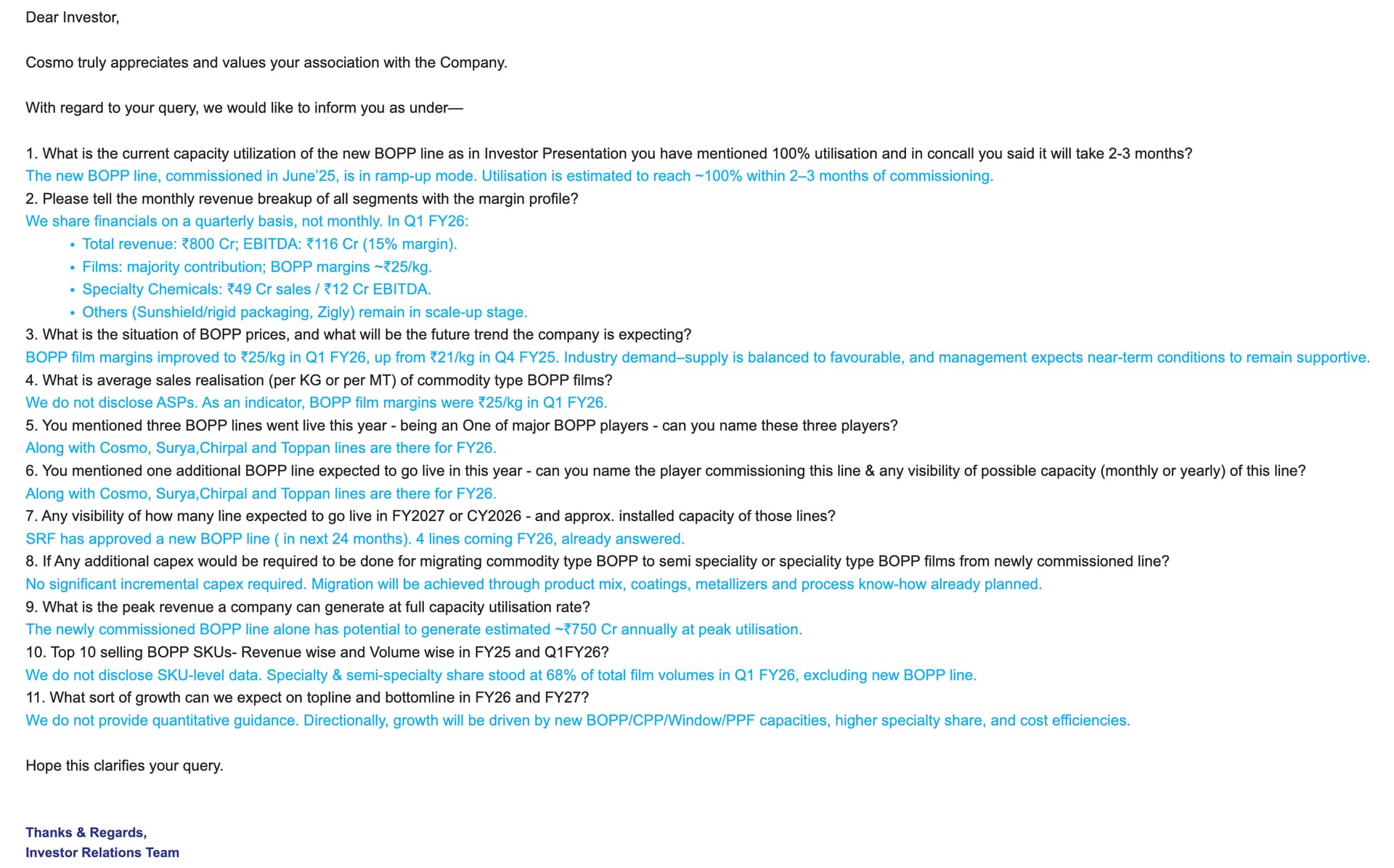

Full leverage of supply side issue is being monetized by Cosmo. No doubt if situations remains like this Q2 is expected to be much better (better margin, full capacity utilisation of new BOPP line).

Would you like to disclose the source of this data, please.

