I believe this is not necessarily true. Check operating margins in Mar 12, 13 and 14. I would still maintain that it’s a cyclical stock. Though by focusing into value-added films, they are trying to reduce the cyclicality.

-Jiten Parmar

I believe this is not necessarily true. Check operating margins in Mar 12, 13 and 14. I would still maintain that it’s a cyclical stock. Though by focusing into value-added films, they are trying to reduce the cyclicality.

-Jiten Parmar

This seems ot be an interesting company. However there are few questions that I have an would appreciate it if any of you can help me by answering them-

Thanks

I am also tracking Cosmo for last two months but still have few concerns about it. It will be helpful if someone can clarify.

a. Packaging industry is debt intensive. You can look at any of its competitors in India. As of Sep 2016 result,

Long term debt - 308 cr Short term debt - 137 cr

Total debt ~ 450 cr

Equity and Reserves ~ 500 cr

On top of it, they have cash /bank balance ~ 32 cr

So debt/equity is pretty comfortable < 1

Another positive thing - they have not diluted equity since 2005. Debt since 2011 is more or less around 400-500 cr. They have improved their topline slightly and bottomline quite considerably during this period without equity dilution and keeping debt more or less constant is no mean feat.

b. You are right regarding specialty film segment as that is high margin segment. But operating at 68% means there is still considerable room (32%) before they would need expansion.

c. Regarding using ROCE, you are absolutely correct. Another better metric here would be ROIC/ROIIC, which takes into account incremental capital invested.

In any case, ROCE = EBIT /Capital employed = 154 /878 ~17.5% (improved from 5% in 2014). (figures from March 2016)

d. Regarding Mr. Jaipuria and LGT bank connection, there has been no update since the news broke out in Mid 2014. I would like to point out more about how mgmt is been honest in operating the company by not diluting or introducing warrants, paying high dividend, etc.

Point no 4 is learning for me. Did not use key words like money laundering though i remember using word fraud, legal etc. Anyway, mistake done and accepted,

Disc : Hold but back to validation of assumptions mode

Cosmo Films new plant started. Will add 40% to capacity.

Management very positive about future http://www.printweek.in/news/forecast-2017-satish-23837

Couple of Points to Note

TO has been flat for last 3 years . BOPP and laminations have overcapacity globally and hence suppliers like cosmos have very little bargaining power

OPM has expanded from 5% to 10% on account of Crude which will start to reverse ( visible in Dec qtr )

Only good thing is it is getting some tax benefits & there is some low cost capacity lined up .

Another issue is Make in US can be bit challenge as it has limited capacity there as compared to Jindal poly films or other US based suppliers

The only way to play this stock is buy when stock is trading less than 0.5 book value ( < Rs 120 ) and sell when it above ( 1.2 to 1.5 BV ) .

Discl : I used to hold the stock . Bought at 56 - 70 in 2011 - 2014 and sold between 275 to 370 in last year rally . Maybe biased

Shailesh bhai… Thanks for your views…Some rebuts -

From the annual report -

Financial Year 2016 has been one of the best years in the history of Cosmo Films. Consolidated sales stood at Rs. 1,616 Cr representing an 8% growth in sales (not revenues). Furthermore, EBITDA rose approximately 80% to Rs. 197 Cr. During the year, we not only remained focused on driving cost efficiencies across our global operations but also implemented a number of marketing initiatives to increase the sales of higher margin products in specialty films. As a result of these relentless efforts, consolidated profit after tax expanded more than three times to Rs. 96 Cr. Our U.S. operations have also improved from last year as a result of several strategic initiatives taken. Strategic focus area for the company remains value added specialty films and we look forward to increase its share in future.

Even though sales volumes (particularly overall specialty sales) grew, revenues declined as benefits from lower raw material prices were passed on to consumers. EBITDA on a consolidated basis is Rs. 196.84 Cr as against Rs. 110.31 Cr in F.Y. 2015, an increase of 78.4%. This includes benefits from a reduction in variable costs through several engineering initiatives. In particular, power cost and freight costs were optimised.

