Maybe it does but db income statement doesnt show it over last 5 years besides newspaper revenue traditionally was from advertisement. I don’t know if companies still use newspapers for job advertisement or their advertising budget will increase so that money spent on online advertisement is over the current spend or will it be a portion from the current spend

It has grown. Please see above Recently there is slower growth.

No business grows in a straight line. Clearly circulation is not going down drastically => death of the business is greatly exaggerated

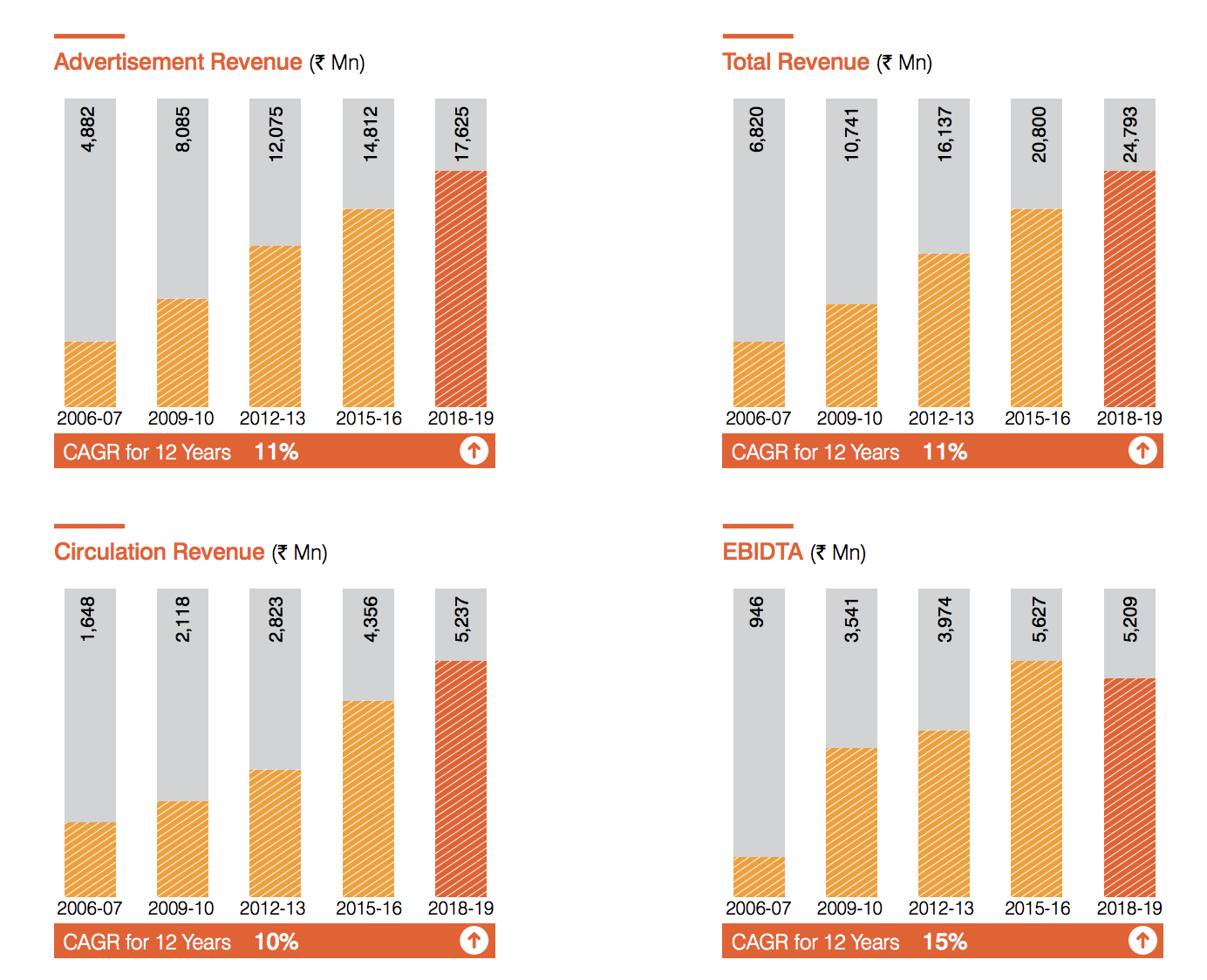

Source: 2019 Annual report

1 Like

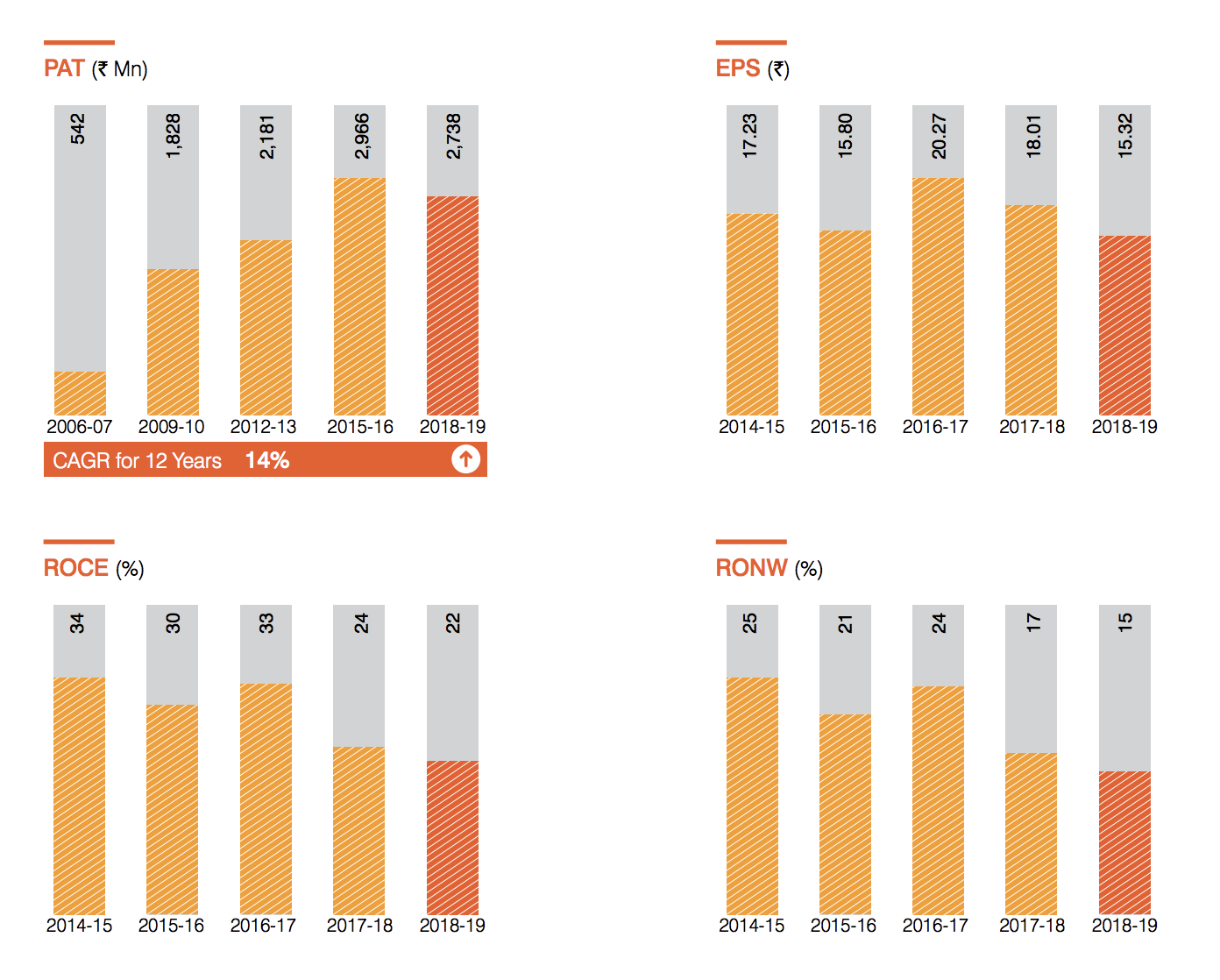

Why is eps and roce not growing in line with revenue begs the question if revenue was grown at zero profit or loss however I am not invested, just my initial observations

Happy investing anyway

One of the major overhang over the stock seems to be coming from pledge shares. 40% of shares are pledged to lenders. Promoters own 71% of shares, which means ~28% shares are pledged. The pledge is for group entity company Writers and Publishers Private Limited (WPPL).

