I have no further information about players and their share in market. However, what I understand is that the company has technical tie-up with 4 Global companies which would continue to assist it to grow from trading to manufacturing/marketing business.

Shall keep posted in case get any further information about market.

Good result by Control print. The profit in Q4FY15 is adjusted with following one time:

Exceptional item of of Rs 95.4 Lakhs (Last year Rs 8.08 lakhs). Mainly inventory write down and investment sale

Prior period item of Rs 98.28 Lakhs expense (Last year. Rs 8.02 lakhs). This is CST tax liability of earlier year provided for. Need to understand why this item is appearing constantly.

Higher depreciation due to new companies act resulting in higher depreciation charge of Rs 57.52 during FY15. Not sure whether it should be called one time, but since non cash item, shall not have material impact on cashflow.

Other issues:

No major upswing in interest cost

Total dividend on Rs 4 per share (2 Interim+2 Final). Very good increase in dividend

On June 30,2015 further conversion of 6,00,000 warrants into shares. No further issue to promoter which is good sign. Look at diluted EPS for getting better perspective on valuation.

Delay in deposit of Unclaimed Dividend by one year. Also, service tax payment of Rs 23 lakhs has been overdue for more than six months for reconciliation. Not a very positive sign. Partially get offset by healthy divided tax payment.

Almost Rs 10 crore increase in working capital from March 31, 2014 to March 31 2015, driven by inventory sales also needs attention.

Delay in June results from May 2015 to June 2015 also indicate weak process and system in place for the company.

Limited related party transactions is positive sign.

Overall cautiously optimistic due to following:

Cash generating sales growth (reconfirmed by increase in royalty payment as well). Commencement of new plant of Guwahati in May 2015 also drive profit and sale growth hopefully for next 2-3 years. No major increase in debt despite capex in new plant.

Good dividend and no announcement of further equity dilution

System and process needs to improve so company become regular in payment of statutory dues, reduce prior period items in P&L accounts and publish results on time.

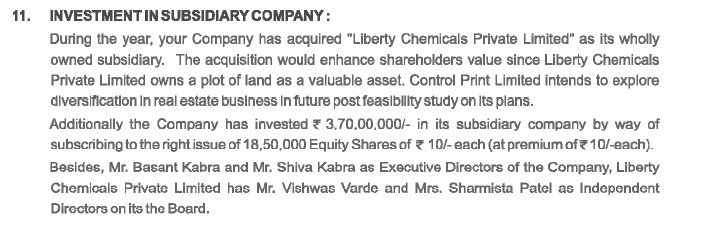

Any information regarding the chemical plant they had bought and were planning to develop real estate jointly.What could be the imbibed value of that ? They mentioned about this in their FY13 annual report.

I looked at other players like Dominos prior to their buyout by Brother’s and their German partner i still have question regarding the scalability of the business?

Can the recent e-commerce wave where a rfid led billing is prominent and government steps with respect to pharma packaging to include manufacturing date etc result in good sales for Control Print?

If someone can share the AGM notes of prior years it would be very helpfull.

Nikhil,

Can you please let me know which page of Annual report of FY13 has real estate development mentioned? I could not trace that.

No clue on the second question.

@ Dhiraj: Sorry my mistake it was from AR of 2012-11 page number 11.Added a snippet of the same.

@Vivek:I think the juice of the Assam expansion is to play out since it was commissioned in Q4.And the major risk that company has always iterated in its AR is about players with higher capacities.

I have been trying to meet the management.Would share my questions with you guys if you have some do shoot? I’ll let you know when i’ll be able to meet.

Assam plant with its tax benefits was commissioned in May 15. I spoke to local sales guy .He was very confident abt co achieving sales figure of 150-200 Crores in time to co,

The German product they are manufacturing it seems has the highest speed when compared to competition.This commissioning gives scalability one of the imp criteria before investing as Opp size is big and ROCE 32%.With this zero debt co assured of 20-25% growth we can ride the stock

Also there are no more warrants left for conversion after recent one.

Co came with an ipo in 1993 and as Ayush says by mistake in hindsight.

These sort of low profile cos listed by chance at times are great wealth creating opportunities.

Looks an interesting micro cap with good financials.

For those looking to get a hang on business, here is an old but decent report from Katalyst wealth (since this is now freely available on their website, I suppose there won’t be any issues with posting link here)-

As in California gold rush pick n shovel co flourished.As Blue dart and other courier/logistics cos flourished due to booming E Commerce sales can Control Print business also boom as each n every item to be delivered wud need its products?

The product becomes necessary due to regulatory compliance issues,inventory tracking,complaint monitoring,freshness of the product.

Due to recent Nestle Maggi fiasco the importance of product becomes all the more imp.

It shud keep on growing at 20-25% cagr n 30-35% ROCE.

Also the elder Marwari promoter seem to be an astute stock picker having picked up gems like Amar Raja batteries v cheap.

Younger one is US educated in a reputed college and Insead MBA.

Most importantly the dilution overhang now seems to be gone with full conversion of all the warrants issued.

Suspension of CFO & Company Secretary 10 Jul 2015 15:54

Control Print Ltd has informed BSE that Ms. Saroj Agarwal, CFO & Company Secretary of the Company has been suspended w.e.f. July 10, 2015 by the Managing Director after consultation with members of the Board of Directors till they take a final decision on her employment.

Sent a mail to CS.Got a prompt response.As SH we have nothing to worry.here is the reply

Dear Investor,

I understand your concerns & fears and I would like to personally reassure

you that there are absolutely no financial irregularities in Control Print

and your trust stands safe.