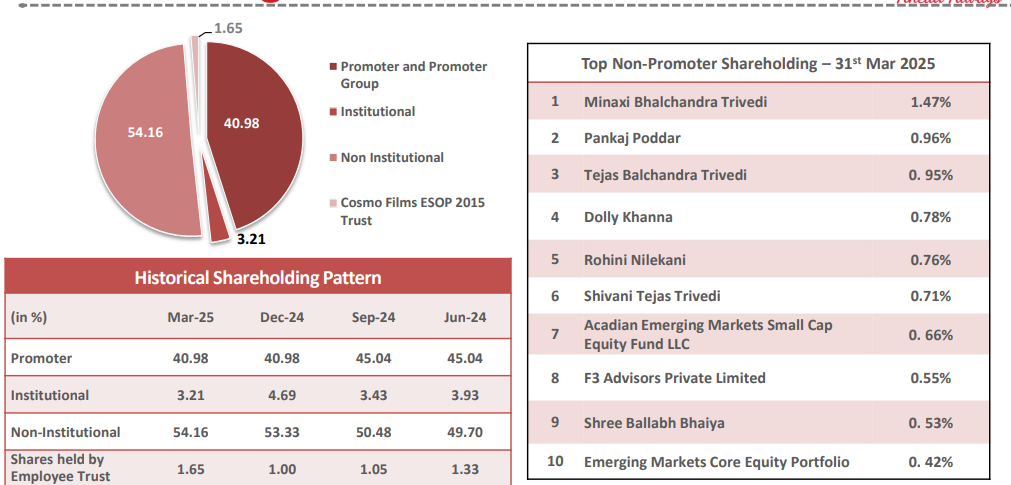

Dolly Khanna & Rohini Nilekani reduced stake, also seems some clerical error by whosoever prepared this SHP .. look at #7 & #9 (same shareholder mentioned twice).

Also look the numbering post #7… is it just an unintentional error or something else behind the scene.

BOPP margins running near to Rs 25 per kg during Q1FY26 vs Rs 21 in Q4FY25 and Rs 19 in Q1FY25. For june it is Rs 30 per kg.

Company started new line which is of 81000 Tonnes started operations from 1 June and this line added 45% to earlier capacity. Incremental Fixed cost for new line is very minimal.

New line adds 750 Cr of revenue to the business at full utilisation. By next 3 year this line will be used only for Speciality films.

Current speciality films mix of total BOPP is 68-70% as per volumes and 80%+ in terms of amount.

The new film lines are one of the most cost efficient and should make Cosmo more competitive in the market.

Window film line which started operations in May 2025 under brand Cosmo Sunshield gained momentum with more than 50 distributors. Both the business segments will be EBITDA positive by next Quarter.

Investment done in last 3 years started commercial production in Q1. In window films – company has first target of domestic market, and company already started making brand in Domestic market.

Jindal had 15000 tones Capacity per month which get impacted. In current year there are 3 new line came which covers 11500 Capacity since there is shortage gap of only 3000-4000 tones. (As per my analysis, one line averagely is of 30000 Tones per year capacity which means 2500 Tonnes per month and Cosmo introduced 81000 Tones line which is world biggest line with monthly capacity of 6700 Tones. This means 2 lines of 2500 each and 6700 line of cosmo adds to 11500-12000 Tones monthly capacity. Hence, here also beneficiary is Cosmo)

India has 65000-70000 Tons domestic consumption and 15000 Tones is exports, Cosmo is the largest exporter.

Current Tariff Rates are unsustainable, management feels it will reduced to 15-20% soon. Company business will impacted at 20-25% of tariff.

Last year company did 250 Cr of sales to US last year which is 8-9% of sales. Management said company currently not looking to increase it further. So at per current run rate of 4000 Cr, this year it will be around 5-6% from US. If the Tariff rates will be 50-55%, then company may loss its 50% of business in US.

After fire incidence, lots of dealers imported good quantity because they thought companies will rise prices to very higher level and margins will be increased significantly. But companies increases prices to certain level and at this price imports become useless as dealers also has to pay import duties and dealers has to sell their inventories at losses.

Imports as of now reduced and by August end imports will be stopped. Imports are mostly coming from China.

