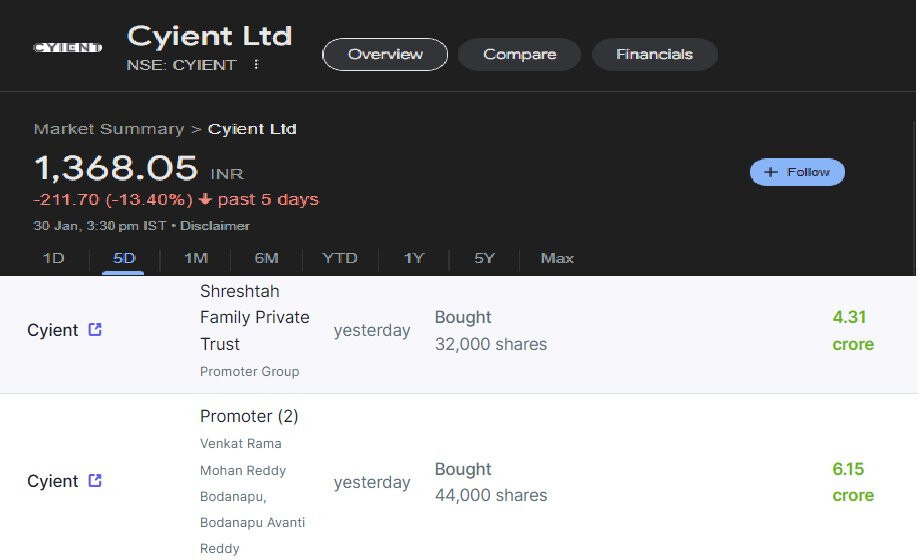

Very poor results by Cyient. Management guided for high single digit growth and delivered 5 pc degrowth. Have been missing guidance regularly.

Invested and looking to exit.

Few of my takeaways from Q1 FY25 of Cyient Limited

𝐂𝐨𝐫𝐩𝐨𝐫𝐚𝐭𝐞 𝐓𝐫𝐚𝐣𝐞𝐜𝐭𝐨𝐫𝐲:

Cyient faced significant operational challenges in Q1 FY25, resulting in weaker-than-expected performance.

However, the company is confident of a robust recovery starting Q2, driven by a strong order book, double-digit growth in order backlog, and healthy engagement with top customers.

The management expects H2 FY25 to be stronger than H1, with flattish year-on-year revenue growth for the full year.

𝐒𝐭𝐫𝐚𝐭𝐞𝐠𝐢𝐜 𝐁𝐥𝐮𝐞𝐩𝐫𝐢𝐧𝐭:

Cyient has announced the setup of a wholly-owned subsidiary to drive dedicated focus on turnkey ASIC design and chip sales through a fabless model for analog mixed-signal chips.

This move is aimed at capitalizing on the growing semiconductor market opportunities, leveraging Cyient’s existing capabilities in design, fabrication, and testing.

The new semiconductor business unit is expected to unlock value for shareholders, akin to the success of Cyient DLM.

𝐌𝐚𝐫𝐤𝐞𝐭 𝐃𝐲𝐧𝐚𝐦𝐢𝐜𝐬:

The global semiconductor market is poised for significant growth, expected to reach $1 trillion by 2030, with the Indian market forecast to reach $100 billion by 2030.

Cyient is well-positioned to capitalize on these opportunities, given its extensive portfolio of intellectual properties, long-standing client relationships, and global capabilities.

The company is also making progress in emerging technologies like Generative AI, winning multiple projects across various business segments.

Industry Tailwinds:

The semiconductor industry is experiencing strong demand, driven by the increasing adoption of analog mixed-signal chips across various industries, including automotive, healthcare, and industrial automation.

Cyient’s expertise in designing and fabricating these specialized chips aligns well with the industry’s growth trajectory.

Industry Headwinds:

Delays and project shifting in Q1 FY25, particularly in the connectivity and sustainability segments, impacted the company’s performance.

The continuing stress in the rail sector also contributed to the weaker-than-expected results.

𝐈𝐧𝐯𝐞𝐬𝐭𝐨𝐫/𝐀𝐧𝐚𝐥𝐲𝐬𝐭 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬:

Analysts were surprised by the magnitude of the miss in Q1 FY25, questioning the company’s forecasting accuracy and process.

The management acknowledged the challenges and indicated that they are working to refine the forecasting process, incorporating lessons learned from the recent experiences.

The company is also focusing on improving the predictability of the project-based business, especially in connectivity and sustainability, to better manage potential delays and ramp-ups.

Competitive Landscape:

Cyient’s established capabilities in design, fabrication, and testing of analog mixed-signal chips, along with its growing semiconductor business, position the company as a unique player in the evolving Indian semiconductor landscape.

𝐅𝐮𝐭𝐮𝐫𝐞 𝐏𝐫𝐨𝐣𝐞𝐜𝐭𝐢𝐨𝐧𝐬:

For FY25, the company has provided a flattish year-on-year revenue growth guidance, citing a prudent approach after the Q1 miss.

However, the management remains confident in achieving a strong recovery in Q2 and H2, driven by a robust order book and growing engagement with top customers.

The company aims to reach its previous year’s EBIT margin range of 16% by the end of FY25, as the revenue growth trajectory strengthens.

𝐂𝐚𝐩𝐢𝐭𝐚𝐥 𝐃𝐞𝐩𝐥𝐨𝐲𝐦𝐞𝐧𝐭:

Cyient has been proactively managing its debt position, which has seen a 44% year-on-year reduction in Q1 FY25.

The company is focused on maintaining a healthy balance sheet to support its growth initiatives, including the new semiconductor business.

Opportunities & Risks:

The growing semiconductor market and Cyient’s unique end-to-end capabilities present significant opportunities for the company to drive long-term growth and value creation.

Execution risks related to the new semiconductor business, as well as potential delays in project ramp-ups, remain key concerns that the management needs to address.

𝐑𝐞𝐠𝐮𝐥𝐚𝐭𝐨𝐫𝐲 𝐂𝐥𝐢𝐦𝐚𝐭𝐞:

The Indian government’s various initiatives to promote the domestic semiconductor industry, such as the Production-Linked Incentive (PLI) scheme, provide a supportive regulatory environment for Cyient’s semiconductor aspirations.

𝐂𝐨𝐧𝐬𝐮𝐦𝐞𝐫 𝐏𝐮𝐥𝐬𝐞:

Cyient’s top 10 customers have seen double-digit year-on-year growth, indicating their continued confidence in the company’s capabilities.

The management is focused on improving the predictability of project-based businesses to better align with customer needs.

The immediate resignation of the CEO can be due to the severe underperformance of the Cyient group including lower guidance for 2025 and underperformance at Cyient DLM(subsidiary).