Veru has always talked about competition in their filings. Let me put it here easier reading for all of us. I am picking out the points which directly apply to Cupid.

Source: https://www.streetinsider.com/SEC+Filings/Form+10-K+VERU+INC.+For%3A+Sep+30/16238460.html#Item1A

It is possible that other female condoms may complete the WHO prequalification process. The female condom marketed by Hindustan Latex Limited, which is the Company’s former exclusive distributor in India, is substantially similar in design to FC2, except it is made of latex. FC2 has also been competing with other female condoms in markets that do not require either FDA market approval or WHO prequalification. Reflecting increased competition, Cupid received part of the last two South African tenders. Increasing competition in FC2’s markets has, and will likely continue to, put pressure on pricing for FC2 and may also adversely affect sales of FC2.

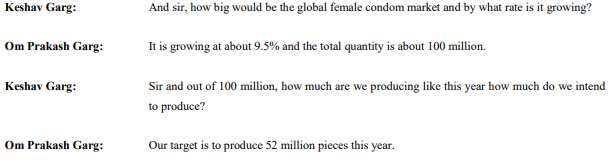

Veru also agrees with what Mr. Garg conveyed in the concall. There are 3 major competitors in this market: Veru, Cupid and Hindustan Latex Limited. PATH used to be a player too, but they lost their pre-qualification in 2019.