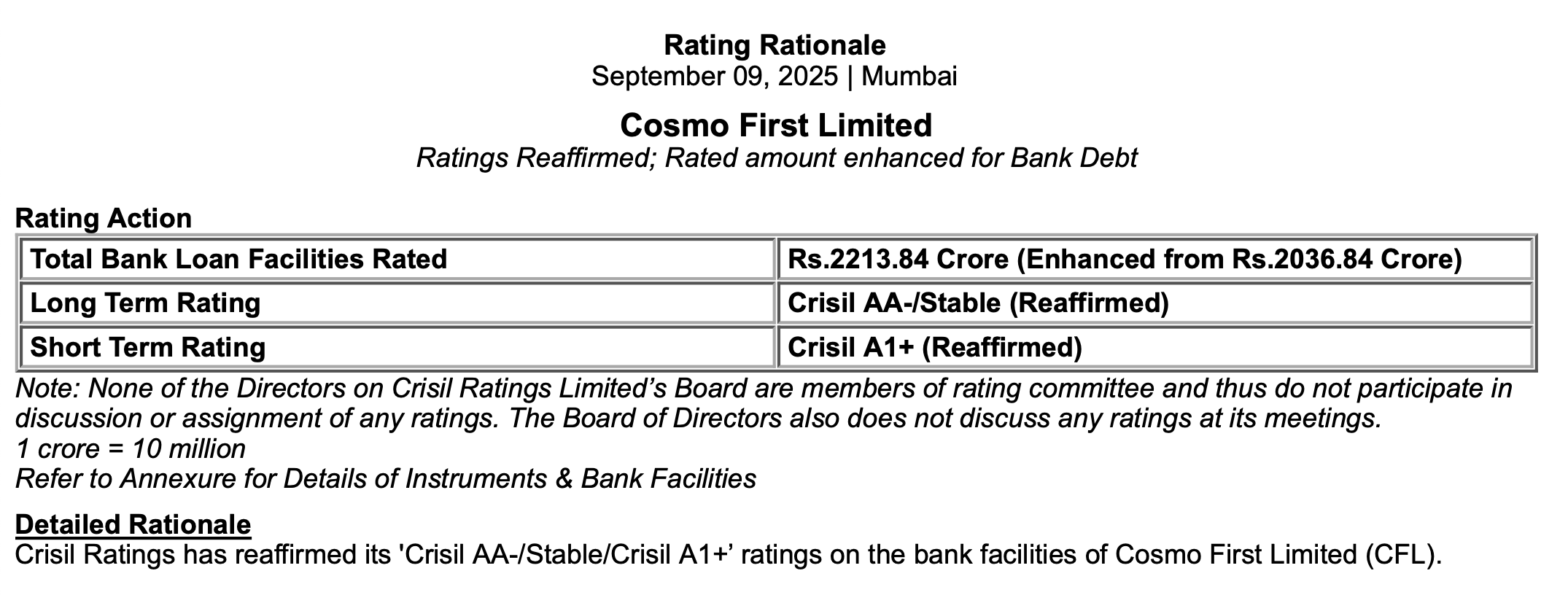

Company’s current net debt stands at 1140, this is peak level as reasonable capex has been done and no further capex plan for next year by the company.

ZIGLY – In Q1 revenue was on lower side because of some issues in Online business because of change online selling platform but companies retail business grew by 30-35%. Mangement also mentioned about recent acquisition will add 25-30% in Zigli revenue.

Company currently have 33 Pet Care Centers and will take it to 40 by next quarter. By december, most of the 2 years old center will start making money.

Export contributes 40-45% of total revenue.

Any change in raw material prices will be passed on to the customer.

Management said there will be favourable demand for next 1.5-2 Years.