As per care rating update on May 29. Although, the quantum of debt at WPPL in absolute terms has declined on back of repayments made, the share pledge percentage continued to surge with decline in share price of DBCL. As on May 22, 2020 the number of promoter shares pledged as a % of their total shareholding stood at 52.24%. The declining share price has also resulted in overall market capitalization reducing from Rs.3,269.97 crore as on March 31, 2019(share pledge was 39.88% then) to Rs.1,047.10 crore as on May 22, 2020. Management has indicated (on May 29, 2020) that they have made certain prepayments towards the debt raised by WPPL, however, despite the prepayment, percentage of shares pledged by the promoterscontinues to remain elevated.

But as lock-down eases slowly and company being operational mostly in Tier-II and III cities, there is good chance of faster recovery of ad-business. However it mayn’t go to the same level very soon due to reduced economic activity.

3 Likes

Even if it doesn’t go back, I am happy with > 10% dividend every year

Recent interview of Girish Agarwal of DB corp. Aired on 30 Apr 2020.

Some highlights:

- News papers have not been read so much in metro due to concern about corona virus spreading through newspaper. What is the true picture?

Ans - This is a metro phenomenon, specially of larger societies. Societies did not allow anybody external to society to come inside during lock-down days. In other parts of India, specially in Tier-2 and Tier-3 cities, circulation number is back to 75-80%. The rest 20-25% is due to offices, shops, airports and railways being shut. Also they are not able to deliver to some towns, where they were dependent on railways. - What would happen to advertisement industry in future?

Ans - There are two types of companies. Companies who derive 80-85% of revenues from Tier-2 and 3 cities (for example two wheelers) and others who does have more metro concentration. Tier-2 and 3 cities should recover faster than metro because of one metro being shut for more time due to larger number of hot-spots. Another critical factor that local advertisers would come back sharply than national is for a local advertiser, advertisement is to get sales boost at the end of day, it is not for branding. A coaching institute or real estate company or two-wheeler show room would give an ad, see if there is sales calls at the end of day. If yes, he (and other advertises) goes for more ad. - What is the trend of digital readership of news paper and how are you looking for monetization of that?

Ans - We have seen a 150% jump in digital readership to website and apps. People want to know more about events during the day and hence once they read newspaper in morning, they want updates during the day for news. Monetization of digital readership is far away (>1-2 years). Currently the focus is on acquiring the customers. Unlike metro, where few people are interested in e-newspaper using pdf. the trend is not same across the country. People want to use apps and get updated with news continuously. - Why has advertisers not valued digital readerships vs newspaper readership?

Ans - Advertisers look newspaper as engagement, but think digital as commodity. They think digital as how many eyeballs I can get and who gives me most eyeball (read fb, insta) and go for that. Overtime, advertisers would recognize that they are not looking for any eyeball (out of context ads) versus a matured eyeball from a credible source. - Is it a challenge to get Indian news readers to pay for news?

Ans - Not at all. Indian readers are paying approx. 130-150 per month for reading a newspaper. This cost is same as to subscribe for a large number of TV channel. Reader is not shy in paying but they look for good news. (Value for money category). Post-covid, there is a pretty good chance of increasing subscription revenue by 10-15% due to price hike. - Disruption has occurred, what would be changes in industry?

Ans - Some kind of consolidation might occur in future. There are problems at many print media companies. But the consolidation is not happening. One because newspapers are not capital intensive businesses, especially for old players. Another is the power newspaper printing brings. - Not looking for any major layoff.

- Government should help other businesses, that would automatically help media companies.

- Radio business is facing tougher time due to reduced listening and subsequently reduced ad.

4 Likes

Q4 and FY2020 financials and conference call notes:

- Q4 financials: Revenue 487 Cr (-17% YoY), OPM dropped to 14% compared to last year 18% and last quarter 24%. PAT 24 Cr (-66% YoY).

