Nice article. Hope you move to a dry state for higher output

Its a nice small company, but no case for a concentrated bet. All other comparable companies mentioned make equal investment case. So spray and pray across the segment may be better approach.

Thats rear view investing…doesnt work in real markets.

Net cash flow is negative due to aggressive repayment of loans ahead of date.

Tax paid is low in past ( point agreed, will need to check why ) but for q1 they have paid 4.5 cr of tax on 18.5cr PBT, which is 24.3%.

As company becomes debt free, interest coverage ratio will be infinite ! Also, with debt payback and increased profitability, return ratios will see significant upside.

My take is simple:

For 300 cr you own 2.3 million tpa (2,300,000,000 kg per annum)

for 30 cr you own 230,000,000 kg per annum

for 3 cr you own 23,000,000 kg per annum

for 30 lacs you own 2,300,000 kg per annum

for 3 lacs you own 230,000 kg per annum

So if you buy 3 lacs worth of shares, you personally own a 2,30,000 kg per annum capacity fully integrated cement plant personally ( with captive mines and power plant ) ! that has to be worth owning and cherishing !

I had a difference of opinion on few points and hence stating them with due respect:

Cement firms are normally valued on an EV to Capacity basis and EV to EBITDA basis and looking at PE might not be the right way to look at a cement company. (However size of the plant, geographical location, mgmt. quality, etc.,. should be considered as well).

In cyclical businesses earning swings can be very wide and hence I am not a big fan of looking at EPS or average there offs and I think that one should take a broad macro call on the economy (Earnings swings is also one of the reasons coz of which cement companies should not be valued on a PE basis). So if one feels that the stock might have bottomed out and macros will improve resulting in a sustained period of demand off take then one should invest. (one might like to consider other supporting factors as well while taking a call, say company with better margins, low debt, etc.,. in the sector per se) I personally prefer going with decent sized players in such an industry but if there is good undervaluation in a small player with good visibility of earnings ahead, reducing debt, improving margins, etc, etc.,. then I don’t mind a small cap/small capacity player too.

ROE and ROCEs can fluctuate too coz of the nature of the business (Shree maybe an exception and hence has been rewarded over the years, although I don’t have a view on it. Just stated this trying to pre-empt just in case Shree might be quoted as an exception).

Discl: I am an amateur investor and might be biased in my views as I am positive on cement as a sector since last 2 qtrs. Apart from positive commentary from some mgmts. at a ground level have heard from transporters about increased cement movements and some government spending etc.,. actually kicking in.

Not invested in Deccan but Invested in NCL industries since sometime due to reasons already covered by few boarders in NCL thread and due to my views expressed above.