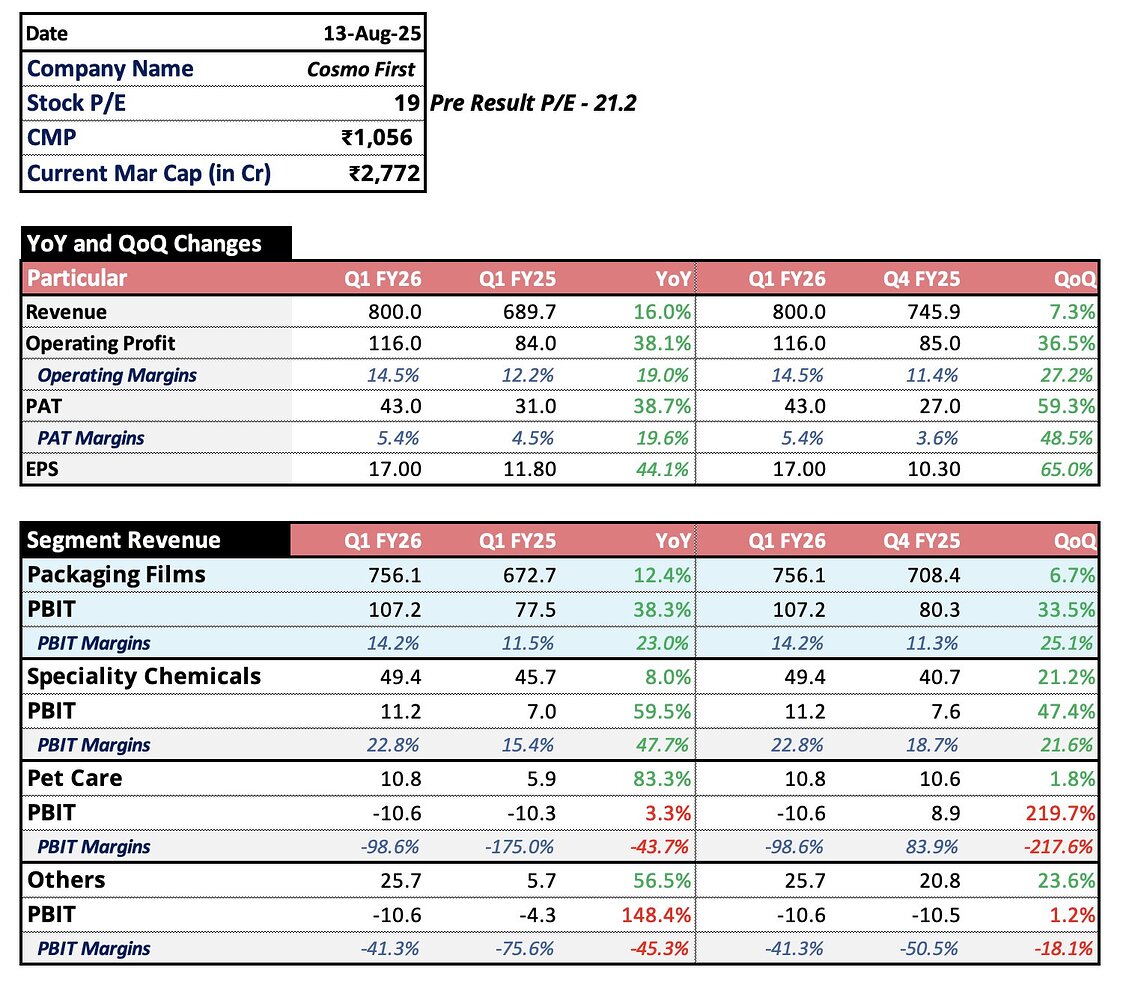

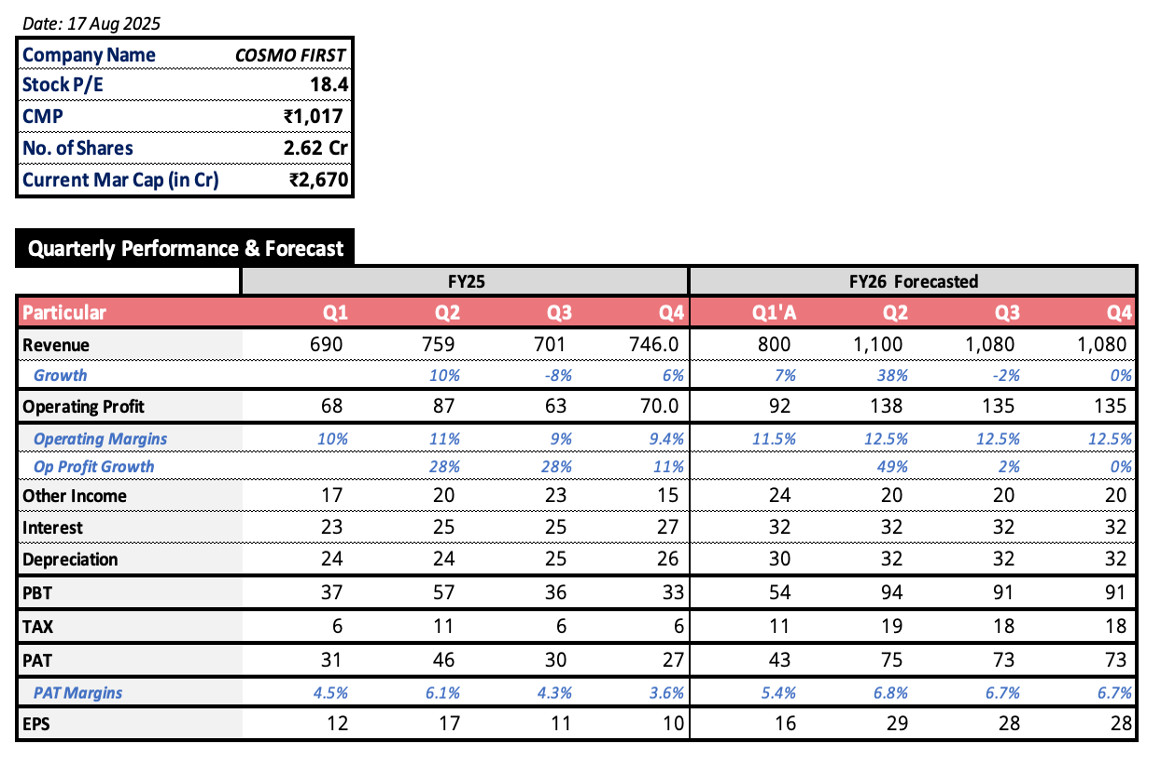

In Q1, there is no major improvement in revenue despite huge increases in prices of BOPP in June, whole because of there is significant price drop in first 2 month of Q1 i.e. April and May, the June month take all up and put it in positive trajectory.

Q4 FY25 base is huge that makes the result neutral.

We can see prices were drop in April and then in May significantly. So as per this we should consider Q4 prices as base. As per this 13-15% net prices increase of BOPP films.

Our capacity increased by 45% which means for first 2 months we have 196000 Capacity and now have 277000 capacity.

As per the above analysis and weighted calculations:

First 3 month revenue will be as follows:

April : Rs 220 Cr

May : Rs 200 Cr

