Results look pathetic to say the least… It was a promising stock once… Thankfully I got out after last quarter results seeing lower sales growth. Monday could be a lower circuit

Hi,

Would suggest to take a look at anothersmall capin the same theme Cosco. Results have been good this quarter.

Regards

This company is long forgotten. Thought there are no specific triggers, at 50cr market capital. 200Cr sales annually, is this worth a relook?

The rising phase of Indian consumer discretionary market with the rising middle and upper middle population is no news. The consumption patterns towards F&B and Clothing have risen drastically and within which the Clothing and Footwear market is poised to cross $100bn by 2025.

Source: Kotak Research and Tata Capital.

Within the crowded clothing and leisure market is Cravatex Ltd. The company is in the sports clothing and sports equipment business with exclusive license for the FILA and Proline brands in the Asian Sub-Continent.The company has the FILA license upto 2043 The company has been struggling over the past two years with slowing demand, trend shifting towards ecommerce discounts and currency depreciation affecting imports. The rising working capital loans also dented the bottom line further. Inspite of the headwinds, consolidated revenues in FY16 and FY17 were 270 crores and 257 crores respectively.

Although, the profitability in the past two-three years, rising debt made the company cripple under pressure, the chain of events since February 2017 are worth noticing and very rarely have I seen a company this small getting into such transformative Balance Sheet restructuring-

-

In December 2016, company incorporated Cravatex Brands Limited (CBL).

-

Till March 16, Company had a single subsidiary BB UK which took care of the its international licensing operations. BB UK clocked a revenue of 110 crores in FY17.

From the Website-

BB UK provides end-to-end design, development and sourcing services for all Fila development within Cravatex and to other Global Licensees. BB UK also operates an exclusive Sub-License given by JD Sports PLC for the Fila brand in the UK and a Sublicense for Accessories for the whole of Europe from the brand owner.

-

In Feb 2017, Company initiated sale of its Fila and Proline business (90% of Standalone Business) on a slump sale basis to its subsidiary CBL for a consideration 32.68 crores. Also, now CBL is its 100% subsidiary. The consideration is paid by issue of equity shares of CBL.

-

In March, CBL receives an investment amount of Rs.75 crores from Paragon Partners. (Not relevant but one of the partners at Paragon is Deepak Parekh’s Son). Since, most VCs and Private Equities invest via convertibles/preference shares, on paper it still appears as Cravatex Ltd. holds 100% of CBL. The investment by Paragon was made in the following manner-

a) 57 crores via CCPS (Compulsorily Convertible Preference Shares)

b) 18 crores via Optionally Convertible Debentures

Based on the slump sale basis, we can assume the pre money value of CBL’s business as 33 crores (although since it is internal transfer of business it is the most conservative possible value).

The company has not completely disclosed the term sheet (which it should being a public company) but taking into consideration general PE terms, the convertibles would crystallise on the happening of a future event like fund raise, revenue target, IPO etc. Paragon currently has voting rights and 2 board seats along-with other general exit and anti dilution rights.

The reason why the investment was not made within the holding company would definitely be to prevent the Open Offer curve. The PE does have a significant indirect ownership in the company though which would not be clear from the equity holding structure. Another interesting fact is one of the portfolio companies for Paragon has got the SEBI nod for a 400 crore IPO, one year after Paragon invested in them. I do not expect an IPO for CBL that soon but never say never :).

-

Post this funding the company seems to have paid off its long term loan liability. The working capital issues would have dissolved allowing the company to focus on expansion, which was derailed over the years because of host of issues. The balance sheet is significantly streamlined. Would be interesting to see the next year as the company has not disclosed any future expansion or business plans in its public filings.

-

Cravatex Ltd. thus is a holding company with two subsidiaries with BB UK forming around 40% of its revenues, a significant jump from the past few years and CBL forming 60% of its revenues which is poised to increased once the funds are utilised. On the standalone basis Cravatex would just have the residuary sports business such as the license for the Wilson Brand etc. which would not be significant.

The company’s long standing ability to manage brands like Proline, FILA as well as the long license agreements with a strong backing professional board is an impactful new beginning and should be watched closely.