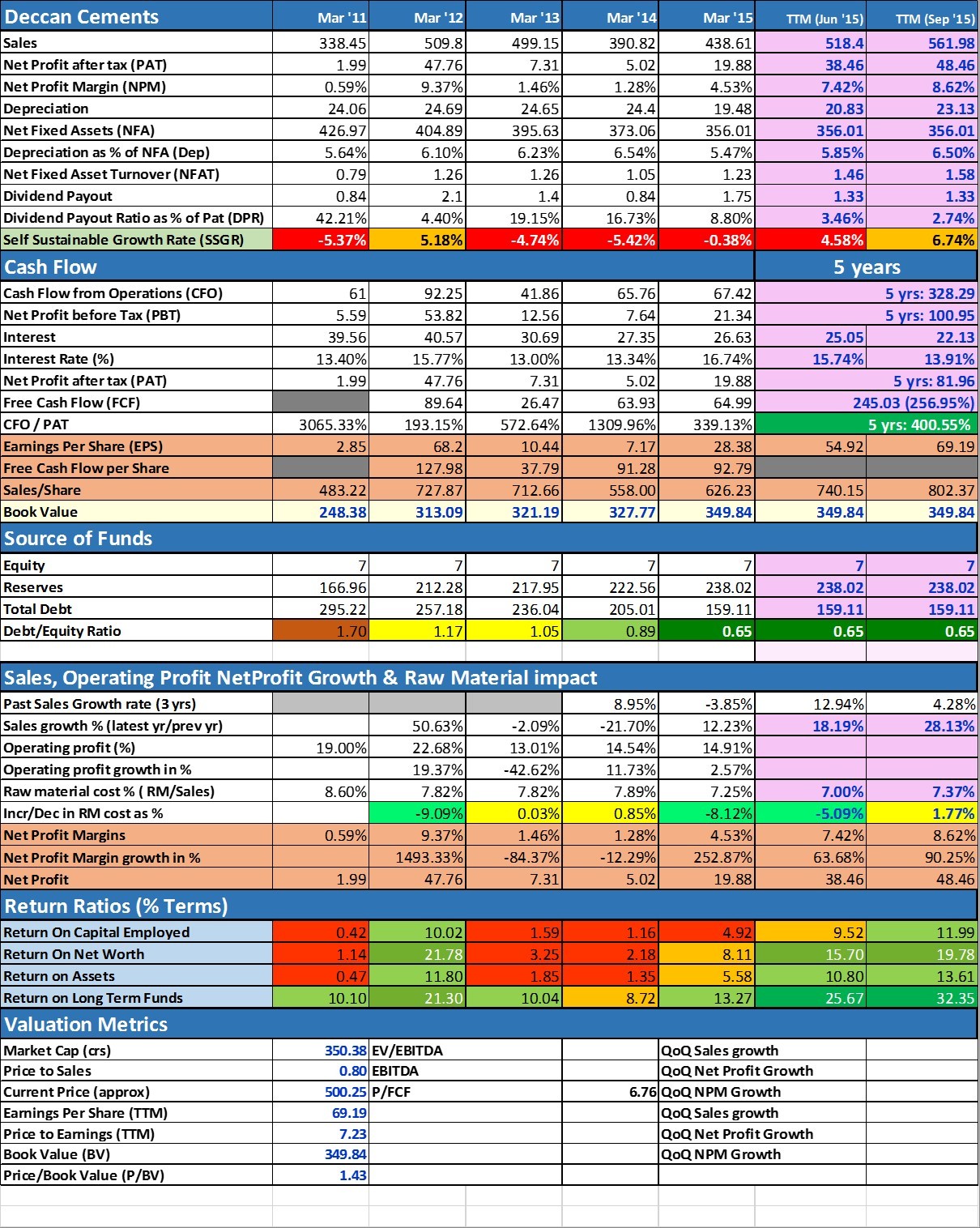

Deccan Cement released their q2 results today. A great set of numbers and puts the company firmly on track to where we want to see it in 2018.

Salient updates are ( all numbers being compared on a y-o-y basis )

sales up from 109cr to 153 cr , up 40%

EBITDA up from 16.95 cr to 34.84cr , up 105%

EBITDA margins up from 15.55% to 22.77% , up by 722 bps

PAT at 15.43cr compared to 5.43cr , up by 184%

finance costs have dropped from 6.77cr to 3.85cr

LT borrowing down by 20 cr in H1

Q2 eps is 22

H1 eps is 41

promoters pledge continues to be zero

The company continues to ignore investors clamouring for a bonus/stock split…which in my view is the right thing to do. Equity is still only 7 cr. Its still 10 paid up.

With the best quarters of the industry yet to come, company on track for a great year ahead.

CMP when posted : 500/-

Mcap when posted : 350 cr

Disclosure : own the stock , currently 16% of portfolio. Will need to trim position if the stock rises substantially from here to maintain portfolio balance

Seasonally this is the weakest quarter for cement companies due to rains & slow construction activity. If company can deliver such strong performance in this quarter with EPS of 22 then there is high probability of doing 25-30 EPS per quarter in the coming two quarters.

Looks very nice bet with almost negligible downside given current circumstances.