June : Rs 380 Cr This gives us conservative run rate of Rs 360-370 Cr per Month.

Taking above analysis into consideration 360*9 = 3240 Cr + 800 Cr in Q1 we will get a total revenue of 4040 in full FY.

Management also guided the same levels.

On margin levels it will further improves in coming quarter. As other business will become breakeven and For BOPP segment Company has average realisation of 30 Rs/kg as which is higher then whole quarter i.e 25 Rs/kg as per this scenario our EBITDA levels will be somewhere around 12.5% or more for coming quarters.

Debt is at peak so not further increase in Interest levels.

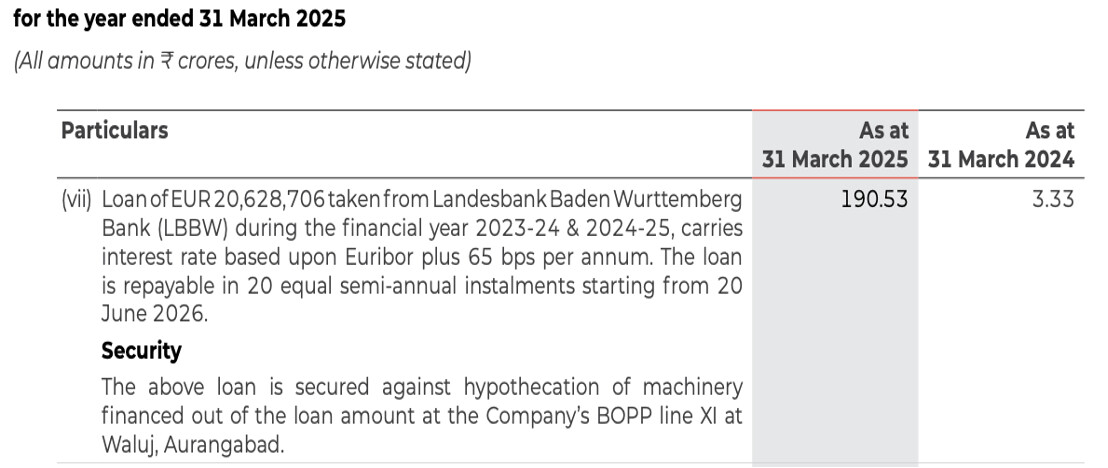

For new machine company has also taken loan last year at very minimal rate i.e. Euribor + .65% which will be maximum upto 2.6% - 3% per annum, interest payment will starts in jun next year.

