Should see reboud in a day or two.

True, but they have said that around 70% of the capacity can be used for captive consumption. For rest 30%, they’re still free to explore opportunities.

This is ofcourse a very long shot right now since DF isn’t into major R&D and at a global scale, Ammonia usage isn’t at a large commercial scale right now.

I think there are no green Ammonia projects presently in India and probably the proposed Ammonia project in Deepak Fertiliser is also conventional Ammonia manufacturing plant.

As per the ICRA credit report Ammonia project faced a cost over run from 2920cr to 4350cr. This is very huge over run of nearly 50%. With this kind of over run, project ROCE will fall drastically, how management will justify it.

This sort of activity of meeting investors is a bit abnormal perhaps. They have met investors almost every day in the last 1 month and quite a few of these are group meetings with a whole of funds domestic and international from Kotak, ASK, Abakkus, Sage One, Elara to Fidelity and some US based funds.

My guess would be the investors wanting to take a piece of pie in another chemical story, currently available at discount. While i’m not sure to what extent segmentation of commodity chemicals makes them speciality - but by doing a large backward integration and also capex in TAN, they’re trying to repeat a Deepak Nitrite.

Also, another thing is that Fidelity has taken a 1 to 2% stake in Deepak Fert as per the latest sharholding pattern. So I sense, this is mostly investor interest.

At current prices, I don’t think there’s a whole lot of downside risk.