Thanks for sharing this vikas. I completely concur with your views that this is a good investment due to sectoral tailwinds, despite this not being a great business.

Excellent results posted by deep ind for this qtr . Topline 75cr, NP 23cr and eps of 7.74. Simply brilliant

There is an other income of 7.40 cr though this time around

Result are average this time aided by lower tax out go (20%), other income (7 cr). Operating margins have taken a beating. Average result to be honest. I was expecting 80 cr topline with margins of 55% as guided by the management. Would be important to understand why margins have suffered so much.

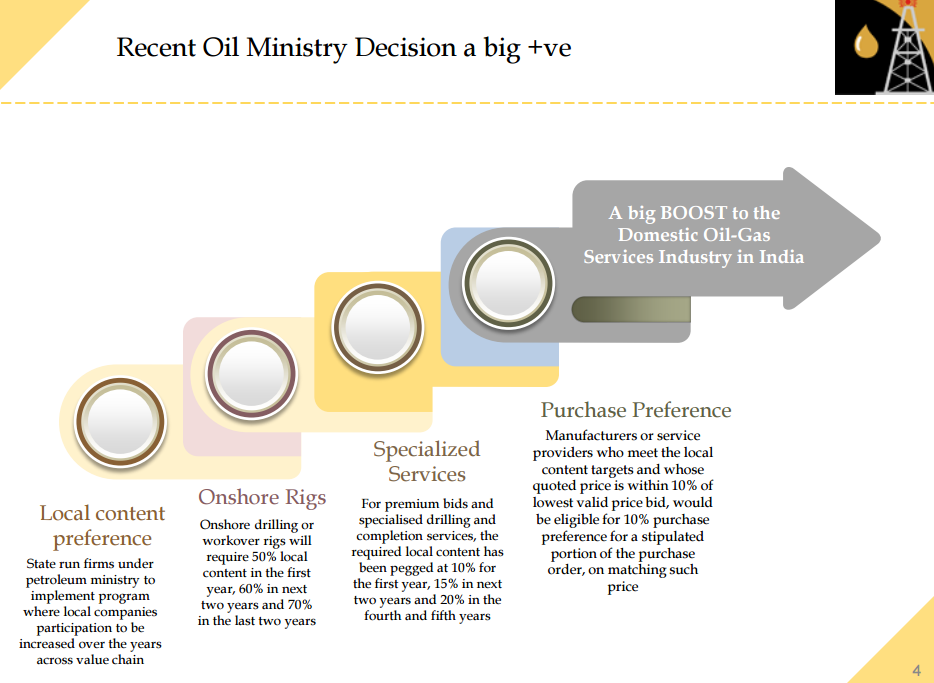

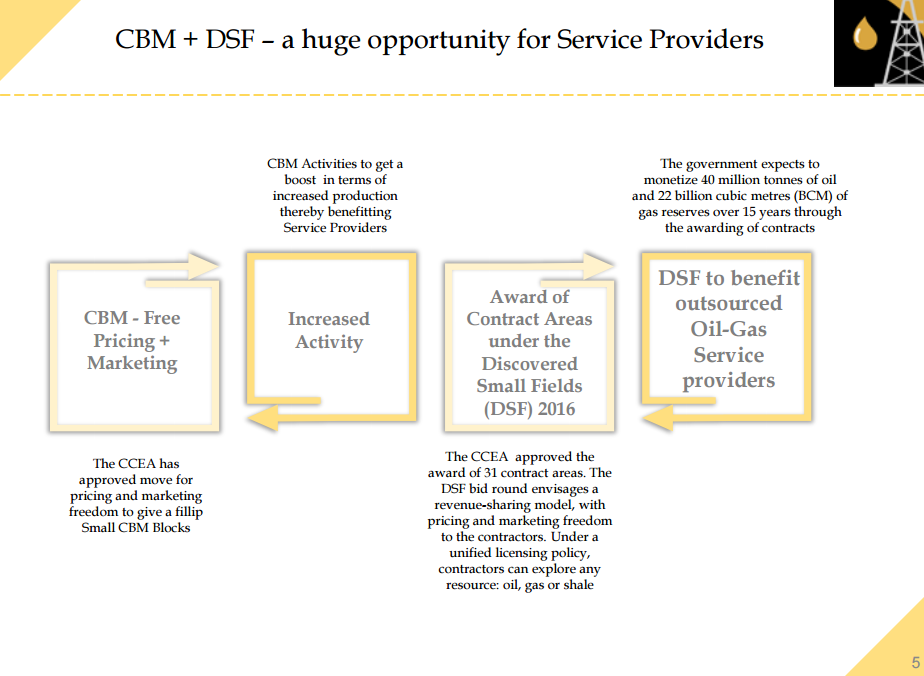

The story is getting better every day…Below 2 slides from the presentation boost the confidence in the story.