In any case, topline will be taken care of this year and the next with new capacity coming online in Feb 17.

As mentioned in point 1, this is not just because of crude (there might be some impact definitely), but due to increased focus on specialty segment, various cost improvement measures (power savings, marketing and engineering initiatives, reducing inefficiencies, removing bottlenecks, improving US operations). Moreover, mgmt has time and again said that they are increasing focus on specialty segment. This will be the next margin trigger. Along with, the new BOPP line is highly efficient, and would entail savings resulting in better margins. Another important thing is continuous improvement in their US Operations. Here is what mgmt said in August 2016 -

"We had an issue with our Asian subsidiary of Japan and Korea where the currency really went against us, where it was 80 yen to the dollar and it went up as high as 120 yen to the dollar and now it is back to 100 yen to the dollar which gives us a more productive base at least on the Asian side. So I certainly think that this quarter onwards if the currency movement is not as volatile, or we should do better in our Asian subsidiaries.

Where the US is concerned, there have been one-off write-offs, there has been one-off some receipts which we got on the customs duty, but I can assure you that the US operation is much more under control. We have revamped the organisation, we have got the right processes in place and I must tell you this today that we are looking to expand US operations at least doubling the revenue in the next couple of years. We are going to invest there, we are going to spend more on processes, but I am fairly confident that in the next 24 months, you will see at least doubling of our revenues which will obviously mean a productive bottomline".

Refer to point 1 and 2 ![]()

Disclaimer: Invested. Very bullish; views might be biased!

Good to know you are invested .

Pl check history on earning on screener . It has volatile OPM which moves between 5% to 12% .

In any commodity stock I check status of 3 leverages : Operating Leverage ( capacity utilisation, movement of industry capacity ) , Margin leverage ( RM cycle , Overheads etc ) , Financial leverage . Right planning can 5 bagger to 10 bagger returns .

In Cosmo btw 2011- 2014 I had all three leverages in my favour . Now they are not there , so I moved out of stock .

Operational leverage would improve further with new capacity coming (which is the most efficient production line in the world). Financial leverage is actually improving over time and would keep on improving with increased margins going forward due to focus on specialty segment. They have actually repaid some debt this year despite capex. RM cycle - They want to remove the cyclicality aspect, so moving toward this specialty segment (they mention this in their presentation).