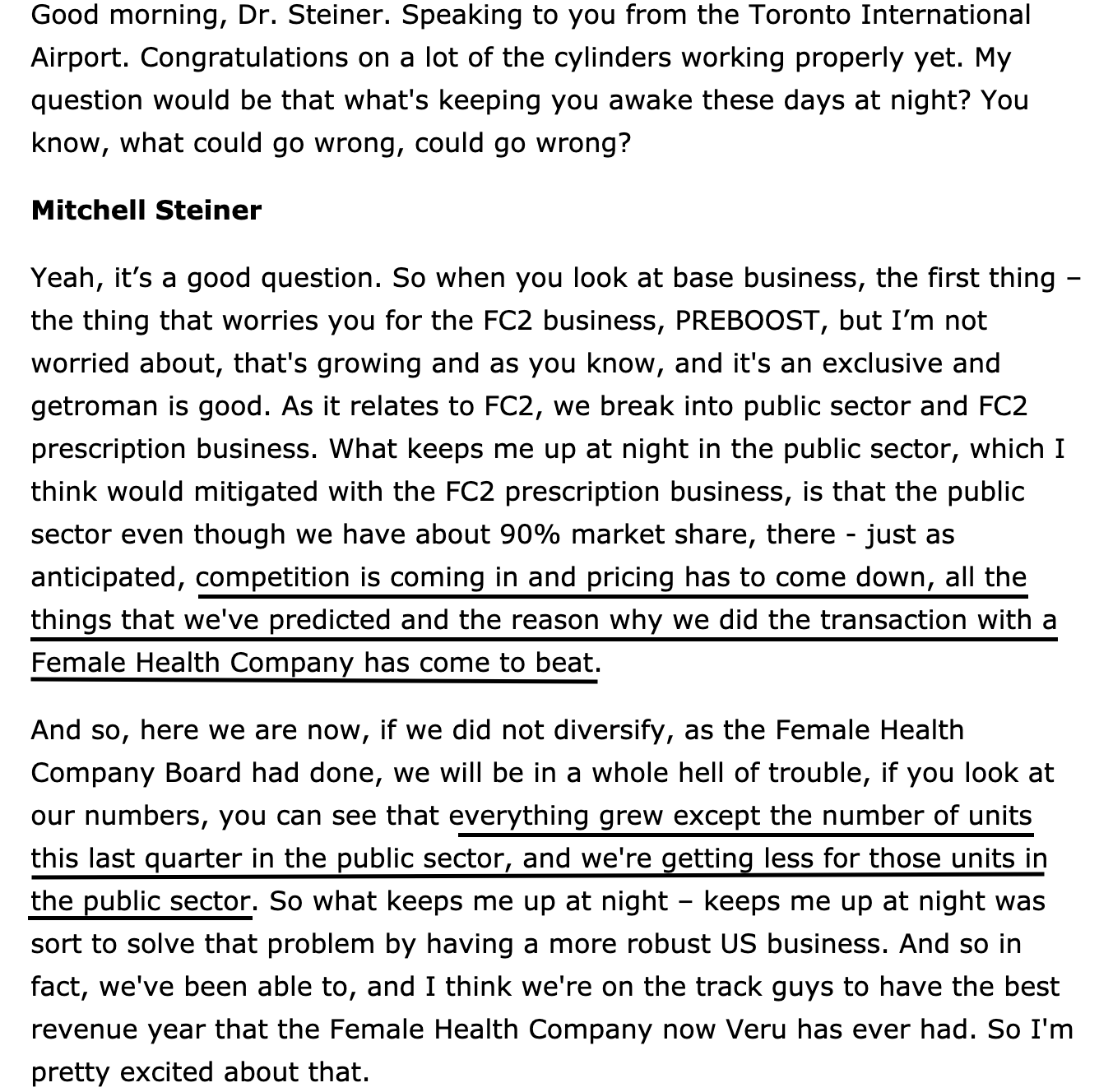

The FDA issued a final order reclassifying female condoms as Class II medical devices, which may result in increased competition for FC2 in the U.S. market.

On September 21, 2018, the FDA issued a final order reclassifying female condoms from Class III to Class II medical devices, renaming them “single-use internal condoms” and requiring new devices in this category to submit a 510(k) premarket notification and comply with various “special controls.” Special controls are a battery of product clinical testing which includes, but is not limited to, determining product effectiveness against pregnancy and against infection transmission, and product tolerability. While FC2 is the only currently available female condom approved for marketing by the FDA in the U.S., this reclassification by the FDA may reduce the barriers for other types of female condoms to enter the U.S. market. If other female condoms enter the U.S. market, we may face increased competition in the U.S., which may put downward pressure on pricing for FC2 and adversely affect sales of FC2 in the U.S.

We may experience intense competition.

Other parties have developed and marketed female condoms, although only two such products presently have WHO pre-clearance and none of these female condoms have been approved for market by the FDA. FDA market approval is required to sell female condoms in the U.S., and WHO pre-clearance is required to sell female condoms to U.N. agencies. The FDA’s recent reclassification of female condoms from Class III to Class II medical devices may reduce the barriers for other types of female condoms to enter the U.S. market. FC2 has also been competing with other female condoms in markets that do not require either FDA market approval or WHO prequalification. We have experienced increasing competition in the global public health sector, and competitors received part of the last three South African tenders and the latest Brazilian tender. Increasing competition in FC2’s markets has put pressure on pricing for FC2 and adversely affected sales of FC2, and some customers, particularly in the global public health sector, may prioritize price over other features where FC2 may have an advantage. It is also possible that other companies will develop a female condom, and such companies could have greater financial resources and customer contacts than us. In addition, other contraceptive methods may compete with FC2 for funding and attention in the global public health sector.