Regarding the matter of the suspension of Ms. Saroj Agarwal, our CFO and CS,

I can only clarify that none of these matters are related in anyway to

issues with The Company’s Financials and would like to excuse myself from a

detailed reply on the core underlying matters until the outcome of our next

Board Meeting where the Board of Directors will take up this matter. Once

the Board Meeting is done we will certainly answer all investor queries in

depth.

I thank you for your faith & support in our Company.

A dated but still useful report.Company seems to be walking the talk nicely.

Spoke to someone in company.Co seems to be investing in R & D as well for increasing indigenisation.

Co opp size seems big with usage of its products reaching conventional cement,ply ,steel sector as well

Due to its Iindian production company is able to make customised produtcs ,v suitable for Indian power situation,doesnt breaks down easily,Product quality is damn good,service network is strong n experienced.

Best part about the company I iked was the sticky nature of its customer which acts as a moat

Assam plant will boost its profitability further as it was commissioned in May 15 for making mostly consummables only which are highily margin accretive

Maybe I am reading too much. But in many companies where there are financial irregularities committed by the CFO…CEOs tread cautiously and more often than not this is on account of being unduly worried about market perception. I also suspect that the delay in declaring results for FY15 could be on account of the same. It would have been easier to get the CFO to resign and not bring it to the attention of public, however the promoter choose to be transparent / open about it - though not aware of the compulsions. Whatever it is hopefully the worst is behind them.

Company is run by typical first gen entrepreneur who is now executing beautifully ever since he ventured into manufacturing from trading.Now all the warrant allotted have been converted & the promoter statake is 55% no worries on this count.Mkt cap is still low,opp size very big,zero debt company executing nicely well evident in Assam Plant commissioning which will definitely add to bottomline as its focussed on lucrative consumables segment.

All in all management has walked the talk for last several years & has a competent son to take care .Ride the story with 2-3 years POV

While typically resignation of key management person like CFO is concern, as Vivek got reply from the company, we can wait for further development on counter. I have added some more shares during last week at around 240 prices. The spurt in dividend is really very strong indication of good cashflow generation by the company.

Disc: I hold share in the company and my view may be biased. No recommendation to purchase the share

This covers usage of Control Print printers n Inks in only 1 segment ie Cement.Others include which include automotive, agro-chemicals, metals, FMCG, pharmaceutical, food and beverage, wire and cable, pipe, construction materials, and commercial printing.

tHS IMPLIES HUGE OPP SIZE

Key benefits to customer

Two decades of market leadership with complete knowledge of customer needs.

Customer- centric operations.

Superior international technology adapted for the Indian environment.

Powerful local networks giving full support and service any time, anywhere.

Local manufacturing for cost- effectiveness and options of customisation.

Comprehensive product range to meet any coding and marking requirement.

Complete range of consumables.

Deep multi-layered talent base with extensive market knowledge and experience.

Large- character inkjet printers, the NP100 and NP200 systems.

Key features of NP100, NP200 include:

High reliability in especially harsh, dusty environments, including the cement, chemicals, and steel industries.

Advanced hydraulics system requiring no compressed air.

Electronic valve switchover from ink to solvent greatly simplifying maintenance, startup and shutdowns.

7 or 17 drop per head capability enabling large logos and 1-3 lines of print.

10mm-50mm print height.

High print speeds.

Compact footprint.

Low power consumption (only 100W) with no cost of external compressed air.

Macroline software to control all printers from a single console.

Fast drying inks suited for a wide variety of substrates with enhanced adhesion and fade resistance

Through some scuttlebutt I came to know the promoters of Control Print Basant Kabra and his son Shiva Kabra are competent hardworking business men.

Videojet their earlier partners whose products they were distributing suddenly left them in lurch in 2008 breaking the tie up , snatched away many employees by giving them double the salaries all of a sudden.

Any other co and promoter would hv broken down and closed the operations but not Basant ji.He invested all his savings of 20 Crore in setting up Nalagarh(HP) manufacturing operations & rebuilt the business from scratch to become leaders.This shows determination,competence,execution and growth mindset. He shows the same growth mindset by commissioning the Assam plant which again has tax exemptions like HP giving an edge over competitors.

The pie for the business is big enuf for all 3-4 major players due to fast growth n still more growth envisaged due to strict actions being taken by FSSAI post Maggi banning.CP has huge margins in Inks and solvents giving GPM of 68%.Cost of production is 500-600 Rs per kg vs selling price of Rs 6000 per Kg for inks and 150 vs 2000 for solvents.

Incidentally if one reads Polyester prince again by Hamish McDonald it mentions Kamal Kabra ex BSE president who took on RIL in early 90s .Such a gutsy person was the brotehr of Basant Kabra the MD.this shows the quality of family and also the affinity and mastery of Basant ji towards stock markets.

The views expressed here are my personal views. It is a safe to assume I am

personally invested in some of the stock ideas.I invested recently . My views will be biased. This

is NOT a stock recommendation.

Hi vivek thanks for sharing info on the management.

While analysing a company’s numbers I use this formula(cPAT : cCFO) for checking if the company is able to convert its reported profits into cash over a period of time.(borrowed from Dr Vijay maliks blog).

10 year cumulative PAT - 66 cr

10 year cumulative CFO - 25 cr

Over a period of time these numbers should match. But here there is a wide difference in control prints case. There is not a match even when tested for shorter time periods. Am I missing something? Please give your view.