Yes, it seems in Jun-15 qtr it got fuel expense benefits. Generally their fuel expenses (to sales) ratio is between 27-29% but in Jun-15 qtr it was in 21% which gave it approx 11-12 crs of fuel savings. This qtr is back again to normal levels, still profits are up. Need to demystify it

There is one more company - Panyam cements (located in Andhra only) which is doing phenomenal like other cement companies in south. I think it is still undervalued. NCL industries and deccan had their rise. Panyam has its results today. The results are expected to be good - June quarter was also good. We can think of beting on this stock. Mgmt shares were pledged and some of them have recently been released.

Disc: Not invested yet. Much interested in it. Analysis going on!

Further, answering to your concerns raised on rise of Deccan and other companies - are you expecting that the stock will command PE more than 6 or 7 ???

Its really a fancy story out there which is not sustainable. Its good to bet, earn and come out. Its not like ultra tech which commands PE of 38 !!

I hope I have answered to all your concerns raised above.

Check the performance of these small companies during the times of low demand. They were squashed. High debt, low margins and poor mgmt (main reason). It is not the company which has outperformed or has made a turnaround - its the industry in south which has improved. Let these companies flourish for sometime.

Cement stocks are normally not valued on a PE basis. And are valued on an EV/Ebitda basis + Ev/Tonne basis (which is compared with EV/Tonne to set up a new plant). Also good to apply a discount on both the above parameters for a small capacity company (discount on say for e.g. to EV/tonne to set up a new plant). Current EV/Ebitda and EV/tonne should be compared with the above discounted value to arrive at a conclusion if it is undervalued.

Add to that other things like amount of debt component in EV. So company with minimal debt in EV is a better choice. Also add better to have a player with good margins and a company that is reducing debt constantly etc.,. (Deccan has been reducing debt constantly). So say a company that is reducing debt constantly would have a falling EV which will make its valuation better and this would be compensated by a rise in market cap of the company.

Throw in the scope of ramping up capacity utilisation depending upon current capacity utilisation.

Other things like WC cycle etc.,. can be considered as well while comparing with other players. How does receivable picture, credit period given, cash flows etc.,. look on comparison? For e.g. NCL sells mostly to retail and not to govt. which results in better receivables cycle as retail mostly would operate on cash or with minimal credit cycle.

What is the current capacity of Panyam vis-a-vis Deccan or NCL, etc.,.?

How does Panyam fare with Deccan, NCL or other small players on above

parameters?

Stating the above on the basis of my limited understanding.

I also do not expect a good PE levels or PE expansion for cement companies going forward. Here are some other comparisons

Panyam is 157 crs (TTM, till Jun-15) sales with MCap of 158 crs.

Deccan is 562 crs (TTM) sales with MCap of 391 crs

Panyam has done 0.32 crs of profits (TTM, till Jun-15)

Deccan has done 48 crs of PAT (TTM, till Sep-15).

Panyam has D/E ratio of > 5 with -ve reserves (-1.76) on Equity of 16.02. Debts 3 yrs back was 65.28 crs (Mar-13) and currently it is 81.48 crs

Deccan has D/E ratio of 0.65 with reserves of ~160 crs on equity of 7 crs Debts 3 yrs back was 236 crs (Mar-13) and currently it is 160 crs

Panyam has started showing good numbers from last 1/2 qtrs where as deccan has done it for 6 straight quarters.

Rest of the comparison is done by hrfacebuk.

I for sure think that market will value Deccan more than Panyam which it is currently doing it and the gap may increase going forward if they both give same kind of performance going forward.

Disclosure: Had Panyam from 55 levels when one fund was selling but booked 75% profits and moved to Deccan Cements. This is not a long term hold is I believe due to cyclical nature. Will decide holding based on south cements conditions.

Amol Chavan - I agree with you completely. But i see not much growth in deccan which i see in other cement companies. Deccan is more or less steadily growing Q on Q. No doubt it has increased its EPS and operating margins to a certain level. Panyam in comparison to deccan has almost doubled its EPS in June compared to march quarter. As more and more positive news comes about Panyam - release of pledged shares and doubled EPS sustained for sept quarter also, repayment of debts, etc. stock will command more price.

I am purely betting from a medium term perspective. I am not interested in keeping deccan or panyam for long term in my portfolio.