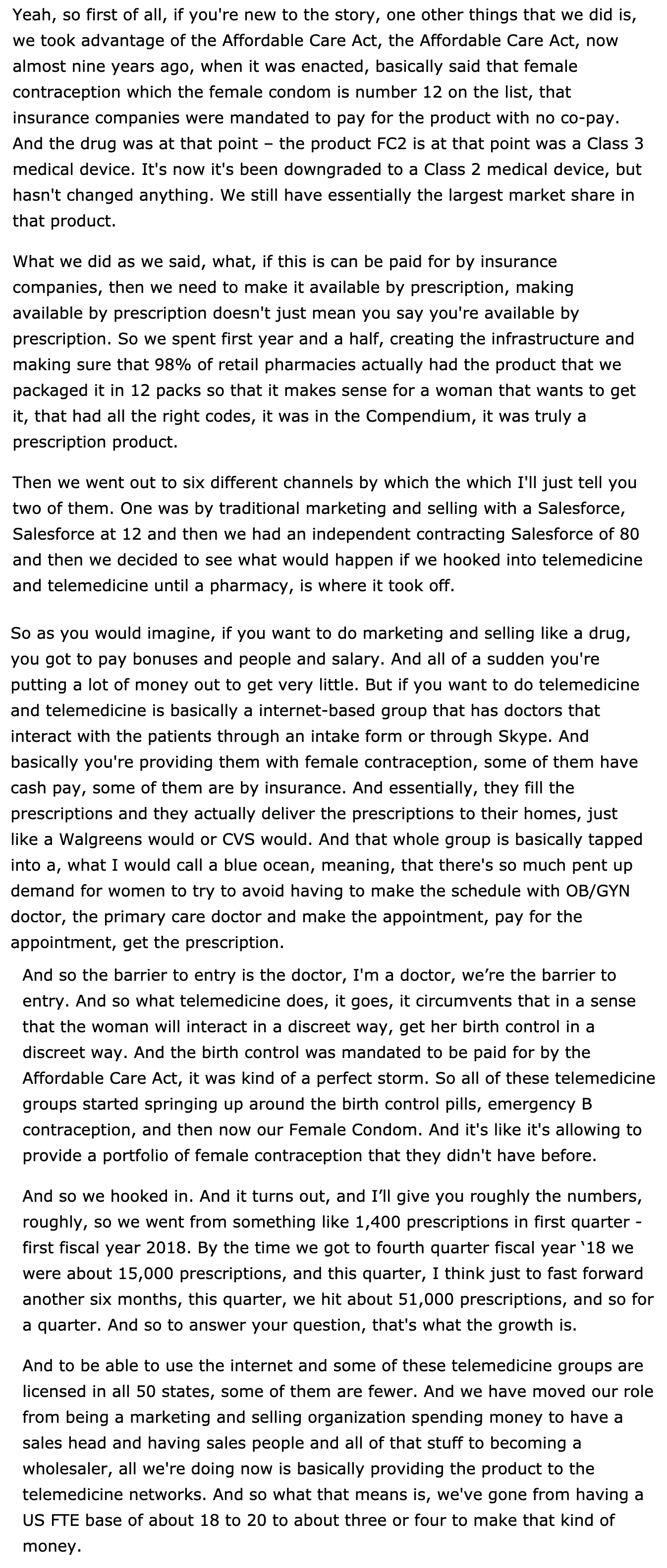

We may not be able to sustain price levels for sales of FC2 in the U.S. market.

Price levels for sales of FC2 in a developed country such as the U.S. are typically higher than for sales to less developed countries in the global public health sector. Over time, due to increased competition or other factors, we may experience price erosion in the U.S. market. Negative pressure on our price levels for U.S. sales may have a material adverse effect on our net revenues and gross margin in the U.S. market.

Finally, as rightly pointed out by @stal88, Veru’s financial position leaves a lot of be desired: VERU | Veru Inc. Annual Balance Sheet | MarketWatch

- Negative Retained Earnings

- Negative or low OCF for the past 3 years

- Negative Earnings (Net Loss) for the past 3 years

- Negative Growth in Assets over the last 3 years, but a Stark increase in Liabilities (This is funded by increased Debt and Working Capital needs)

- 36% D/E (Which is not bad) compared to 0% 3 years back

- Dividends stopped after 2014-15 (Figures)

- MorningStar gives you an overview of Operating Performance over the last 5 years: https://www.morningstar.com/stocks/xnas/veru/performance

