Insider trading is a negative check list for many institutional investors…

Income Tax Raid was also there in Company 2 years back with claim of around Rs 500 Cr on the Company…

Company should make efforts for improvement in Corporate Governance matters…

FY 2022-23 was an exceptional year, Amonium Nitrate prices had reached historical high of EUR 850 /MT… as against average price of around EUR 200-250 for last 10years. Topline growth may be flat during current FY and there will be pressure on the margins also.

Margins have already started declining : last four Quarter margins Mar 22: 25% June 22 : 24%

Sept 22 : 18%

Dec 22: 17%

Market seems to have already factored in Peak price and peak Margins and the share price is already down from Rs 1030 to Rs 600

Disclosure : Exited my position and will review entry once the margin stablises.

Hi guys this is my first chemical company analysis so please pardon me incase my understanding of few concept is wrong. So let’s begin

CAPEX

A. Problems During large capex

-

There can be a delay in capex and the cost estimates can be wrong. So in Deepaks case this has already happened so in my view it is already priced in. One of the major reason for this was they bought land close to the main road which was expensive than the land 1 to 2km away for main road and the conversion of land to industrial land. So expensive land and delayed conversion.

-

If you are doing backward integration for RM how competitively can you make the RM, how critical it is for your business, do you have any experience. So in short above in the thread we have seen how critical the RM is ( it is close to 80% of their entire RM used across different vertical) they already have experience of making ammonia.

How competitively?

So ammonia is made from natural gas and Deepak will buy NG internationally in the form of LNG(Liquefied Natural Gas) and domestically. So a company who has a factory in Middle east has access to cheaper NG and hence they can make it more competitively. But as per management the economics are in their favor such that it is as good as buying NG at middle east rates.

So as per management the ammonia capex cost is 20% to 30% lower than somebody who would have done In middle east and the economics are in their favor such they are buying NG at middle east rate. (will explain later in detail)

- Who is using the RM. In deepaks case 100% is being used for internal use. (Big advantage)

- DEBT- So in their case they take long term debt of more than 10years in this kind of setup the burden to pay principle is very low so their basic cash flow generating ability should be able to handle this. Their next three year obligation is very low as per management.

- Commissioning, scaling and stabilizing. In deepaks case the plant will start commercial production from Q2 and in this FY it will run for 9 months at 75% to 80% utilization. DFPCL Ammonia Project Update (April 2023) - YouTube ( Status of plant as on april)

The engineering of this plant has been done by TOYO a 80year old Japanese company and here are few of it past projects.

They are pretty experienced and the contract with Deepak fertilizer is a performance guarantee contract where TOYO will have to prove the capacity, purity, efficiency. I am pretty confident that the project will be running by Q2 FY24 commercially. I my view there will be now commissioning issue.

These are majorly all the problems a chemical company can face when doing large capex .

B. Ammonia economic and GAS

Economics per TON

- They are going to save anywhere between 80$ to 90$ on logistics.

- They are going to get 9% of SGST refund of the transfer pricing from ammonia plant to the consumption plant. So basically 9% of ammonia price per TON. So if ammonia is 500$ then they will get 45$

- Since this is an exothermic activity the ammonia plant will release a lot of energy which will be used in their TAN plant which is close to 10$ to 15$ of savings per TON

- The difference between the GAS price and ammonia price

- This entire projects adds 200cr of interest cost and close to 110cr of depreciation ( as per Q4 concall)

- They have 25$ to 30$ of other expense which is basically to run the plant.

So if you take ammonia price of 450$ then all the additional benefit will be close to 140$ so when you convert this 140$ in LNG terms it comes out to be 3.5$ to 4$ and on an average gas prices have been 8$ to 8.5$ hence it is as good as buying gas at 4$ to 4.5$

GAS

First let us understand the relation between ammonia and gas. With my limited understanding ammonia demand is most of the time going to be there and will grow at a certain % the supply side disruption is the major reason for price fluctuation.