Disc: invested

2 Likes

To me these are good results. Margins are down this quarter but for the full year margins are similar to last year.

We need to watch the trend for few quarters. If this continues then this is a worry.

In fact Pat margins are up for the quarter and for full year.

This is a high growth story in near to mid term available at very reasonable valuations.

Thanks for the concall summary. Few questions if you can help answer -

-

Was there any discussion regarding tax outgo for the qtr? It has fallen substantially…

-

Also, one-off year end charges (4.5 r)…what are these specifically? Will they repeat every year?

-

Do they have some kind of insurance for any untoward accidents happening at the sites? Or for instance, the delays in delivering some equipment cost them 2.5 cr. Won’t it be sane to have some sort of insurance for such events?

-

Regarding dehydration business, competition is kicking in and there will me pressure on the margins going forward. They might deny this, but we have to read between the lines. What is eye catching is - “we will be able to maintain Ebidta margins of 55% on the current order book”. Meaning, going forward, margins might decrease.

-

I think there market share in dehydration business going down from 100% to 60% means they have lost some contracts they had bid for. Any information on who else is competing against Deep and have won those orders? Won’t this mean they will have to bid aggressively going forward? Or i am getting this wrong, and they have not bid for the contracts which resulted in their market share reducing.

Dehydration business is the key here going forward as is evident from the ONGC commentary as well. And such high margin business is going to result in competition kicking in at some point in time. May be happening already…

2 Likes

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/ab611bcd-0f4a-47c0-8f64-f566278566c1.pdf

8 cr other income added, in this revised filing. came out around noon yday

Show cause notice fro ONGC on some of the contracts. Feel its more to pacify other bidders than anything else. Here’s the clarification from Deep

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/7ca734ac-3634-43f3-9c11-37c5dd6684b9.pdf

What’s the call guys. Should one continue to hold deep industries with the sword of delisting hanging on its head ??

1 Like

Deep has got High Client concentration. Most of its dehydration and compression business comes from ONGC. Also, most of its order book of 750Cr consists of contracts with ONGC. If the worst fear of blacklisting by ONGC comes true, it would mean doomsday for Deep. Deep is working with a government company. This can go either way. Either it would be able to come out of this unscathed. Or if some bigger player is behind the accusations, the above mentioned risk might come into play.

I would request senior investors who have tracked this industry since a long time give their inputs regarding what such show cause notices mean and if its really something we should be worried about.

Disc: Invested.

I exited my position completely. ONGC is their largest client and if they are found on the wrong side then there will be severe impact both on the existing as well as future orders.

I am ready to jump in and buy at 20% higher prices once the issue settles down in favour of Deep.

Regards,

Raj

3 Likes

Holding onto this and bought more today. These things keep happening in govt. contracts and the issue will get settled quietly.

1 Like

Could it be another Shiv vani? lot of similarities…

Sold 75% of my holdings in deep today at 285. Would add back if the allegations made aren’t true. No point hoping! Protection of capital/profits is a priority.

I believe deep being only among few players providing services in the oil dehydration n compression segment, something w’d work out behind closed doors. Claims bout delisting…the way promoters have been raising their stake were asked last year about this…they skirted the question.

Anyone got the article link which is mentioned in the bse announcement?

There is a tug of war going on within ONGC over how to handle the problem with Deep Industries.

A direction by the vigilance department to take action to invoke the contract and take necessary steps to blacklist the company.

8But this attempt was fobbed off by senior ONGC personnel on the basis of the argument that more information and documentation would be needed before the last steps are taken.

8So far the evidence seems to point against Deep Industries

8ONGC has now decided to appoint a senior level officer to conduct an investigation

Find out more on the allegations and counter allegations circulating against Deep Industries

Deep Industries Ltd calls itself a leader in the gas dehydration business. It has a big chunk of this business from ONGC.

8But the company is now facing very serious allegations of misdemeanors in a set of ONGC contracts

8Highly placed sources said that there is move now to blacklist the company if further investigations find the misdemeanors to be true.

8But the company is lobbying very hard, and it has been able to elicit the support of a few key directors in fighting the move by the rest of the company to blacklist it.

Sold @ 260. I agree with you @Mridul that there is no point hoping. Such things can go anywhere. No doubt this company has bright prospects in absence of such risk factors. The management is capable and will try it best to come out of this after which it should be an attractive buy. But for now, I don’t want to take on a uncertainty with huge downside potential.

Here you go…

Scroll down and you will find part of the news. Full can be accessed only on subscription.

Regards,

Raj