Wondering what would be the average sale price per KG of commodity type BOPP films by Cosmo. Just for ex. @ Rs.100/kg - Per Ton sales value comes Rs. 1,00,000/- and hence for 81000 ton capacity (if operated at full capacity) must come at Rs. 800 Cr+.

For Semi Specialty and Specialty type BOPP films - I assume sales price would be higher vs commodity BOPP films (as Margin earned by company is also higher in those films type) - in case yes this calculation on projected revenue must be relooked.

Another thought which caused me to question the management commentary in concall is - if Existing Capacity of 1,96,000 MT in giving a sales of approx. Rs. 3000 Cr then why only Rs. 750 Cr- Rs. 800 Cr turnover from additonal capacity of 81,000 MT.

It must translate into additonal turnover of approx. Rs. 1,000 Cr.

If any VP member from this line of business, can please guide if in reality what would be on average sales value (per Kg) of BOPP films produced by players like Cosmo etc.

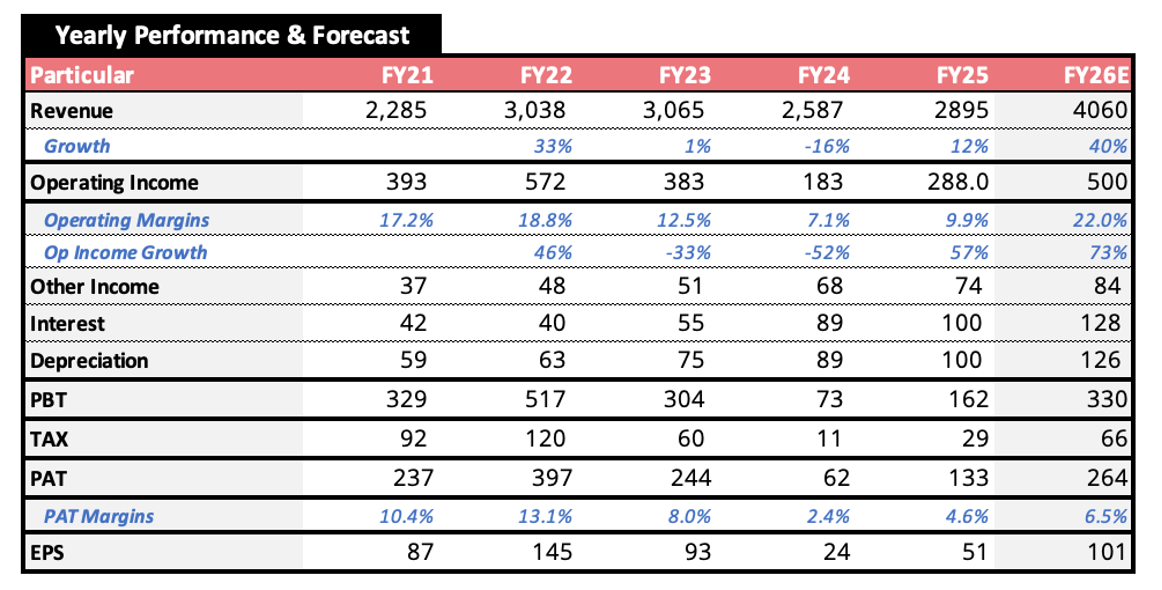

Crisil Ratings expects revenue growth of 30-35% in fiscal 2026, driven by the ramp-up of newly commissioned capacities with EBITDA margins ranging between 13-14%. Very Positive for the company. From 10% to 13-14% means 300-400 Basis point improvement in margins which is very huge. Revenue will also be increased by 30-35% which is significant improvement in Topline.

New capacities got absorbed in the market easily because of Jindal Poly issue.. the rise to the 180 was temporary and was to come down.. what we should understand that there was huge capacity addition and still price are not falling much.. we must focus on what is next.. the new capacity in next three years and demand supply issue in next three.. we will be happy if you can elaborate on this area…

Thank you @jitenp .. these are wonderful insights on BOPP as well as BOPET.