During Russia war gas prices went up pretty fast this lead to most of the ammonia factory shutting down in Europe GAS is RM hence ammonia shortage prices went up. Now GAS prices came down factory opening, ammonia oversupply hence ammonia price down. Now there has to be a certain margin in producing ammonia. Like if gas is 100$ ammonia has to be 110$ whenever there is disruption in this margin the supply side adjust. GAS is more volatile and ammonia price take time to adjust hence we see these cycles. Like in the above example now ammonia price are so low that the margins are again being affected.

China also plays a role here being a large supplier. So there has to always be a spread between

ammonia and gas other we would keep seeing the cycles.

I don’t know how relevant the above table is it came from chat GPT

They have tied up close to 68% of GAS requirement and they will do it for balance as well before commissioning

As per management for 10$ of LNG landed cost on per TON basis is 330$ (conversion and freight included)

So current Gas price is 11$ to 11.5$ landed which is close to 360$ to 375$ on per ton basis and the current ammonia price FOB Middle East is 280$. If I include all the benefits as on date the ammonia realization will be 410$ and their operational cost is 25$ to 30$ so they are at break even.

So as per above logic this should be the case with other global manufacturer as well so now either gas has to fall or ammonia rise but definitely they are in a down cycle

THIS IS ONE OF THE BIGGEST RISK FOR ANY CHEMICAL COMPANY DOING CAPEX BECAUSE THEY ARE AT BREAK EVEN BUT THEY HAVE INCREMENTAL DEPRECIATION AND INTEREST OF 310CR. DESTRUCTION OF P&L

Currently in domestic market ammonia is selling at 50% to 60% premium.

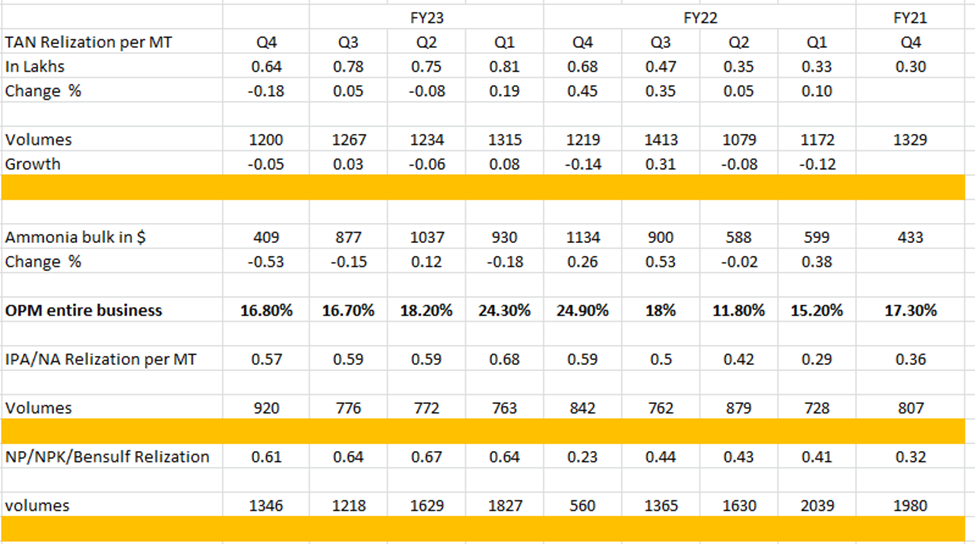

Q4 ANALYSIS AND ROAD AHEAD

In the above table see ammonia Price chance and TAN realization change with 1 quarter lag.

- Like in Q1 Ammonia up by 38% but TAN up by 5% margins at 11.8%. FY22

- Q2 Ammonia down by 2% but in Q3 TAN up by 35% margins 18%. FY22

- In Q4 TAN down by 18% and in Q3 ammonia down by 15%. FY23

- In Q4 ammonia down by 53% so in Q1 FY24 TAN can be down by 50% to 60%

.

Just a small point that even if TAN moves up or down by less percentage than ammonia it will in absolute terms create a positive effect in up move and negative in down move.