- For full year: Revenue 2,224 Cr (-10% YoY), OPM in the same range of 21-22%. Net PAT: 274 Cr (same as of last year).

- Increase in depreciation by 22% YoY due to adoption of Ind AS 116. The nature of expenses in respect of operating leases has changed from Rent in previous years to Depreciation for Right-of-use-assets and Finance cost for interest expenses on Lease liabilities. Don’t understand fully this accounting part.

- EBITDA margin stable over year (even though there was revenue loss) mainly due to reduction in newsprint price (-11% YOY). Same is true for PAT margin.

- Revenue breakdown:

- Advertising revenue: 1564 Cr (-11% YoY)

- Circulation revenue: 512 Cr (-2% YoY)

- Radio advertising revenue: 139.1 Cr, EBITDA of 43.1 Cr with margin of 31%. PAT 198 Cr with margin of 14%.

- Impact of Covid-19 on news paper circulation:

Ans: Sudden drop in circulation numbers (55-60% of pre-covid circulation number) in last 10 days of March (initial lock-down days). Due to 1) Closure of major cash counters like railway stations, bus stations, book stalls. 2) Copies to offices and shops got impacted. 3) There was fear among people that newspaper spreads corona virus. But they ran the campaign to clear the myth and from April beginning, the circulation number is back to 80% of pre-covid level. Remaining 20% belonging to reason 1 and 2. - Impact of covid-19 on advertisement

Ans: April had 15% advertisement of last year base. May the number reached to 20% and June might go to 30%+. Q1 FY2020 should see a 70-80% drop in advertisement revenue. As company serve to Tier-II, III, IV towns, semi-urban and rural areas, and most of these areas are not in red zone. Advertiser is focusing on these areas and there might be faster revival in those areas as compared to metro. Government advertisement has come back. - Cost cutting efforts

As advertisement is less, number of pages has been reduced in the newspaper (but not the cover price). Apart from print expense, there are 1000 Cr expense, would reduce this by 10-12% and most of reduction would be sustainable. Newsprint price further went down and in Q1 this year it would be Rs 36,000/ton (12% reduction from Q1FY20). Due to page reduction and print cost going down, circulation revenue should be able to cover newsprint price. Approx <50Cr loss is expected by management in Q1 FY 2020. Normally a paper has 20 pages, approx 30% of which is ads. 5 pages ad, 15 page content. As ad went down to 25-30% of base. 5*30% = 1.5. Number of pages which can be reduced be 3-4, leading to a drop in newsprint cost of 16-20%. Overall cost drop of approx. 6.4 - 8%. - Share pledge issue:

Overall promoter debt has comedown from 300 Cr to 160 Cr. We should be able to pay this within next year. Due to sharp drop in share price, pledged shares increased to 34%, if not it would have been at 15% level. - Digital strategy of company:

Consumption of news has shifted from whatsapp to News app, due to increased fake news in whatsapp and due to better content at apps. Direct traffic to app increased by 3 times (pre-covid) and average time per session is also higher. Company has appointed a dedicated digital media team for this. Exact strategy discussion could be possible only after few quarters. Currently focusing on creating great user experience, engage readers, so they spend more time, and once the critical mass is reached, we would look for monetization model. In next coming years, we are looking for a 10X increase in volumes of app. - Shift in advertiser’s preference from print to other medium

Ans: For our readers, there has not been major shift from print to digital, due to which we believe that they would come back. As some of them are coming back now and have not come across any advertiser who is saying I am going to stop a particular medium. Every one tries everything. - Receivable numbers have not spiked. Company would announce dividend based on whatever cash we have. Past payout ratio of 64% would be maintained.

- Synergy with peer group (Jagran mentioned about it in their concall)

Ans: Actively engaged with peer group on leveraging distribution network as well as printing facilities, but do not expect significant savings on this max by 1 million dollar. - Competitive intensity and acquisitions

Ans: No one is looking to get acquired. As market is tight, advertisers is now choosing to go with one publication having maximum reach and is leader. There has been some scheme run during April to June by all print companies for advertisers to easily advertise. They are hoping rate would correct once situation normalizes in July.

