EV/Tonne measure of Deccan cement is far cheaper than other players operating in the southern region.Also it has access to captive limestone in Telangana.Considering that 1)the value of Deccan cement is much less than cost of setting up new capacity 2)capacity utilisation of players is gradually crossing 70%

doesnt Deccan cement present an attractive acquisition opportunity for the bigger players?

Any insights? @jitenp @basumallick @james_kerala

Deccan Cement EV/tonne is 32$. Company has almost 0 debt. Southern region, especially AP-based players have had a tough couple of quarters due to freeze in infra projects by new govt.

Disclosure : No transaction in last 30 days.

2 Likes

hi Jitenp,

Would like to get your views on the Cement industry dynamics in AP. How the prices and capacity utilization is shaping up in last 2-3 months?

Thanks

Disclosure: Tracking Cement Sector

massive margins in Q121 for all south players. 2.5x Ev.Evitda on this quarter annualized; $20 EV/Ton, why are promoters not buying themselves in boat loads is what I cannot figure

Hoping to revive discussion and get boarders view on this.

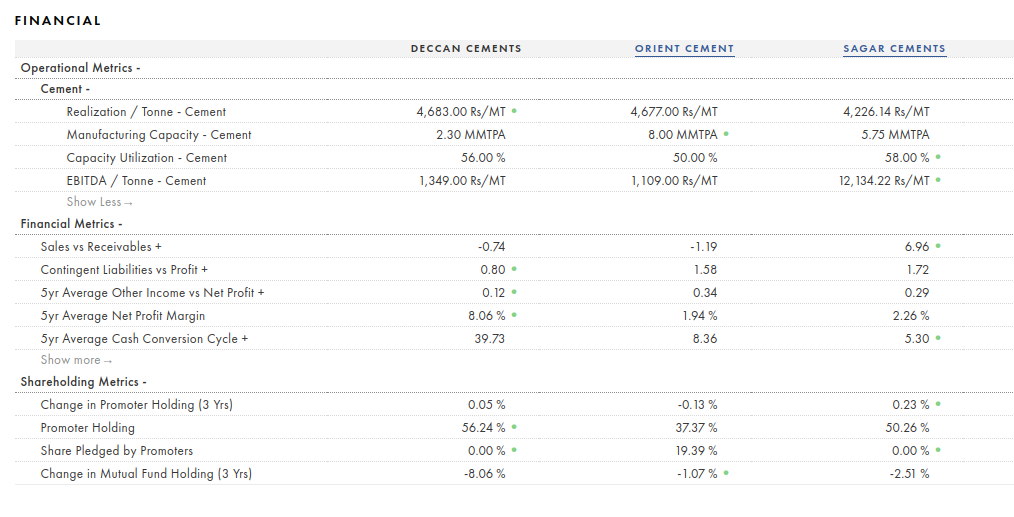

Been reading up on this co last few days and in comparison with peers, Deccan cements is at much much lower PE and fares better on below :

- Negligible debt

- Steady profitability

- Decent Return ratios

- Consistent and higher promoter holding - no pledging too.

MF holding seems to have gone down in past quarter and not sure if there are any issues / red flags. One thing, I noticed, is their Capacity is lowest 2.30 MMTPA but has room for higher utilisation (56%). And low debt can help add further capacity to aid growth.

With Infra and promising beginning fo upward cycle, is this an attactive investment? Am i missing soemthing Mr. Market knows!?

Also, read of issue around mining but not sure how authentic it is and imapct it has on future of company.

Disc: Not Invested.

Screener - comaprison with Peers.

Yes, seems like a very good value bet. They announced doubling of capacity recently. Very cheaply priced at EV/EBITDA of 3 (CMP of 410).

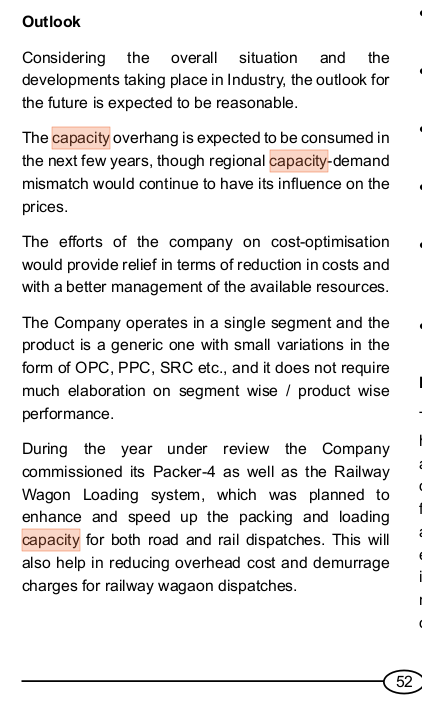

On page 52 of the annual report for fy20, company is taking about capacity overhand and situation could improve in couple of year.

Can you help us by point towards the source of your info that company is doubling it’s capacity?

1 Like

Attached, outcome of the Q3 results board meeting.

Also note the capacity utilisation fell in FY20 (due to abnormal monsoon 2019(FY20) & Covid impact in March 20), but was higher in FY19. And current utilisation would have shot up higher as evidenced from market trends. Most companies go in for capacity addition as utilisation level start reaching 85-90%.

1 Like

Hi, Came across this company during searching for cement companies, anyone attend AGM on 22nd September? More than doubling capacity from 1.8 to 4 mtpa, expected by Jan 25, capex is nearly double current market cap, Let me know if anyone is tracking this

1 Like