Reopening this thread.

It is time to look into this stock. Company is planning to open 100 new stores in 5 years year

Stores are being opened in posh locations and malls with the idea of brand building.

It is taking up a massive influencer campaign on Social Media (specifically Instagram)

Sales have already doubled its sales and swung from loss to profit. Dividend too has been increased.

Would be helpful if people can post about new stores in their cities and their experience with the product.

Attached are some important links/Snippets on what their strategy is

“We were approached by Rohan Batra, CEO of Fila India, to create an online presence for the brand, that would appeal to the youth of the nation. Fila had, as yet, to cement an identity that was relevant to its Indian consumers. We decided to create a lifestyle connect in an unconventional way - associate Fila with movement rather than performance and create a brand synonymous with Dance.” - http://thoughtoverdesign.com/work/fila

https://apparelresources.com/business-news/retail/fila-aims-grow-five-times-india-2023/

2 Likes

700 Crore sales and 70 Crore market Cap.

Debt too is just working capital debt and is quite moderate in relation to the sales being done

1 Like

They have now also partnered with Vans in India

1 Like

They have got a sitting PE as well, who has invested in their subsidiary. One could consider that a positive for management credibility.

PE is invested in Capacite, Chai Point etc.

This is from the opening post.

We have seen value destruction over the years.

What has changed now?

Hi Ashwini,

Do you have details about the breakup of this turnover. I really doubt that they could have scaled up to this number from just Fila brand (even bigger names have much lower turnover).

Also, somewhere i read that the listed co would not continue to own the majority stake in the key subsidiary in coming times…is that right?

1 Like

Details of the deal with Paragon - http://www.cravatex.com/admin/file_new/23-03-17%20-%20Outcome%20of%20Board%20Meeting.pdf

Agreement is not very clear to me: But does it mean they have valued Cravatex Brands at about 75cr? Is it correct, After conversion of debentures and preference shares, Cravatex’s holding in Cravatex Brands will become negligible.

Looks like majority of revenue and all profit is coming from BB UK which is more like outsourcing service for Fila.

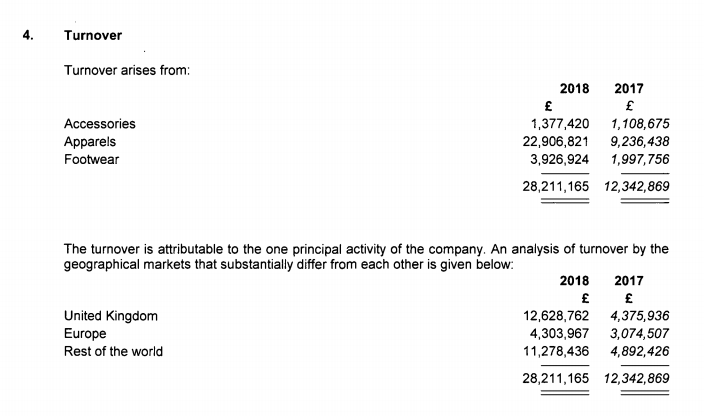

As per last year’s annual report revenue from Cravatex brand was 113 cr and BB UK was 242 cr.

1 Like

This year’s subsidiary report is not out yet I suppose. Last year BB (UK) had £28mn revenue (28*90= INR 252) with breakup as following:

As per Cravatex report, ‘717 out of 722 crores revenue’ and ‘11 crores out of 10.5 crore net profit’ is not audited by the Cravatex auditor. On checking BB (UK) Ltd auditor is SRV Delson, don’t know how reliable is it.

my take is maybe because of international presence INR 700cr is not that much!

