DATAMATICS Clarification of Rumor: The Company would like to clarify on the rumors in the market regarding the termination/cancellation of a big partnership in the US. These rumors are false and baseless and merely public speculations.

Also some rumor… which datamatics clarified on

2 Likes

Well this space has been dormant for a while, but this week I had attended a session -

28th September,2023 - Arihant Capital meeting with Management

Rahul Sir from Management:

Lines of Business

Digital Operations

- Digital Experiences (DE)

- Focuses on front office - interacting with customers of customers (not exactly customer support) - mostly on the cloud, use of Al for survey programming

- Implemented Generative Al - for creation of the survey forms. Eg : A company selling awards, Al to deploy read articles - where the award is getting provided ( categorize accordingly - and then categorize the award - turnaround time has decreased from 1 month to 3-4 days. And the use of employees have reduced from 300 to 100

- Digital Technologies (DT)

- Couple of Pockets - HyperScalers ( Cloud, ServiceNow, SalesForce, etc)

Product improvement for customers

What takes 2 months, now 2 weeks

- Investing heavily on robotics - used in operations and experiences. Selling as 3rd party licenses. Margins in the range of 16-18%. Due to investing margins look suppressed. And are not capitalizing on these.

- Automatic fair collection(AFC) - 30 products globally for metro fair collection ( implemented in HK, now in India they are doing as prime contractor in India - Mumbai, Lucknow. Memphis in US. Will bid more for US and India ( would be largest player in India)

- 50k$ → 150-200k$, now half million to million from orders

Cracked a few good logos - they will all scale to multi-million dollars.

- All new customer signs small, and then start scaling substantiatilly ( like sony )

- Fringe Benefit - like some customers don’t want to buy but want to outsoursce it

- No slowdown has been observed as such, no customer has said so. There pipeline has increased

Q/A

-

What is driving the growth and what factors would take place for datamatics and data-analytics. Where is DMG leading in 4 years view:

- 14/15% growth for this year, going forward 15-20% - some uncertainity in the field due to Al causing disruption (depends which side you are on). Mgmt is confident about there outlook for next 3-4y. Margins should improve because of the investment being made for which margins are squeezed but they will start getting improved (18-20% on DT, on Experience and Operations - it would be north of 20-22% )

- Cognizant and TCS are very large and to grow 14-15% is big. So matter of the size of scale. Large spends not taking by them due to recessionary fears.

- Talking to companies for M&A

-

Journey of datamatics, 3-4 years back we had all the offerings ( were working on robotics and fair collection)

-

All AFC are greenfield capex for India and they are price sensitive - strategy to go aggressive ( lower pricing to capture market share, which has lead to market share - now doing price correction to capitalize on there brand - so margins should improve) - 200-300 Cr for single project

-

On the robotic side - tool for a product improvement on digital experience - When it was successful then took to market (before was a tool, now they have made it as a product to sell - more user friendly - implemented Gen AI - lowcode/noCode - seeing very good traction) - Fringe benefit: As per the hockey curve they are on the lower curve and can see high growth

-

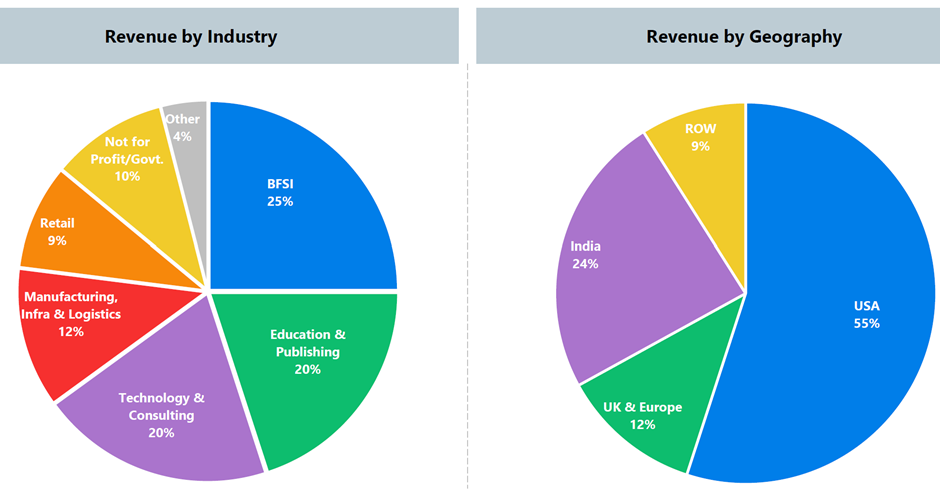

Usecase from Digital Technologies(DT) - Growth would come from HyperScalers - American and European markets - 25% from India - pivoting towards abroad due to pricing better - work on salesforce & implementing lowcode/nocode - providing global support

-

Will Al be disruptinve in all verticals

- Moving very fast and disruptive on industry - early mover benefit would be for DataMatics (feedback of top 1% on the working of Al - so they will disrupt)

- Have to make Al more accurate for use of corporates compared

-

Implement salesforce - say it in english and then it simply creates chatbot and creates the task - showcases prompts to the salesperson as to what to say to the customers.