7 Likes

Promoter has revoked pledged share of around 25lakh.

See the video below

1 Like

Q1 FY2021 con call notes:

- Q1 financials: Revenue 210 Cr (-65% YoY), EBITDA loss of 27.8 Cr, Net loss at 48 Cr.

- How things are progressing month over month

| Month | Circulation % | Print Ad Recovery % | Radio Ad Recovery % | Print business Operation cost |

|---|---|---|---|---|

| April | 67% | 19% | 20% | (16.9) Cr |

| May | 69% | 20% | 20% | (4) Cr |

| June | 76% | 32% | 30% | 9.7 Cr |

| July | 78% | 53% | 55% | 18.4 Cr (20% EBITDA margin) |

| August | 81% |

- In a recent notification by DAVP, Indian language newspapers would get 80% of the space, out of that 50% would come to bigger guy. Earlier absolute volume that bigger guys would get was 27-30%, which would rise to 40%. Small newspapers might get affected because of the regulation that newspapers who are certified with ABC/ RNI would get preference. Smaller players might find it difficult to comply.

- Average number of pages currently is 14 as compared to normal 21-22. 30% cost drop

- Segments of customers advertising:

- Automobile – did pretty well and continued performance.

- FMCG – is doing good.

- Education – worst performer. Education ad demand got shifted from April, May, June to later part of the year. When school, college admission and all opens. We might see a spike in local ad due to this during Q3 may be.

- Real state – started to come back in July, August. Assuming it to be moderate only.

- Digital monetization and strategy: The earlier stated strategy continues. Want to build a platform where users loves to spend time and so focusing on that. On the question of how the competition between different media apps would be in future. Companies seems to be going ahead with its time tested older strategy of identifying customer needs and tailoring app according to their need. Number of app users up by 4 times during Covid.

Comparing some of the other news apps:

| App | Downloads | Rating | Number of people who rated |

|---|---|---|---|

| Dainik Bhaskar | 10M | 4.2 | 225K |

| Jagran | 5M | 3.9 | 116K |

| Hindustan | 1M | 4.1 | 13L |

| Aaj Tak | 50M | 3.8 | 201K |

| In shorts | 10M | 4.6 | 468K |

| TOI | 10M | 4.0 | 550K |

| Daily Hunt | 100M | 4.2 | 1M |

It becomes very evident that DB corp may be leading the pack in term of better app as compared to a newspaper competitors. But nowhere near close to Daily Hunt or Aaj Tak. So monetizing at this stage may not be that fruitful. They have not put ad on app even during Covid time.

- Several cost optimization initiatives has been taken. But it would be worth watching how thing progresses if and once the ad volume recovers. But some cost advantages would recur.

- Share pledge issue: Currently having absolute debt of 140 Cr, would be paid in next 12 months.

- Dividend policy would remain consistent as it was earlier. Whatever cash is not required by company would be paid back.

- Girish was discussing in the call about an advertiser who was apprehensive about putting ad on paper, as he seemed to believe everyone is reading from app and so no sales would occur. Seems that was not entirely true as number of calls received by advertiser was similar to pre-covid level. Company would need to be in regular sync with advertisers to remain relevant.

- The main reason of advertisers staying away from advertisement seems to be the absence of sales. Another interesting point noted about consumer preference by Girish was consumer’s brand preference has gone down due to unavailability of the preferred item (which companies refer as downtrading). Hence he believes, once sales remain advertisers would be back with a bang to claim this loss of customer trust and firm up the preferences again.

7 Likes

This is what DB Corp said at MOSL conference. If print recovers from Covid, bears need to rethink. Ofcourse stock px is Mr Market determined

DB Corp: EBITDA will grow by ~20-30% in H2 over last year

Girish Agarwaal, Promoter Director

** We were able to recover losses of Q1 in Q2 and also have some operating profit

** H2 will be a very good period for media companies, especially print

** Advertising revenue back to 80-85% of pre-COVID levels, expect it to go to 90-95% in H2

** Confident that FY21 full year EBITDA will be ~80-90% of last year

** News print prices have softened by 10-15% compared to last year, but costs have also reduced correspondingly

** In terms of Circulation, regional dailies are back to ~85% of pre-covid levels, English dailies are yet to pick up as metros are worst hit by the pandemic

2 Likes

DB Corp. Revenue drop was only 19% in Q3, commendable given the situation. Circulation back to 80 of pre-covid. Advertisement by volumes back to 90%, pricing down 5% and thinks will normalise. I dont want to highlight the good margins, as this is a seasonally strong quarter. Key point is racing towards normalcy, which is not what markets are pricing in for newspapers. Its digial apps in Hindi and Gujarati also ramping nicely.