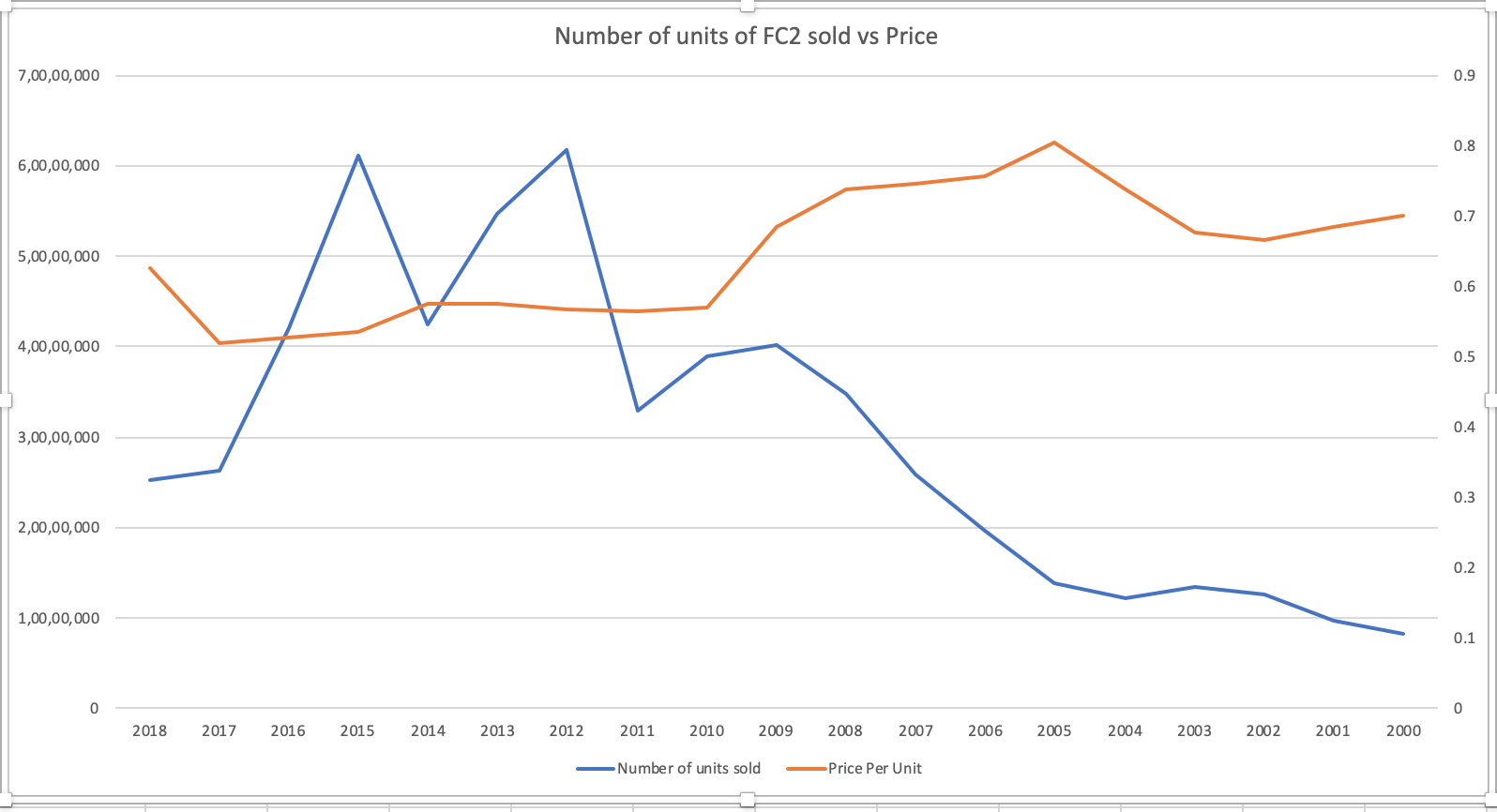

Notice how Veru’s already bad financials took a turn for the worse after 2015-16, which is exactly when Cupid entered the market with their pre-qualification.

There is no doubt in my mind that Cupid is going to take a lion’s share of the US market once they set up shop there (Unless there are regulatory interventions and such).