In Q4 the margins have improved by 10bps and they have performed more than my expectation but HOW?

-

IPA in Q4 has performed phenomenally because Safeguard Quantative Restriction was imposed on IPA dated 31st March 2023 by Directorate General of Foreign Trade. This means IPA cannot be imported now

-

Fertilizers segment benefits with falling ammonia price and this segment has also performed exceptionally

MY TAKE

-

They have entered down cycle and next quarter can be a horrible quarter we saw that in Q4 ammonia is down by 53%. So let’s see how much can IPA, Fertilizer rescue the TAN, Like if you see Q4FY21 and Q1FY22 TAN realizations were almost 50% down from current level and margins were between 15% to 17%. if they can give in these lines then it is good.

-

Ammonia plant looks like more of a burden this year than creating value but we tried to see the economic cycle so as per me either GAS has to fall or ammonia has to RISE. Will take time nobody can predict

-

They are making a lot of efforts on Steel Grade, Solar grade acids they are also working on TAN as a solution rather than product and as per them this solution will give them premium margins.

-

Technical

500 is a big time time support and 300 to 400 the sub sequent support looks like we can see 300 to 400 levels in the coming time unless we have a rally in ammonia or fall in GAS price

Overall the possibility of operational or commissioning issue looks low but the economics are not favorable for them. Lets see like they are saying domestic price are up by 50% to 60% so they can also sell some ammonia.

Thankyou

@manhar thanks for summarizing Concal commentary with your analysis. Gas prices have also fallen down drastically during last months , however they might have contracted at a higher price. Historically , Q4 has been the strongest quarter for Tan sales and hence Q1 and Q4 are expected to be subdued. Ammonia plant is expected to drag down the margins during FY 2023-24. Further TAN prices have also fallen by 50% from its peak along with other commodity prices which will is likely to have a negative impact on the top line. Stock is likely to fall from this level and consolidate in the range of 300 to 400 during FY 23-24.

c0183bc2-a575-4250-98ca-5f60a3801a01.pdf (183.7 KB)

Performance Chemiserve Limited (Issuer) a wholly owned subsidiary of the Company has raised Rs.900 Crores by issue and allotment of rated, listed, unsecured, redeemable non-convertible debentures (NCDs) on private placement basis to qualified institutional buyers

Are they working on green ammonia? Any views on the same?

-

Ammonia production uses about 2% of the world’s fossil fuel energy and generates more than 420 million tons of CO2 per year.

-

Approximately 80% of ammonia is utilized for fertilizers, with around 5% for explosives and the balance for other chemical commodities

Ammonia Production Process: Ammonia is produced by the highly energy- and carbon-intensive Haber-Bosch process, which requires temperatures of 450–500°C and pressures of up to 200 bar.

-

The feedstock for this process is hydrogen from natural gas (NG), coal, or oil, and nitrogen.

-

Per ton of ammonia consumed, energy from NG, coal, and fuel oil is 7.8, 10.6, and 11.7 MWh, respectively.

Producing ammonia from renewable sources is nothing new. In the past, a number of hydropower plants synthesized ammonia using hydrogen produced from electrolysis as the feedstock. Several large-scale electrolytic hydrogen facilities have been built since 1928, when hydrogen was first produced via hydroelectric power in Norway. By the 1970s, plants in India, Egypt, Zimbabwe, Peru, Iceland, and Canada were also producing fertilizers from electrolytic hydrogen, the largest of these facilities being a 180-megawatt plant in Egypt.

However, due to falling NG prices and increasing local electricity demand, many of these plants have been closed or converted into NG feedstock-based plants for ammonia synthesis.

Ammonia can be produced by wind power. Beginning in the early 1960s, wind-powered ammonia production was investigated by the United States Army through an initiative called the “Energy Depot Concept.” Later, in the 1970s, ammonia production using wind power in a stand-alone system was extensively explored by Lockheed California Company and the U.S. National Science Foundation. While both the U.S. Army and Lockheed/NSF found that wind power could be used to produce ammonia, neither constructed a wind-powered ammonia prototype plant nor discussed the economics of building a wind-powered ammonia plant in any significant depth.