Average net profit over last 5 years, fy16-20, was 308crs. Last 2 qtrs profit is ~120crs. I feel they might return to 300crs net profit no on fy22.

Mktcap is 1400crs and dividend track record is top quartile amongst listed cos.

6 Likes

Hi

I have done some analysis on DB Corp which I am sharing below:

Apart from all the good stuff about the co., one must understand that the markets give a valuation only to the growth companies. Everyone knows here that the newspaper is in a dying industry. A lot depends on whether they are able to generate online revenues from the Hindi and Gujarati readers via subscription or from the advertisers for the advertisements. Currently the online news portal & app is loss making and even on the revenues side, it is very very small as a % to the co.'s total top line.

If one looks at the global Newspaper publishing listed cos, one can spot 2 stocks (which I’m aware of) on US stock exchange viz. New York Times and Lee Enterprises. I am sharing the valuations on both the stocks in the separate comment (so as to not distract the viewers from the DB Corp analysis). One can use those stocks as a benchmark to see and compare DB’s valuations. (FYI: DB Corp is trading very cheap vis a vis New York Times, but there are reasons to that, see the next comment)

Now coming back to DB Corp, the company is currently trading at ~P/E of 4x. The newspaper is a dying industry and if it grows at say, 4% every year, the stock is fairly valued.

The company did buybacks in the past at very high valuations in which even promoters participated. Buyback was done at 4x the P/B. Why at such a high price and pls check that the promoters also participated, taking some handsome gains out of it. (Don’t respond stating that the stock price was trading around those levels at that time, i know that, trying to share a diff view here.)

DB Corp and Jagran Prakashan are very very similar stocks. (Even Jagran Prakashan’s buyback was at ~4x its book value and promoters participated as well)

Both have sales of around INR 20bn, opm of ~22-23%, gross block of around INR 20bn and a similar Cash profits. Both the companies (after adjusted for working capital, taxes and interest costs) have made a cash profit of INR 1500cr ball park in the past 5 years (2016-2020). Jagran is trading at INR 12bn mkt cap and DB Corp at INR 16bn (33% higher than Jagran).

In fact, Jagran Prakashan has net cash (after removing debt) of almost of INR 300cr, that means you pay INR 900cr for the biz.

Now one would come and say, that hey look, the eps of both the cos are different. DB Corp has an eps of INR 15-16, wheareas Jagran has an eps of INR 9-10 (on a sustainable basis). That’s exactly my point. The main reason is the depreciation. DB Corp is reporting lower depreciation than Jagran, the reasons of which I am unaware of. One needs to look at that. Despite the same gross blocks, why would the depreciation differ? Infact, the 9M depreciation of DB corp is significantly higher than last year. (Apart from depreciation, Jagran has a higher int cost than DB Corp, but that won’t make a big difference, have already considered that).

I believe that at the current juncture, there is an arbitrage between the two stocks. One should look at buying Jagran Prakshan because of the gap in valuations.

Disc.: Holds DB Corp and Jargan Prakashan, both.

1 Like

Here’s my next comment on the valuations and analysis on New York Times and Lee Enterprises

- Lee Enterprises

Warren Buffet bought 28 newspapers in 2010 for $344mn and sold at $140mn to Lee Enterprises in 2020. WB was aware that the newspapers were a dying industry but his rationale that ‘everyone wants to get the info first’ can be read in his 2012 Berkshire Hathaway letter to the investors. In a nutshell, the investment failed.