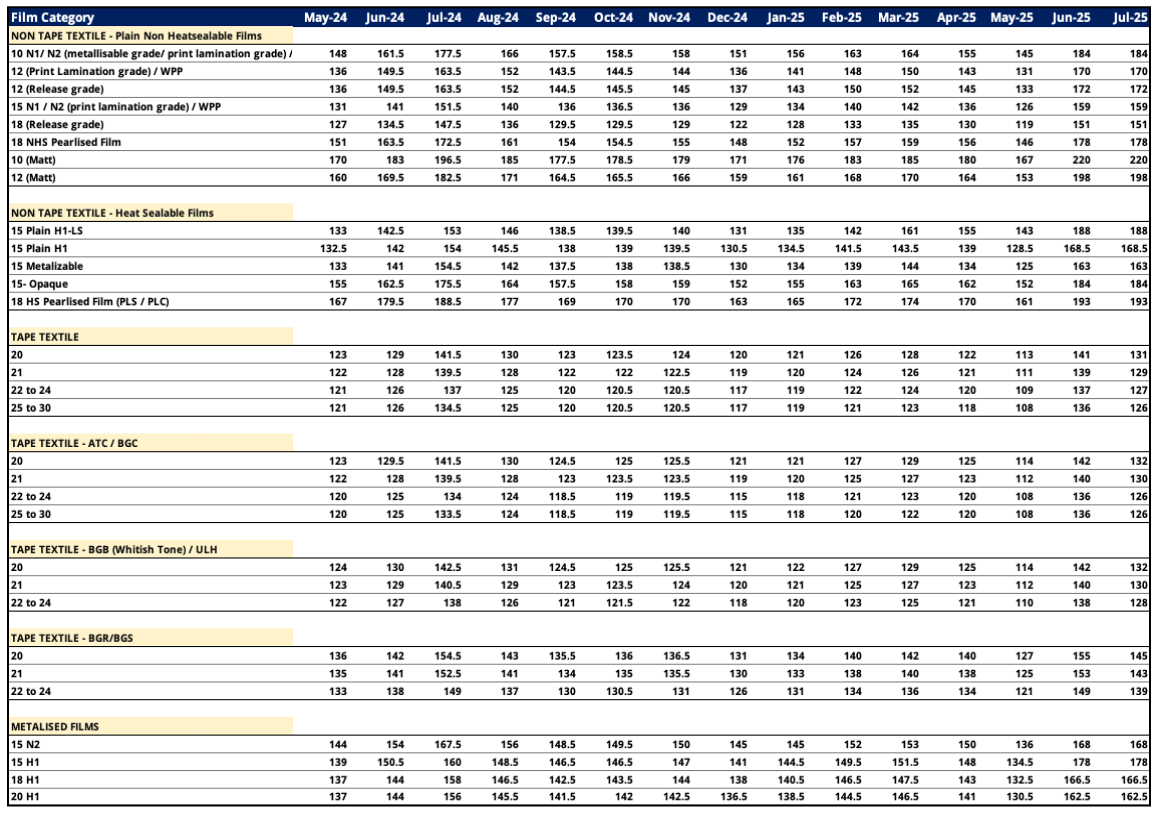

As a fellow investor, if you don’t mind in sharing, - BOPP @ 140, BOPET @ 93 is this Commodity film type rates or blended rate for commodity + Semi speciality + speciality.

Also, in case you have any idea - any platform / website ( other than JPFL Films: Price List) which an individual investor can refer to get an understanding of prevailing BOPP /BOPET rates.

The Enforcement Directorate (ED) has conducted raids on the BC Jindal Group, including Jindal Poly Films, across 13 locations in Delhi NCR and Hyderabad, focusing on alleged violations of the Foreign Exchange Management Act (FEMA). The investigation targets directors and employees over concerns about foreign investments and illegal fund parking, which brings the group’s international financial practices under close scrutiny.

The ED raid covered 13 sites associated with the BC Jindal Group, a major player in the packaging films industry through Jindal Poly Films.

The operation focuses on alleged FEMA violations regarding the group’s foreign exchange transactions, investments, and possible fund parking overseas.

Directors and employees of both the parent company and Jindal Poly Films are being investigated, suggesting possible institutional-level decision-making and compliance lapses.

This is a regulatory enforcement action that relies on FEMA, which is the key legislation regulating India’s foreign exchange ecosystem.

Jindal Poly Management is under monitoring, they are also doing imports from their UAE entity to retain its customers, selling BOPP at cost to cost as Nashik Plants takes 1-1.5 years to revive.