- Read legal documents, a lot of effort and within 5 seconds give the answer and the reference dates, also gives questions to ask

- Email feedback, Al reads that then understands, and performs the action needed and then addresses back to the customer over email (what takes 2 weeks now does hardly 5 mins - leads to customer satisfaction)

- Al to generate images and videos, translate the audio from english to spanish on the fly which helps customers understand and provide an ease to do business

- These are hyperscalers, under the umbrella of DT. As in salesforce - they have implemented Al which has enhanced much more on the Al experience

- Digitised the Blr Airport - implement Microsoft platform

- Project with Zians Bank - acquired more 5-6 banks - they all have more mortgage - 40 millions to go through, Al helped and recategorized them to 219 categories and what are the supporting documents is needed

-

Focusing on RPA - as to add products and Intellectual Property ( IP has a residual value which is a huge value - enterprise value increases - gives you an edge)- Customer feedback has been exceptional.

-

Growth would come from there subsidiaries which were more than 51%, but now they have divested couple of those as they were dragging there performance.

- Focusing on high growth areas and removed the underperform

-

How are you hiring employees who know they are in high demand

- Core team is from a lot of years - which has been stable - and also large scale training are taking place. b.

Senior people have ESOP’s, not all.

-

Risk as big corporates on small project -

- Big guys are chasing, but then as Datamatic shows Proof of concept there win rate increases. Sometimes customers don’t want to go with the large clients probably because of hand holding which they value.

Feel free to correct me where I have missed any pointers.

Datamatics Global Management Call notes.pdf (5.7 MB)

I have also uploaded the pdf notes - If someone want’s to refer that

13 Likes

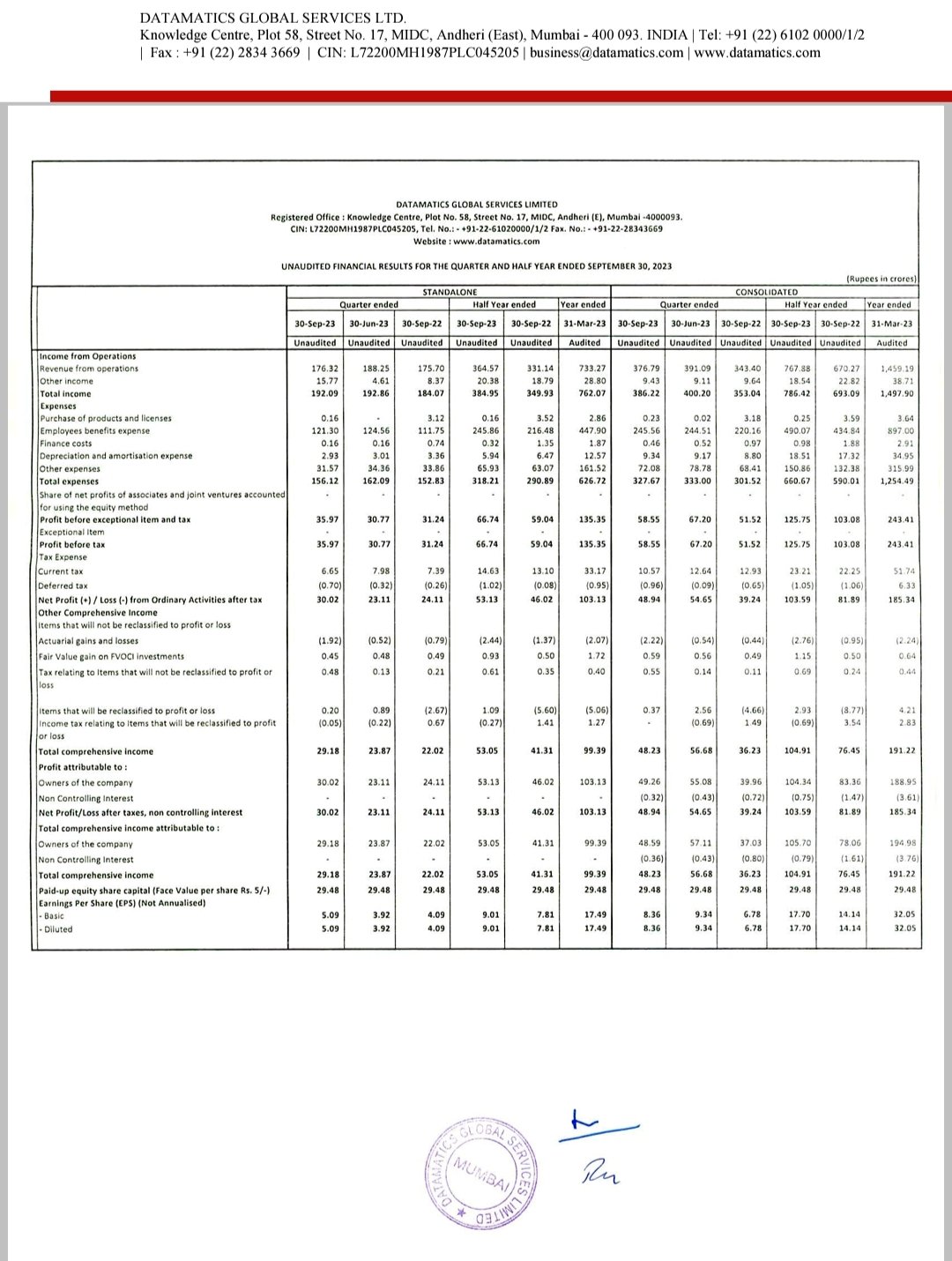

Datamatics quarterly results Q2FY24