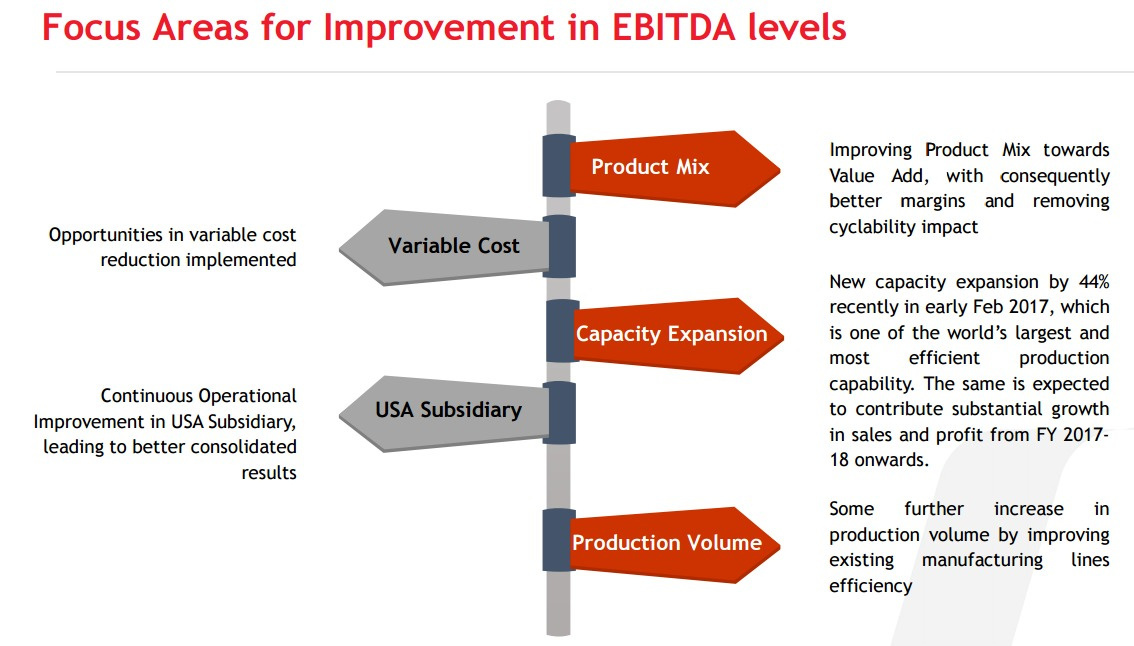

Some points pondering over from recent presentation -

New capacity addition in FY 12-13 impacted margins temporarily in India, which is now totally reversed

Consolidation results in FY 13-14 and 14-15 were adversely impacted by USA subsidiary, which is on

operational improvement phase

During Q3 FY 16-17, the company was under installation of its new line (largest in India with a capacity of 60,000 TPA). Given that new line is installed at the existing site, shut-downs had to be taken on existing lines which caused a volume drop. The demonetisation too has impacted the company adversely both on volumes and margins. The said two factors have caused a volume drop of 6%. The new line (with capacity enhancement of 40%) has already now been commissioned in early Feb 2017 ahead of schedule at lower than planned cost.

On Financial leverage, debt/equity and interest cover are actually getting better over time.