-

In the renewable ammonia or Green ammonia synthesis process, hydrogen is produced by electrolysis. The required electricity is generated from a renewable source, such as solar or wind generators. The hydrogen and nitrogen from an air separation unit (ASU) are compressed to the required synthesis pressure and fed to the Haber-Bosch synthesis reactor.

-

The cost of the ammonia for this route is mainly dependent on the electrolyser capital costs and electricity input costs.

-

Casale, Haldor Topsoe, ThyssenKrupp, and KBR all developing designs for the integration of their ammonia synthesis technologies with renewable powered electrolyzers.

post deleted as already covered beautifully and in detail by @manhar

Deepak Horrible result as you expected

Hi everybody,

The results are not how exactly I expected, there are new things which I am seeing.

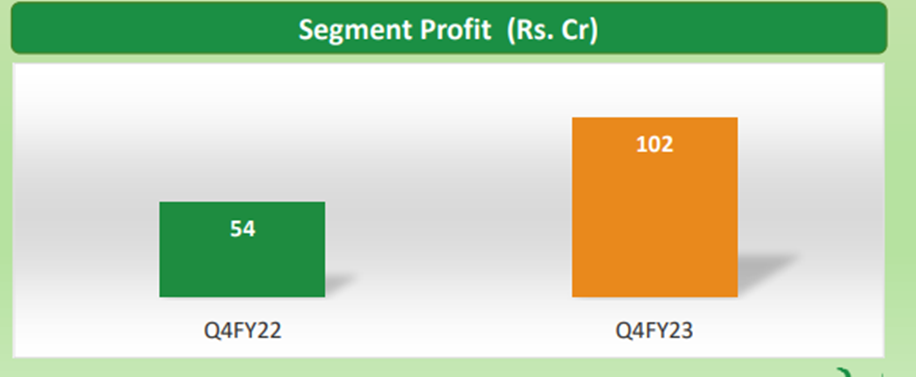

The fertilizer segment was totally unexpected,

we can see from a profit of 101cr in Q4FY23 to loss of 69cr in Q1FY24

-

They took a 161cr of hit

-

Finance cost is almost up by 90% YoY, I think this should still go higher in Q2

-

I cannot see depreciation increasing in this quarter. I think this is because their trial production started in JULY 10th so for next quarter we should see depreciation going up

This quarter dep is 59cr and last quarter it was 69cr . (this can go up by 20 to 25cr, just my guess)

-

Chemical segment profitability down by 54% YoY and 11% QoQ this is despite IPA doing extremely good. (I think IPA comes under chemical segment, please correct if wrong)

- TAN they are expecting volumes to decrease in Q2 due to monsoon and ammonia prices have further corrected form last quarter so Q2 TAN it looks like can be the worst.

Next quarter

- TAN volumes will go down, ammonia prices have further corrected

- Interest cost will go up, depreciation will go up

- IPA should be strong, fertilizer I have no idea.

Looks like next quarter PAT can be either in same lines as current quarter or even worse. Wafting for concall (if they would do) for better understanding. Overall if 500 is breached we are definitely seeing 400.

I am very much interested in this company and I think ammonia capex is going to be value accretive, waiting for the right time to enter where margin of safety is high. They only thing which is difficult to predict is weather all of this is already priced in or not.

Disc- tracking

As per the Concal Ammonia Business will be a dragger for this FY.

Fertiliser will not add to any Profit on an annual basis as subsidy has been withdrawn from back date and hence incremental profit will only offset the losses of Rs 168 Cr.

TAN business margins will be lower because of Dumping from Russia which may continue for another 2 to 3 quarters.

Nitric acid will have normal commodity margins.

IPA business will be the main driver of profit during current FY.

Overall I see a negative performance for the Company and Stock price during the current year and valuation may come down to the range of 300 to 400.

Any improvement in Ammonia business may change the scenario and then we will have to relook the Company.

Disclosure: No holdings and tracking the overall chemical sector.