Did some fundamental research on Deepak Fertilizers and putting my thoughts here.

My first impressions on the business at a surface level

- This is a fertilizer business - has fertilizer in the name and has a fertilizer business P/E (reinforcing cause/effect cycle)

- Numbers look good (which is why I was looking at it any way) - but they are the largest manufacturer of IPA - So Covid should be driving the numbers and so they must be one-off

With this first impression, I set out to understand the business.

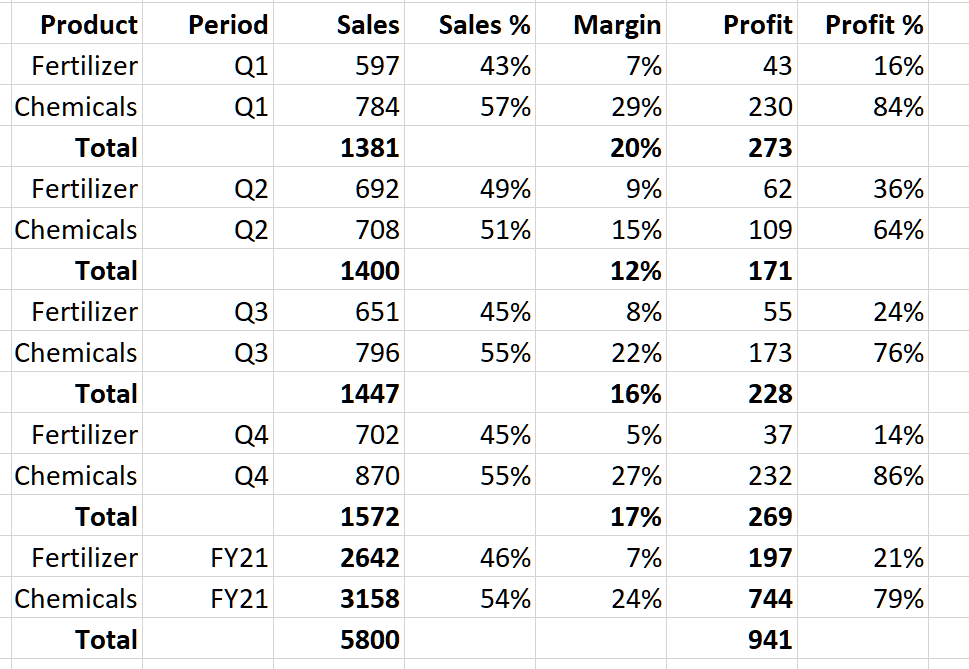

These are the numbers I pulled up from the last 4 Investor Presentations in FY21.

Looking at these, few things stand out

- Though Fertilizer business contributes a lot to the topline, its contribution to the bottomline is much lesser. Chemical business contributes 80% of the profits.

- Chemicals margins are at a respectable 24% for FY21. This appears to be continuously improving on account of increase in TAN contribution when compared to FY19 and FY20 - There is almost 30% increase in volume of TAN and consequently the margin profile has continuously improved

But what about IPA? Is it contributing disproportionately to the profits in FY21?

IPA sales as per my calculations by looking at the 4 investor presentations works out to about 550 Cr. That’s about 9% contribution to the topline (18% to Chemicals). They are likely to have made about 150 Cr profit from IPA sales. So the more than doubling of operating profit from 450 Cr to 950 Cr - 500 Cr odd increase, had a contribution of about 150 Cr from IPA which may reduce by about 50 Cr when Covid demand reduces. But the rest of the increase of about 350 odd Cr could be the sustainable increase due to operating leverage in the TAN (Technical Ammonium Nitrate) and CNA (Nitric Acid) business. Again, lot of guesstimating - so please verify on your own.

The improvement in product mix by reducing of low-margin trading products is also visible in the working capital management.

There is also a big improvement in OCF which has helped in reducing debt from 3000 Cr to about 2300 Cr. The net D/E of the business improves as a consequence from 1.2x to 0.65x

While researching I discovered that they have major market share in these. #1 in India in all and 2nd largest manufacturer of Nitric Acid in SE Asia