Lee Ent has a market cap of $80mn, Sales $509mn and a huge Debt of $440mn, zero dividend, negative networth of $38mn. Clearly anyone can figure out that the co. is not at a ‘BUY’ at the current juncture. Most of the newspapers are local newspapers in the portfolio of Lee Ent. (Some newspapers are not even published daily)

- New York Times

NYT is trading at a premium valuation. The co. has a market cap of $8.3bn, Sales $1.8bn (p/s ~7x), ebitda of $260mn, P/b 8x, P/E 53x and a poor div yield of 0.8%.

But here is a justification due to which the stock is trading at such a premium. More than 80% of its income comes from the Digital Services. Biggest Reason! I am not saying that the current valuations are cheap, the stock may even fall, who knows, but there is a reason why it is at premium to its net worth.

Against DB Corp’s annual INR 199 p.a. subscription, NYT charges INR 16/week, i.e. INR 800p.a., 4x DB Corp’s subscription fee.

4 Likes

Hello Chirag,

You’ve done some crisp analysis above.

I have a question regarding jagran. Earlier their app needed subscription but some time back they made the app free and now only revenue source on app is ads. What do you make of this. I thought it was good to atleast keep a very small subscription fee so that Hindi newspaper reader also get accustomed to paying for content.

Thanks

Few suggestions or likely corrections

- DB depreciation is likely to be lower as they did not buy expensive licenses for radio. Though even Jagran was very prudent.

- Both cos did buyback as proxy to dividend as that was more tax-efficient for all stake holders. Generally, if the promoter participates in the buyback, then best viewed as dividend proxy.

- A general observation, that circulation for DB is back to 80% and ads to have reached 85%. Note the economy is only opening up. So the covid impact might not last for very long. I think bears will have to rethink if circulation were to climb back to close to 100% … add these same cos are investing heavily on digital.

Bottomline, too early to say if these cos will be buried, rather I feel they might even thrive. Unlike the USA, the cost of a newspaper is very reasonable in India, as funded by advertisements (which is also information in many cases for the readers, like a new property launch, or a mega sale on ecommerce site). Add the cost of distribution is perhaps reasonable, as we have densely populated markets. Eventually, both Jagran and DB are market leaders in their key markets.

2 Likes

What do you think about high pledging in Jagran? It appears like there is not much information available publicly on why and what.

This was just a pledge to not sell shares as the co took a loan during covid. I think they have not utilised the loan. Hopefully it goes away soon. So will not worry about it. Though sad that the bank was unwilling to lend to the corporate without this guarantee.

Thanks Sarthak

It is definitely not good. We need to see how the advertisement revenues tend to be over a period of time. But in near future, the newspapers will remain a major revenue contributor for both the companies.

Thanks for your feedback

-

Both are running 1 radio channel each, Jagran is 91.1 and DB Corp 94.3.

91.1 was launched in 2001 whereas 94.3 was launched in 2007. Ideally the later one should have a higher depreciation, not the former one. So why the depreciation differs? -

A good option would have been to make an open offer as the buy back price (against ltp on the date of announcement) was higher by only 15-20%. Under Open offer buyback, prom can’t participate and more public s/h could have got an exit.

-

You know better. I can’t comment on the future revenues from the digital subscription. It’s like having an option value which may or may not fructify in future. Please see an article (I think it was in 2018) where the management said they are not thinking to immediately monetize the online platform as the Hindi and Gujarati subscribers may not pay for it. Pls find that if you want to read.

See, you are missing the forest for the woods. My logic is very clear and upfront. You can’t buy a stock just for the dividend yield. I mean, if you want to do that, go and buy Oil India or SJVN or PSUs offering No growth, Full safety of money and 9-10% div yield.

It is a Non disposable undertaking, not a pledge. This question is already covered in some other thread. It simply means promoters can’t sell the stock till the co.'s loans are repaid. What should one look here is whether the loan is taken by the company or the promoters. If the loan is taken by the company and the promoter’s shares are encumbered, there is no worry. You worry only if you believe the co. will not pay loan. If the shares were encumbered for personal loans of promoters, they you had to worry.

Earlier also NDUs used to happen but only pledge was mandated to be reported, not NDUs. Now the SEBI has mandated that even NDUs/Encumbrance needs to be reported in the pledge column.

Thanks

2 Likes