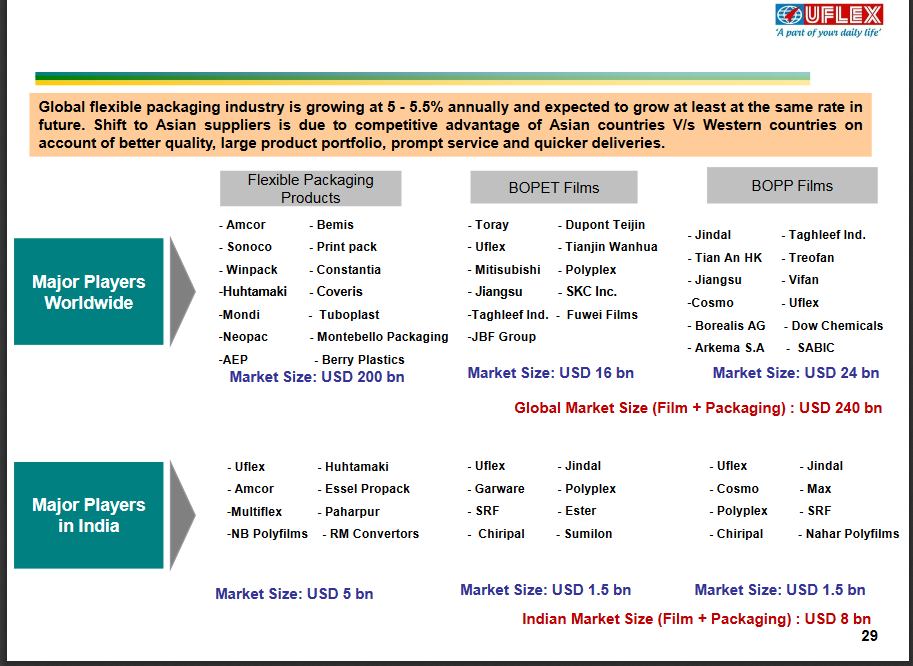

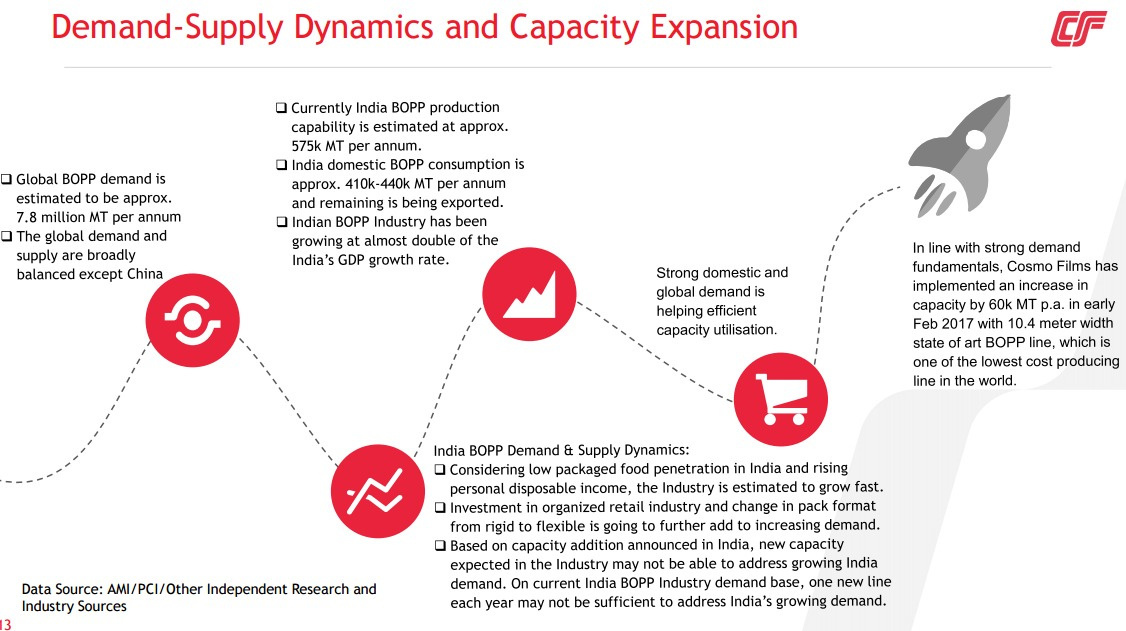

Some good graphics from presentation -

I will be glad to be proven wrong. But I thought I had a 5 bagger in 3 odd years so I sold out .

Some facts from competitor AR which might of use to you

In the year 2015-16 prices of BOPP films remained firm despite falling raw material prices. We expect the lower raw material cost to be fully passed to the end customer in year 2016-17.

The global BOPP industry is dominated by China which accounts for nearly 40% of the global capacity and consumption. The capacity utilization in China has been around 70% for the last few years. The Chinese market itself is growing at an average rate of around 8% p.a.

Mr. S. Satish, Global Head- Sales & Marketing, Cosmo Films said, “The universal printable synthetic paper has been a long standing unmet need of the market, as currently different synthetic paper grades were being offered for different printing technologies. This universal printable product would help the printers to significantly reduce their inventory carrying costs.” Read more http://whattheythink.com/news/84640-cosmo-films-launches-universal-printable-coated-synthetic-paper/

Cosmo planning to enter BOPET. Any idea how this will impact it’s performance? http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/7b9e9f18-2d52-4842-8f0e-ac27a1483de7.pdf

Management’s interview on the revenue expected from the new plant and debt going forward

Hi Chirag

@chiragjain1976

This is One of The best Packaging Company compare to its peers. Value Investing !!!. PE below 9 & Book Value 1.45. D/Eq 0.93. Current ROE is 23%. Promo stake is somewhere 47%. I have planned to invest in this but waiting for market to correct as nifty is @ ~24PE.

More Chocolates & more more Corn flakes & other daily needs products to come in packaging format. Keep track of Quarterly Balance Sheet from here onwards. Keep it simple.

Can someone tell me how BOPP / BOPET players will not end up facing reduced returns going forward? Each player that at least I read about, is making heavy capex plans - I wonder why it won’t impact margins long term

Key players I am monitoring - Cosmo, Jindal, Uflex, Essel, Polyplex

Each one says they are increasing share of specialty films, but I somehow think its increasingly difficult to do so with increasing capex

Would appreciate any insight especially with respect to Cosmo

Hey Sachit,

Thanks for starting this thread, I have heard a lot about Polyplex and Jindal Polyfilms. I am also planning to add one of those to my portfolio. Really need some insights on the best one among them