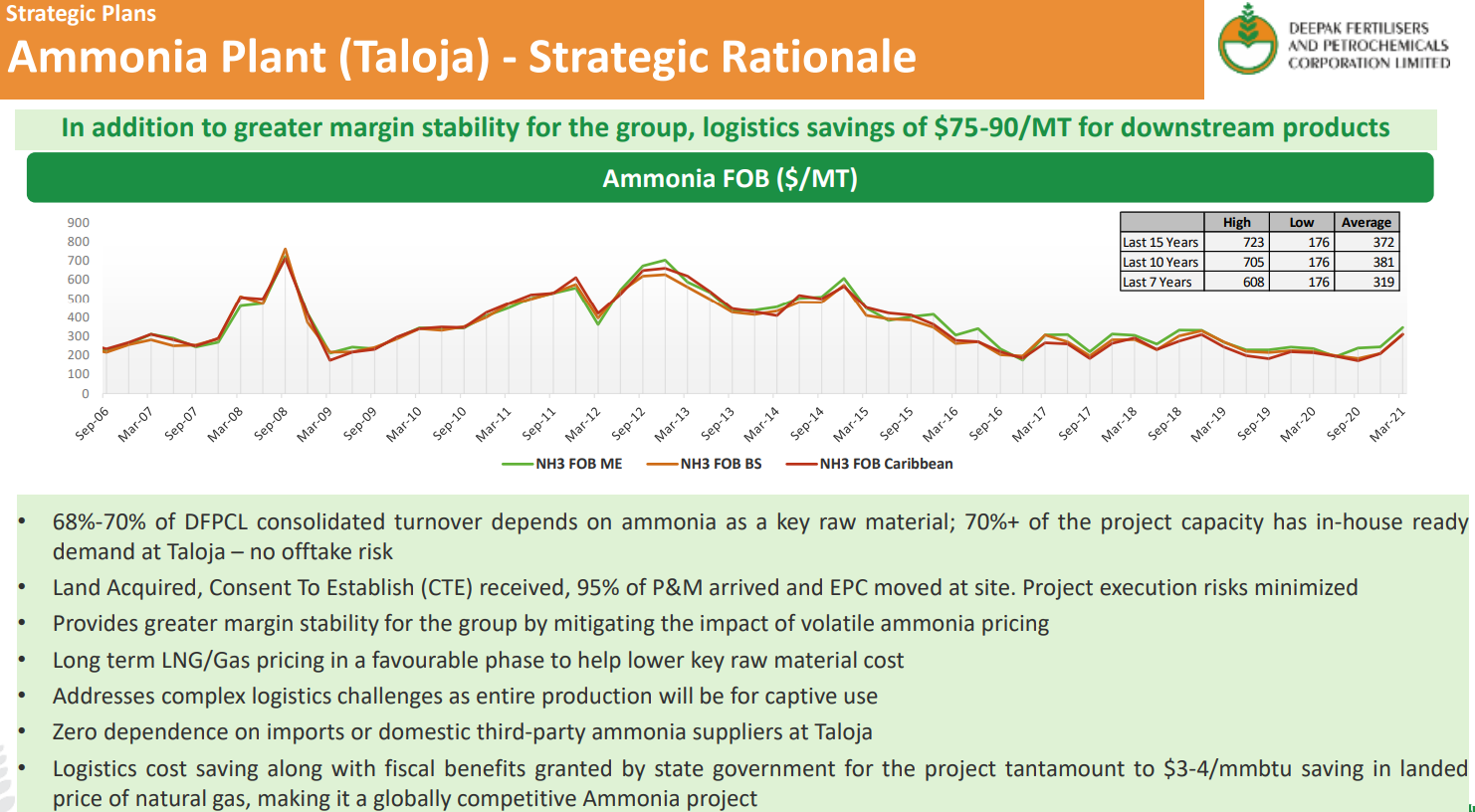

There is another interesting thing happening with the business as well. They have embarked on a mammoth Capex, maybe even more ambitious than what Deepak Nitrite did with Phenol.

Ammonia is a key starting raw material for end products that are used in a lot of sectors from mining, paints, fertilizers, dyes, construction etc. This is China-level capex. We haven’t been this ambitious in terms of building capacities so it is nice to see it happening, especially for essential raw materials.

Investment Thesis

-

Scope for re-rating from the current 7 P/E and 1x sales (Chemical business alone has a sales of 3200 Cr and market cap is 3000 Cr) to something better - Deepak Nitrite for example is currently trading at 5x Sales. Not even including the fertilizer business here.

-

Operating leverage could play out going by the current capacity utilization

-

When Ammonia plant capex comes online, the transformation of the business could be very similar to what Deepak Nitrite did with Phenol

Phenol Imports (FY21 only ppto Feb '21) - Notice the big drop in imports in FY20 and FY21 - Completely substituted by Deepak Nitrite

Ammonia Imports (FY21 only ppto Feb '21)

This is even bigger in terms of opportunity size than Phenol. Also the per kg realization of Ammonia conveys another important thing - At Rs.25/kg - this is cheap by weight which means it will be harder to compete for imports (Same logic as applies in cement at Rs.5/kg or Phenol at Rs.70/kg). Bulk of the cost would be logistics cost in these low realization products.

For domestic businesses as well, there is a lot of working capital stuck in transport which too could be reduced.

On the topic of comparison with Deepak Nitrite, the margins of DN improved from 10% → 12% → 16% → 24% → 29% and with it the stock has returned about 10x.

Deepak Fertilizer is now at 10% → 16%. So next 3 years will tell us how it actually plays out. At current starting valuations, we are probably not overpaying and the trajectory is an optionality at these valuations.

- Last couple of quarters, the management is talking about chemical value chains moving from China. So this could be a China+1 play and import substitution play

Risks:

- Large capex doesn’t always pay off and doesn’t always pay off soon. Plant coming online could be delayed. Total capex for Ammonia plant is over 4000 Cr!

- While OCF is improving dramatically, the business has to continue taking more debt to finish this ambitious capex. While this would have been frowned upon and seen as highly risky, in current low interest rate environment, if the business can generate good returns over the risk-free rate, it could in fact work out as a positive (World is flush with cash with less avenues for profitable investment)

- About 77% of promoter shareholding is pledged

References

Investor presentations Q1, Q2, Q3, Q4

Disc: I have positions from 220-290. Am a novice and could have made several errors. Please do your own due diligence.

Update: Looks like the pledge is not really a pledge to borrow. It is a non-disposable undertaking (NDU) provided by the promoter to IFC for CCDs issued to a subsidiary. Company clarification here.