2 Likes

![]() But that is only revenue they have

But that is only revenue they have

1 Like

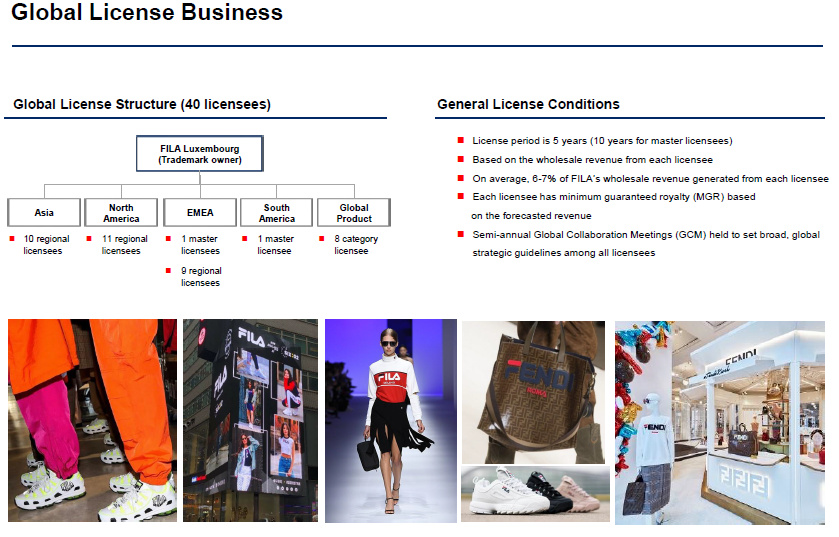

FILA brand is globally owned by FILA Korea which is a listed company, which licenses out the brand in some countries while it operates directly/ through JVs in other regions.

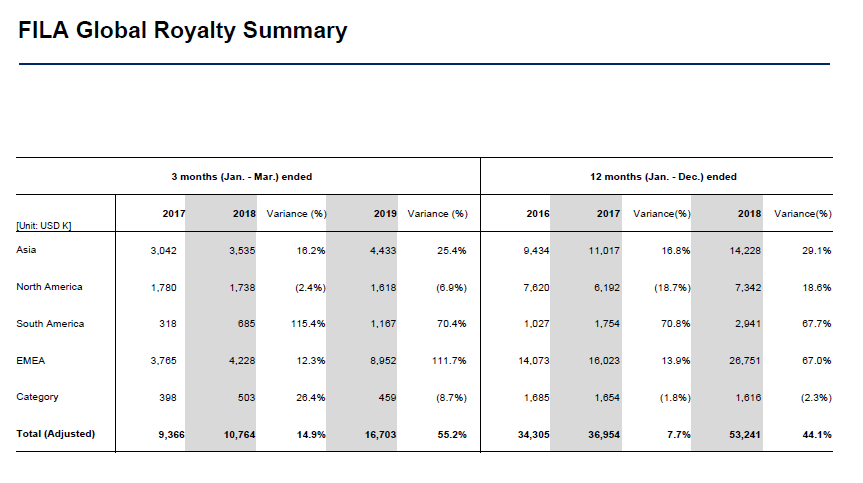

See following screenshots from FILA Korea IR presentation (attached for reference). You would notice that royalty from EMEA has grown by > 100% in Q1-CY19 to ~$9M. Using the average royalty rate of 6-7%, on reverse calculation this would equate to ~$550M annually. Now UK, for which Cravatex has a sub-license for, would only be a small part of the $550M, but even if it is 10-15%, the INR700 Cr does not seem unreasonable.

You can also read this interesting piece from Bloomberg on FILA’s increasing brand popularity: Bloomberg - Are you a robot?

Comments welcome especially from @basumallick sir, who had flagged this company as one to investigate further in his presentation at 2019 VP Chintan Baithak.

2019_1Q_IR_Material.pdf (2.2 MB)

Disc: Not invested

3 Likes

Do keep an eye on Instagaram and try to search #FilaIndia there… A lot of information regarding new stores brand activities will come up

Which cravatex report are you referring to. 2019 ar isnt out.

Had written about the deal two years back-

https://www.linkedin.com/pulse/rising-indian-micro-caps-cravatex-ltd-bhavik-mehta/

My sense is the terms of the Share Purchase are not in public, but the promoters would not dilute off majority as their way to get something out of this is through cravatex as they do not hold much of cbl directly. Even if its a 50:50 stake between Cravatex and CBL theres much value. Apart from that BB UK has been doing really well.

Dear all,

Most of this company’s revenue generates from Subsidiaries and company provides consolidated results annually only…then how can we track its performance?

Thanking you

Prashant.

1 Like